|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Economics of Peak Energy | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | 2009 | 2008 |

One of the best finds of the year is

This is an unedited part of an interview first published on the Lars Schall website. For the full interview see here.

|

|

Switchboard | ||||

| Latest | |||||

| Past week | |||||

| Past month | |||||

|

|

Jul 23, 2013

This is an unedited part of an interview first published on the Lars Schall website. For the full interview see here.

Dr Karin Kneissl is an independent energy analyst, university teacher and writer. From 1990 to 1998 she served in the Austrian Ministry for Foreign Affairs and recently taught several seminars in Turkmenistan and Lebanon, where she works as guest-lecturer in Beirut. She teaches in Vienna (Diplomatic Academy, Military Academy) and at the European Business School (Frankfurt). Her publications range from books on the Middle East (The Cycle of Violence, 2007) to diplomacy. In 2008, a second and revised edition of her book The Energy Poker was launched in Munich, wherein the repercussions of the current financial market crisis on the price of oil and natural gas are tackled. Her articles on the energy market have been published in peer-reviewed journals, notably in India, Poland and France.

The following interview was conducted as her latest book is coming out, Die zersplitterte Welt: Was von der Globalisierung bleibt ("The Splintered World: The Remains of Globalization"), published by Braumuller in Vienna, Austria.

Lars Schall: Dr Kneissl, very recently you have been in Egypt and in Lebanon. What were your experiences there?

Karin Kneissl: I spent a while in Egypt in mid-May and the atmosphere was already very tense; one could really feel that the collapse of the state is imminent. And this is something that is fairly frightening for a country like Egypt, which - in my mind - given its long standing pre-Islamic history - is one of the few countries in the Arab world that is not the outcome of colonization chess board mapping; it has its genuine territorial history for 5.000 years. And that such a country with such a long-standing history of institutions is at the brink of collapse, that is, I think, the most frightening element of the current state of Egypt.

In Lebanon - I just came back from Lebanon two weeks ago - the atmosphere on the spot, continues to be - how should I say? - the traditional optimism of the Lebanese who have gone through terrible times but who have learnt to manage protracted conflicts. Most of my Lebanese interview partners I met are more or less optimistic about the option to avoid the outbreak of an overall conflict. However, most people expect the one or the other booby trap bomb to explode, as we have seen just a few days ago. So the violence in the streets will continue - whether it is in the north or the south of the country. But given the manifold interests at stake in the country, be it from Iran, be it from the Gulf countries, be it some Western vested interests, they might avoid the outbreak of another big conflict inside the country.

LS: Well, Lebanon gets sucked up into the conflict in Syria more and more, is this right?

KK: We have the same confessional pattern on both sides of the border and the old word of Lebanization - you might remember that in the 1970s some political scientists referred to the balkanization of Lebanon, meaning the breakdown of the country in small-sized cantons as we have seen at the beginning of the 20th century - balkanize a country, balkanize a centralized state - and when Yugoslavia started to fall apart in the early 1990s, some political scientists referred to the Lebanonization of Yugoslavia. And today we have some additional terms like the Iraqization, the Somalization and the many spillovers that we have seen from Iraq, from Afghanistan, but particularly from Iraq, into Syria and now from Syria back into Lebanon inter alia, this Shi'ite-Sunni conflict, this inter-Muslim conflict, this is something that very, very closely affects Lebanon as well.

LS: In your new book The Splintered World you have the thesis that World War I in this region is actually still going on. How do you come to this conclusion?

KK: Well, the borders that we see in the Middle East are the immediate outcome of the treaties after World War I, the treaties that were concluded in the suburbs of Paris, in that case in Sevres and later on in Lausanne. And these borders actually have their reference in pipeline agreements of 1920. So the whole region was mapped along the ceasefires, the armistices of ... as the situation in the field was after World War I and what happened to the remnants of the Ottoman Empire, namely the reshuffling of the map of the Middle East by the victorious powers Great Britain and France alongside resource interests, in that case the oil of Mesopotamia, this is the map of today's Middle East.

Now, since I mentioned Egypt just beforehand as one of the few countries, if not the only Arab country that really has a long-standing pre-Islamic, pre-20th century state history ... countries like Syria and Iraq on the other hand, even though their origins as cultures go back to pre-historic times but the nation, the territorial figure of the state is fairly recent and that has a lot to do with the outcome of World War I. And in my eyes that war is still going on because the conflict levels of those days, like, I would say, the fight for Damascus. In my eyes, this city has a much stronger role in Arab history than for instance Jerusalem. Jerusalem is often referred to by Muslims as the third important city and of fairly relevant importance to Arab history. But I would say that Damascus is even more important and we can see the way Turkey, Gulf countries like Qatar and Saudi Arabia and others, are participating in the war in Syria, it is as if World War I was still going on.

LS: Now, when you say that Damascus is so important, does the road to Tehran lead through Damascus?

KK: It is important for Tehran to have a foot in the eastern Mediterranean. However, this is something that not only the Islamic Republic of Iran had been fighting for but it is a very old constant also in Persian history. Iran, Persia, whatever you call it, is the country of the Gulf, of course. But they always wanted to keep a foothold also in the eastern Mediterranean. At various times in history the different Shah dynasties sent Shi'ite clerics to take care of Shi'ite communities in the eastern Mediterranean, such as in Lebanon. And these many constants are also still valid today because for Iran, which sees itself not only now as a power of the Gulf but which also strives for leadership in the Muslim world.

LS: There is also a possible road going from Tehran to Damascus via a pipeline, the Iran-Iraq-Syria pipeline. Do you consider this as an important feature of the conflict in Syria?

KK: I would say in the case of Syria the oil interests are secondary. They were primary in the case of the Iraq War. What might emerge as a larger legacy of the whole conflict is maybe not so much the physical access to certain resources or to pipeline tracing, I think it will be more, as I just mentioned, a fight for Damascus, which has its role in ancient Arab history and it is also about the changing of the maps, the creation maybe of a Kurdish state that is interlinked, I think, in the whole pattern. It has to do with the fight of regional power dominance, both by Turkey and by a number of Arab states and the pipeline tracing according to my assessment is secondary.

LS: The main war theater in the war on terror is Afghanistan and this has become the longest war in US history. How does the balance look like as far as you are concerned? I mean it is now going on for more than twelve years ...

KK: Well, the old coining of the phrase Afghanistan being the graveyard of Empires, or course it is once again very valid and in my book I also refer to a certain analogy. Of course one should never push analogies into the extreme but when the declining Soviet empire decided in 1988 to start withdrawing - and we have here some very interesting details from the Kremlin protocols that were published a few years ago, how Gorbachev and his cabinet desperately were looking for some sort of honorable exit. I think it would be worthwhile studying those protocols of the Kremlin once again because the analogies here are rising.

The kind of mission-accomplished-exit-scenario that the United States and her allies had been building up over the past two years is crumbling. And it will most probably - a lot of indications amount to a scenario where we will have less of an honorable exit but an accelerated exit in a hurry. As we see now certain deadlines are pushed closer; the most important outcome in perception from the Soviet withdrawal from Afghanistan was: look here, rest of the world, a number of shepherds form the Hindu Kush mountain were able to kick out the Red Army! And this kind of perception in my eyes applies also to the current state of affairs because we can see to which point this enormous technological superiority, all the material, financial and political investment that was taken under Obama in the so-called "resurge" a few years ago, all that has resulted in nothing.

On the contrary, what we see right now with the US Army's withdrawal is the biggest destruction of military hardware that has ever happened in history and that might also amount to a change in warfare in the sense that all that war material that was taken into Afghanistan actually has proven to be quite useless. And with that perception in the Islamic world by and large with the current disastrous economic state of affairs of most NATO countries, I would not exclude that ... well, certain analogies might apply also for the Western powers in Afghanistan as was the case for the Soviet withdrawal in January 1989. And as we know, the withdrawal in January 1989 was the beginning of the so-called annus mirabilis that led to the collapse of the Soviet empire.

LS: Isn't it interesting that the US and the regime of Hamid Karzai are now again negotiating with the Taliban about TAPI, the Turkmenistan-Afghanistan-Pakistan-India pipeline?

KK: Exactly.

LS: What is this? Is this a historical joke?

KK: It is. You can call a kind of Treppenwitz der Geschichte, there is no real English translation to that. [1] But I remember fairly well that the first duty trip outside by Karzai when he was elected in 2002 was exactly to Ashgabat, Turkmenistan, because of that pipeline. And some people claim that Mr Karzai, who worked in the oil business before, being brought into Afghanistan, was a man of the oil world. Now, I am not so familiar with the details of his CV ...

LS: I believe he was a consultant of Unocal (Union Oil Company of California) ...

KK: ... but I have always given a certain future to that pipeline because it is something that those countries, those receiving countries, especially Pakistan and India, have a vested interest in. And it is something that we can observe on an overall level: pipelines are turning east and are turning south but they are not turning west. And what enforces that picture is also the fairly successful detente between Pakistan and India that we have seen in the past three, four years despite all the other difficult circumstances but a detente between Pakistan and India is going on. And this, I think, was a major step, and if a number of warlords in Afghanistan can agree on the sharing of the profits then I think that pipeline has a certain chance.

LS: When you say that those pipelines go to the east and not to the west, it reminds me of one theme in your book and this is the rise of the East, in particular China. And that we might go into an Asian age. Can you elaborate on this one?

KK: Well, the Asian age, I think, has to be taken with a certain prudence. But a lot of indicators nevertheless would for the time being be in favor of let's say a multi-polar world where a number of countries in the south and in the east will have a stronger weight than the north-western hemisphere. And for me one of the main elements to argue for such an option is the way those powers organize their strategies in the resource field; the way people are ready to sacrifice something in order to obtain something; the much higher level of curiosity that we will find among younger generations than we have it in our societies. And here of course it would be difficult to put all the countries into one basket and I personally am not such a partisan of the BRICS acronym because these countries are simply so different. But it is nevertheless interesting. Also I would say against the backdrop of the Edward Snowden case, to see how countries like China and Russia behave in that case in contrast to the western countries.

LS: Now that you mentioned it, how do you evaluate the behavior of continental Europe related to these NSA & Co. revelations?

KK: It is shameful. It is really shameful because I mean the basic concepts - I would not even go into norms - but to me simply the concept of asylum and the concept of freedom of speech, the concept of privacy, secret of postal, telephone et cetera ... our rights ... is simply fundamentally violated. And there is no real rising up, there is a kind of funny duty trip by the German Minister of Interior but there is no real outbreak or revolt of anger by the governments in power.

LS: And they also say, well, there is no economic espionage going on. Do you buy this?

... ... ...

Darryl FKA Ron :HAVE FAITH! There MUST be a GOD.

We cannot possibly blame this much stupidity on Darwin :<)

Dec 29, 2014 | RT News

One of the reactors at the Zaporizhia Nuclear Power Plant was automatically shut down after a glitch. This was the second halt in operations in recent weeks at the plant in Ukraine's southeast, which covers at least one fifth of the country's power needs.

"Unit 6 at Zaporizhzhya NPP was disconnected from the network by the automatic system that prevents damage to the generator. The reactor is running at 40 percent of nominal power," the plant's official website says stressing that radiation at the facility is equal to the natural background, which is 8-12 microroentgen/hour.

This accident took place on Sunday morning at 05:59 am local time (03:59 GMT). Causes are still being investigated, while the Energy Ministry hopes to restart the unit in the coming days. The remaining five reactors continue to generate an estimated 4,530 MW.

Late on Sunday, the problem had been fixed and the power plant's sixth power block had been plugged back into the network, the plant said on its website.

"Unit №6 was plugged back in after an error was corrected...At this moment all six power blocks are working," the statement said.

The previous incident at Zaporizhia NPP happened on November 28, but the fact went public five days later, when Ukraine's Prime Minister Arseny Yatsenyuk revealed it during the first session of his new cabinet.

READ MORE: Accident at largest nuclear power plant in Europe revealed by Ukraine PM

At that time the shutdown was caused by a short circuit. As a result, Unit 3 was switched off and put into maintenance to resume operations on December 5.

Dec 29, 2014 | RT USA

Thousands of recently highly paid workers have been laid off after the oil price plummeted 50 percent in 2014. At least four American oil-producing states are already facing budget problems due to decreasing oil revenues.

The price plunge has affected petroleum production in all oil-extracting countries, including the US.

Currently cheap fuel is still believed to be providing an overall boost to the US economy, as consumers can spend less on gasoline and more on shopping and services. But for the American energy sector the future looks less bright. It's effecting places like Alaska, Louisiana, Oklahoma and Texas, the New York Times reports.

US oil experts recall the 1980s oil price downturn, accompanied by economic disasters around the globe and arguably becoming one of the causes of the fall of the Soviet Union. Some experts are positive and say America's oil-producing states won't suffer too much because they "diversified their economies."

This doesn't apply to the state of Alaska. According to the NYT, approximately 90 percent of state's budget is formed from oil revenues. Alaska's government is considering a 50 percent capital-spending cut for bridges and roads in the face of the oil price drop, with Moody's, the credit rating service, lowering Alaska's credit outlook from stable to negative.The state of Louisiana's 2015-16 budget is going to be $1.4 billion short, with 162 state government positions already eliminated and more to be discontinued starting from January. Contracts and projects are being either reduced or frozen in state agencies. According to the state's chief economist Greg Albrecht, for every $1 fall in price of an annual average barrel of oil, Louisiana loses $12 million.

For Texas, which has a far larger and more diversified economy than Louisiana, the oil price downturn is no good either. In just October and November Texas lost 2,300 oil and gas jobs, the federal Bureau of Labor Statistics reported last week. Through the last half a year the state has been losing $83 million in potential revenue every day, the Greater Houston Partnership recently reported. They blamed this on crashing price of its West Texas Intermediate crude oil, which has depreciated to $54.73 per barrel this week, from more than $100 six months ago.

The situation in other oil-extracting states could be even worse. In a study published last year, the Council on Foreign Relations warned the largest job losses caused by sharp decline in oil prices are going to take place in North Dakota, Oklahoma and Wyoming, where the number of drilling rigs is decreasing.

The US oil industry has showed 50 percent employment growth since the recession officially ended in mid-2009, giving jobs to over 779,000 people as of October 2014, the Wall Street Journal reported. A total of 10 million jobs have been associated with the US oil and gas industry, Mark Mills, a senior fellow at the Manhattan Institute, estimated.

Now according to Tom Runiewicz, a US industry economist at IHS Global Insight, if oil stays around $56 a barrel till the middle of the next year, companies providing services to oil and gas industry could lose 40,000 jobs by the end of 2015, while oil and gas equipment manufacturers could slash up to 6,000 jobs.

These workers can earn more than $1,700 a week, much higher than the average $848 a week payment for other workers, the WSJ reported. When experienced workers lose their highly paid jobs, they stop paying their bills.

There are also fears of a house-price slump. Fitch Ratings has already warned that with the price of oil continuing to plummet, home prices in Texas "may be unsustainable."

Chevron suspends its program of oil drilling in the Arctic:

According to Goldman Sachs because of the collapse in oil prices oil investment can be reduced by a trillion dollars: READ MORE: Oil producers to lose $1tn if price below $60 – Goldman Sachs

In China, an increasing shortage of gas. In the heating season, the deficit will amount to 6.2 billion cubic meters:

Oil production is falling apart at high speed, while alternative energy sources such as gas - also in short supply. If OPEC will join the process at the right time, you can expect at least a steady growth of oil prices and as a maximum - a sharp rise in prices at a record high.

However, it should be understood that the oil market is quite inert. I don't be surprised if low oil prices will hold on inertia for several months. However, if nothing unexpected happens, then closer to the end of 2015 we can might expect a recovery in oil prices, may be even to about $ 100 per barrel.

- READ MORE: $20 oil wouldn't force production cut – Saudi oil minister

- READ MORE: Richard Branson: S. Arabia attacking renewable energy with cheaper oil

- READ MORE: Saudi Arabia braces for $39bn deficit, to cut wages due to low oil prices

- READ MORE: Putin says US and key oil producers may be equally interested in lower oil

NYTimes.com

The big losers will be in the Dakotas and Nebraska, but that whole region has a population not much bigger than that of Brooklyn. The big enchilada is Texas; so how big a deal will the oil slump be there?

Pretty big. If you look at the BEA regional data, you learn that mining output nationally is up a lot - 39 percent between 2007 and 2013 - but that this is still fairly small change on a national basis, 0.7 percent of 2007 GDP. However, more than half the mining growth took place in Texas, which was only 8 percent of the national economy. So in Texas mining directly contributed 4.7 percent to GDP; if we use a multiplier of 1.5, which is what the best research suggests, we conclude that the shale boom added 7 percent to Texas's growth - and what shale giveth, shale may now take away.

tanstaafl, Houston

"Should be interesting to watch."

The Dallas Fed predicts 125,000 jobs lost in Texas over the next 6 months; glad Krugman is entertained by this.

Jack, Illinois 11 minutes ago

I don't get it. We're supposed to be running out of oil, right? Or has that changed? $2 gas and we've gone past the Bell Curve of supply and use? And now we're all drunk on cheap gas. I'm happy to see new innovative efficient technology, new electric and hybrid cars but now they're selling boatloads of SUVs and pickup trucks. They are back in big style. They are better now, instead of 11 mpg they're 15 mpg.

Doesn't that figure into this discussion where oil is going? Has new technology changed any fundamentals? When does oil come back up in price? Does that mean a return of the oil producers, Saudi Arabia, Russia, Venezuela? I don't think you have but there are a lot of people all agog about low oil prices that seem to have forgotten that not too long ago they were telling us it was all going to run out one day.

Dec 21, 2014 | The New Republic

But the schadenfreude over Russia's demise should be tempered by the knowledge that the U.S. has its own regional petro-states. As the White House never tires in pointing out, the U.S. leads the world in oil and gas production, and amid this collapse, those projects are under serious pressure. While the overall impact of falling oil prices may help our economy overall, it will hurt those areas dependent on fossil fuel production-and potentially, it could affect all of us.

Taking the big-picture view, you can see lots of benefits from lower energy costs. Falling oil prices pull down inflation, which could keep the Federal Reserve from raising interest rates prematurely. But more generally, there are obviously two interested parties in any energy transaction-producers and consumers. And while producers may reap fewer profits from cheap oil, consumers ought to love it.

AAA estimates that the average consumer is saving $100 a month on gasoline (Goldman Sachs puts the total savings at $75 billion over the past six months), and this has already led to surging retail sales. Lower-income households devote a greater proportion of their incomes to energy, and we can expect them to turn around and spend the extra cash. With consumer spending making up two-thirds of the economy, this results in a nice bump to gross domestic product. In fact, if you see this as a redistribution from oil producers to consumers, you can even tell a story about how it reduces inequality.

But a macroeconomic analysis obscures how the explosive growth in U.S. oil production-the biggest in 30 years-has been confined to a few select regions. In particular, areas with traditional oil or shale gas basins-including plains states like Wyoming and western North Dakota, as well as Oklahoma, Texas, and Alaska-have seen the biggest growth in production, as sophisticated drilling techniques become widespread.

These areas helped to increase employment in the oil and gas industry by 100,000 workers since 2010, with predictions of millions more in the coming years. But drilling for shale oil remains costlier than, for example, drilling for oil in the Middle East, and makes far more economic sense when prices are high. If prices pass the "breakeven" point, where the cost of production exceeds the revenue gained, those projects will grind to a halt, with idled rigs, reduced hours, and plenty of layoffs.

While it's difficult to pinpoint the breakeven, with estimates varying wildly, there are indications that we're getting close. One Morgan Stanley analysis shows that, under current prices, 80 percent of U.S. shale projects would lose money. This week, Goldman Sachs predicted a loss of $930 billion in future oil production, particularly in areas like south Texas and the Gulf of Mexico. Some reports show that production has already slowed in the lucrative Bakken oil field in North Dakota. Permits for new wells fell by 36 percent in both west Texas and North Dakota in November. Some Texas wildcatter veterans are already talking about going into "survival mode," while their rookie counterparts in North Dakota have blown off the fears.

In general, it's good news for the world to have less oil drilling activity. But it is bad news for boomtowns that got fat and happy on drilling, without diversifying their economies to prepare for the aftermath. That aftermath may not come right away-if the well has already been drilled, it may make sense to keep going-but it's bearing down fast.

What sets these regions apart from, say, Russia, is that they have no independent monetary policy they can employ for quick relief. And the key regions for shale drilling happen to be fairly conservative, so you can hardly expect aggressive fiscal actions at the state level. In fact, many of these areas factor oil revenue into their government budgets, and so the result of a crash could be drastic spending cuts, affecting the most vulnerable members of society. North Dakota appears to be at least thinking about the implications of over-reliance on one volatile industry, but they haven't fully prepared for the fallout yet.

The real unknown is how much domestic oil and gas production has been driven by debt, which could change this from a local to a national problem. Oil producers who financed their investments with borrowed money may not be able to pay back the loans, and default rates are expected to double over the next year. For this reason, investors have sought large interest rate premiums to hold energy-related bonds. Debt-laden producers have to keep pumping crude to pay off creditors, and that could create a fire sale where prices fall even further, putting more companies in rough spots as they reach their breakeven point.

Moreover, borrowed money used to finance energy products often made its way into junk bonds made up of packages of corporate debt, known as "leveraged loans." These loans have been enormously popular for investors seeking high returns. But the collapse of oil prices has sent investors running to withdraw from funds that purchase these securities. So far this appears to be limited to the energy sector, which is crashing. But nobody seems to know precisely how much energy debt was stuffed into these bonds. Investment managers are frantically scanning their portfolios to determine their exposure to energy-related debt. And if they cannot exit fast enough, it will result in significant financial stress.

One interesting theory argues that big banks needed to eliminate derivatives rules in the year-end budget bill to ensure bailout protection for their credit default swaps, and hedge their bets against an oil-related financial crash. This theory is bolstered by the fact that banks have had trouble getting energy-related junk debt off their balance sheets. Presumably we all remember what can happen when banks get saddled with toxic assets.

This is all separate from how instability in Russia and several emerging markets could impact the U.S. economy. American mega-banks are exposed to global debt and will almost certainly have to write off loans from abroad. And trade will suffer from a prolonged, energy-related slump that ripples across the world.

The United States is big enough that major financial shocks like the oil collapse could have separate impacts in different parts of the country. But the potential for financial crisis exists in a way that it hasn't since 2008. And the country is far less prepared for recession than it was then-we still have near-zero interest rates and a Congress opposed to fiscal stimulus. Maybe it will turn out for the best, but we should brace ourselves for the worst.

AlexeyStrelkov

I have to disagree with other commenters here - while cheap oil can be good for the economy, current oil prices will ruin it since they are unsustainable. Let me explain:

1) if oil price goes below 40$, ALL major American shale projects will be stopped http://www.bloomberg.com/news/2014-10-17/oil-is-cheap-but-not-so-cheap-that-americans-won-t-profit-from-it.html that will lead to a local deficit, which will increase prices, but by that time most oil&gas companies will go bust since they are cash negative http://www.wsj.com/articles/SB10001424052702304688104579467810326527526

2) this will destabilise the market http://www.bloomberg.com/news/2014-12-11/fed-bubble-bursts-in-550-billion-of-energy-debt-credit-markets.html

3) American manufacturers will be deprived of domestic energy, they will have to rely on foreign imported oil once again (which increases geopolitical risks, by the way).

Cheap oil is good for everyone (especially considering that oil prices were hugely inflated until 2014), but too cheap is good for no one.

beihai@AlexeyStrelkov you contradict yourself, since they are unsustainable they will not ruin the economy, for the first time in years the American consumer is enjoying slightly lower gas prices and oil companies lower profits. If some go bust then they go bust, what makes them above the free market? And we won't be "deprived" of domestic energy, it will still be there for when prices go up again.

your argument is terrible. If we can buy something BELOW cost then we should. There is no geo political risk is impoverishing oil producing countries. If anything NOW is the time to hike gas taxes in America to pay for our infrastructure repairs. Whatever jobs would be lost in the oil fields will be made up in fixing our roads and bridges.

AlexeyStrelkov

@beihai @AlexeyStrelkov First of all, let's get it clear - I am not here because I am Russian, I am here because I am actually working in the oil&gas industry.

American consumers are enjoying slightly lower gas prices BECAUSE American shale exists. If it did not exist, you would be paying anything OPEC wants you to pay. And if the shale goes bust, who would be there keep those prices low? Saudi Arabia? Qatar? Venezuela?

And no, when the prices go up AFTER the industry is done for, it won't just magically reappear. American shale was made possible by three things - available hardware (America is the biggest producer of specialized equipment in the planet), available engineers (when it comes to drilling, America has a lot of them) and available money (thanks to QEs, the markets were swimming in cheap money). QEs are gone now, if shale becomes economically unfeasible, rigs and engineers will be gone too. It will take years to get them back and I am not sure QEs will ever be back.

And importing oil will ENRICH oil producing countries, not impoverish them. And drilling engineers will not be employed by the construction industry, their skills are simply not transferable.

P.S. In it's current state American shale resources are not profitable on their own (+thanks to bankers, the whole affairs reeks of another market bubble). But if they are used in CONJUNCTION with bringing the manufacturing back from Asia, then it makes sense! Manufacturers get guaranteed supply of energy and resources, become more competitive, sell more stuff, make bigger profits, pay more taxes to the government and the government uses said taxes to ensure that they get guaranteed supply of energy and resources.

I think that was Obama's plan initially, but looks like it wasn't really successful.

TracySchmidt

@beihai @Gadfly7 @AlexeyStrelkov

There is no such thing as "the law of supply and demand."

They are two separate laws.

- The law of supply says that, all other factors being equal, as the price of a good or service increases, the quantity of goods or services that suppliers offer will increase.

- The law of demand says that, all else being equal, as the price of a good or service increases, demand falls for that good or service.

This is basic economics.

aewren86

@Gadfly7 @beihai @AlexeyStrelkov Well it does have a great deal to do with OPEC policies, but those policies are designed to crush our shale projects here that are cutting into their market share. They also want to put the screws to the Iranians who desperately need $100+ a barrel oil just to cover their obligations.

We get cheap oil, the Iranians and Russians can't afford anymore adventures, I really can't see a downside other than for our Boomtowns, and well we all know what comes after a boom...

Gadfly7

@aewren86 @Gadfly7 @beihai @AlexeyStrelkov

That is how the game is played today. We will crush them and bend them to our will through energy a/o economic blackmail, sanctions or other mafia style games.

However, the Chinese are loving it and the USA is trying to figure out what to do with them next.

We assume nobody will fight back.

P.S. Take that SONY pictures. It's perfectly Ok to pretend an assassination of a countries leader if we don't like him. How naïve a Seth Rogen.

beihai

@aewren86 @Gadfly7 @beihai @AlexeyStrelkov Iran also has vast stores of natural gas and holds some of the world's largest deposits of natural gas with an estimated 33 trillion cubic meters of gas reserves, ranking fourth in the world for gas reserves, and the second-largest natural gas reserve storage facilities world-wide, according to the BP statistical review of world energy published in June 2014.

I don't know. If Saudi Arabia was really so desperate to put the screws to Iran they would have been selling very cheap oil for years and years, I think people are putting too much stock in conspiracy and not enough on basic economics, that is people priced oil last year on the expectation that things in Ukraine would be far worse causing oil to spike and that the EU and China's economies would be stronger. The US is one of the few countries outperforming expectations but we are also producing more oil than ever ourselves, as are the Canadians.

As to our boomtowns, they are small populations in North Dakota so I don't care. Texas will be interesting. They are America's Arabia, one industry dependent and backwards in most other respects. I hope oil prices stay low for a while.

beihai

@Gadfly7 @beihai @aewren86 @AlexeyStrelkov look, OPEC is essentially a criminal cartel whose main reason for existence is price fixing so i get your point that supply and demand sounds like a cliche but cliches have some validity. When prices spike people drive less, buy more fuel efficient cars and even migrate from gas entirely with CNG buses and the like.

ISIS has been selling oil as fast as it can otherwise they would have no money to buy food. This is the nature of humanity, to make a buck people would buy and sell with their worst enemy.

Saudi Arabia wants to maintain its market share, they don't want to be the country that has to cut production because of all of the new production elsewhere. Back in 2008 the US produced 5,000 ,barrels of oil per day, we are now up to 7,442 in 2013 bpd. in 2008 Canada was at 3,300 bpd, now it is up to over 4,000 (2013).

http://www.eia.gov/countries/country-data.cfm?fips=ca#pet

in comparison Saudi Arabia is at 11,600 bpd. The US and Canada have increased output from 8,300 bpd to 11,442 bpd.

And this was 2013. These are raw numbers, if the US and Canada is producing more oil than Canada produced entirely in 2008 that oil has to go somewhere.

TracySchmidt

@beihai @aewren86 @AlexeyStrelkov

LOL!

As of September of this year, the U.S. produced 8.864 MILLION barrels of oil per day.

In 2013, the U.S. produced between 7 million and 7.8 million barrels per day, not the absurdly low figure of 5,000 barrels per day.

So says the U.S. Energy Information Administration.

HughMagbie

No wonder your mag is going down the tubes. Ever since we passed the Commodities Modernization Act of 2000 Wall St has been able to manipulate the currency/commodity markets to artificially hype oil to over 100 dollars a barrel. Big oil and petro countries engaged in an orgy of spending and sometime saber rattling with their phony gdp. Big oil got out of refining and distillates and concentrated on oil exploration, demolishing the big lie of peak oil. Folks all over the world had to chose to heat or eat. Big oil.and Wall St demolished the middle class and.made the largest profits in history during a recession. Now they are getting demolished by the Saudis.

I.don't care how many oil jobs are destroyed, they were jobs created by predatory speculation that hurt far more.people than helped. They will be coming to us soon for a bail out. I don't want.to bail out big oil and Wall St,I.want Wall St oit of the currency/ commodity markets, and I think that of you want to save the doomed fracking industry from the Saudi price war, you'll have to.nationalize it in the name of national security.

US oil should be free from the speculators, they should be broken up.and their assets returned to those who.have had trillions stolen from them by this collosal scam.

Dec 26, 2014 | RT Business

The Finance Ministry said the government will try to save some money by cutting salaries, wages, and allowances that represent around "50 percent of total budgeted expenditures." But the move could anger Saudi youth, who are already struggling to cover the costs of living in the country.

According to the International Monetary Fund (IMF), about two-thirds of the population works for the government.

The 2015 budget includes 860 billion riyals (US$229.3 billion) in spending and 715 billion riyals ($190.7 billion) in revenue. Saudi Arabia promised to cover the difference by digging into its reserves.

Jim Oksvold

Saudi Arabia wants a higher market share for their oil and can afford to fight for it.

Giordano Bruno

Sure, they can 'afford' to get rid of their national treasure at a faster rate, at lower prices.

Once it's gone, they are dirt poor again.

Or sand poor, in their case.Evelyn Axiaq

Cutting wages? They should start from themselves. The most senior princes are billionaires and multi millionares. The other 3000 royal family members all have hefty allowances for nothing. All this thanks to Saudi oil wealth. Saudi's oil belongs only to the royal family dictatorship, and not to the ordinary citizens.

Serge Krieger

when you plot mischief for others, you're preparing trouble for yourself

Ivan Butko

Oil and gas shipments accounted for 68% of Russia's total $527bn of gross exports in 2013, when Brent crude - comparable to Russian Urals - traded at an average of $108 per barrel.

Should the current price of Brent, at around $60 per barrel, be sustained over the next 12 months, that would result in Russia's export income from crude dropping to $95bn, from $174bn in 2013. However, these losses will be amplified by the total loss of revenue accrued from lower prices for refined petroleum products and domestic sales of crude, which totalled $122bn in 2013.

As for Saudis, lower price is something they are willing to accept..

Dec 24, 2014 | zerohedge.comIf you only paid attention to the mainstream media, you'd be forgiven for thinking that the US is going to get away from the collapse in oil prices scot free. According to popular belief, America is even going to be a net winner from cheaper oil prices, because they will act like a tax cut for US consumers. Or so we are told.

In reality, though, many of the jobs the US energy boom has created in the last few years are now at risk, and their loss could drag the economy into a recession.

The view that cheaper oil automatically boosts US GDP is overly simplistic. It assumes that US consumers will spend the money they save at the pump on US-made goods rather than imports. And it assumes consumers won't save some of this windfall rather than spending it.

Those are shaky enough. But the story that cheap fuel for our cars is good for us is also based on an even more dangerous assumption: that the price of oil won't fall far enough to wipe out the US shale sector, or at least seriously impact the volume of US oil production.

The nightmare for the US oil industry is that the only way that the market mechanism can eliminate the global oil glut-without a formal agreement between OPEC, Russia, and other producers to cut production-is if the price of oil falls below the "cash cost" of production, i.e., it reaches the price at which oil companies lose money on every single barrel they produce.

If oil doesn't sink below the cash cost of production, then we'll have more of what we're seeing now. US shale producers, like oil companies the world over, are only going to continue to add to the global oil glut-now running at 2-4 million barrels per day-by keeping their existing wells going full tilt.

True, oil would have to fall even further if it's going to rebalance the oil market by bankrupting the world's most marginal producers. But that's what's bound to happen if the oversupply continues. And because North American shale producers have relatively high cash costs (in the $30 range), the Saudis could very well succeed in making a big portion of US and Canadian oil production disappear, if they are determined to.

In this scenario, the US is clearly headed for a recession, because the US owes nearly all the jobs that have been created in the last few years to the shale boom. All those related jobs in equipment, manufacturing, and transportation are also at stake. It's no accident that all new jobs created since June 2009 have been in the five shale states, with Texas home to 40% of them.

Even if oil were to recover to $70, $1 trillion of global oil-sector capital expenditure-in fields representing up to 7.5 million bbl/d of production-would be at risk, according to Goldman Sachs. And that doesn't even include the US shale sector!

Unless the price of oil miraculously recovers, tens of billions of dollars worth of oil- and gas-related capital expenditure in the US is going to dry up next year. While US oil and gas capex only represents about 1% of GDP, it still amounts to 10% of total US capex.

We're not lost quite yet. Producers can hang on for a while, since there has been a lot of forward hedging at higher prices. But eventually hedges run out-and if the price of oil stays down sufficiently long, then the US is facing a massive amount of capital destruction in the energy industry.There will be spillover into the financial arena, as well. Energy junk bonds may only account for 15% of the US junk bond market, or $200 billion, but the banks are also exposed to $300 billion in leveraged loans to the energy sector. Some of these lenders are local and regional banks, like Oklahoma-based BOK Financial, which has to be nervously eyeing the 19% of its portfolio that's made up of energy loans.

If oil prices stay at $55 a barrel, a third of companies rated B or CCC may be unable to meet their obligations, according to Deutsche Bank. But that looks like a conservative estimate, considering that many North American shale oil fields don't make money below $55. And fully 50% are uneconomic at $50.

So if oil falls to $40 a barrel, a cascading 2008-style financial collapse, at least in the junk bond market, is in the cards. No wonder the too-big-to-fail banks slipped a measure into the recently passed budget bill that put the US taxpayer back on the hook to insure any ill-advised derivatives trades!

We know what happened the last time a bubble in financial assets popped in the US. There was a banking crisis, a serious recession, and a big spike in unemployment. It's hard to see why it should be different this time.

It's a crying shame. The US has come so close to becoming energy independent. But it's going to have to get its head around the idea that it could become a big oil importer again. In the end, the US energy boom may add up to nothing more than an illusion dependent upon the artificially cheap debt environment created by the Federal Reserve's easy money policy.

* * *

To find out more, sign up for Marin Katusa's just-launched advisory, The Colder War Letter.

Tyler Durden on 12/24/2014 - 20:32We live in a new world, and the Saudis are either the only or the first ones to understand that. Because they are so early to notice, and adapt, I would expect them to come out relatively well. But I would fear for many of the others. And that includes a real fear of pretty extreme reactions, and violence, in quite a few oil-producing nations that have kept a lid on their potential domestic unrest to date. It would also include a lot of ugliness in the US shale patch, with a great loss of jobs (something it will have in common with North Sea oil, among others), but perhaps even more with profound mayhem for many investors in US energy. And then we're right back to your pension plans.

"People should not be worried," explained Kazakhstan President Nursultan Nazarbayev in a TV address over the weekend, "we have a plan in place if oil prices are $40 per barrel." Kazakhstan, the second largest ex-Soviet oil producer after Russia, explains "there are reserves which could support people, preventing living conditions from worsening."However, if A. Gary Schilling's reality check of $20 oil being possible comes to fruition, as he explains, what matters are marginal costs - the expense of retrieving oil once the holes have been drilled and pipelines laid. That number is more like $10 to $20 a barrel in the Persian Gulf... We wonder who has a plan for that?

The Kazakh President says "don't worry", as Reuters reports...

Kazakhstan, the second largest ex-Soviet oil producer after Russia, has plans in place should global oil prices fall as low as $40 per barrel, President Nursultan Nazarbayev told local TV channels.

"Kazakh people should not be worried. We have a plan if oil price are $70, $60, $50, $40 per barrel," he said, according to a transcript published on his website www.akorda.kz.

"There are reserves which could support people, preventing living conditions from worsening," he said, without providing any details.

Kazakhstan's National Fund, which collects oil revenues, stood at $76.8 billion at the end of November. Separately, the central bank's net gold and foreign exchange reserves stood at $27.9 billion.

Nazarbayev has also urged the Kazakh people not to worry about the slide in Russia's rouble currency, which has lost some 45 percent of its value versus the dollar this year.

But A Gary Schilling is less sure... (via Bloomberg View)

When the U.S. Federal Reserve ended its quantitative-easing program in October, it also ended the primary driver of U.S. stocks during the past six years. So long as the central bank kept flooding the markets with money, investors had little reason to worry about a broader economy limping along at 2 percent real growth.

Now investors face more volatile markets and securities that no longer move in lock-step. At the same time, investors must cope with slower growth in China, minuscule growth in the euro area and negative growth in Japan.

Such widespread sluggish demand -- along with ample supplies of oil and most everything else -- is the reason commodity prices are falling. They have been since early 2011, but many people failed to notice until recently, when crude oil prices nosedived.

Normally, less demand and a supply glut would lead the Organization of Petroleum Exporting Countries, beginning with Saudi Arabia, to cut production. As the de facto cartel leader, the Saudis would often reduce output to prevent supply increases from driving down prices.

Of course, this also cost the Saudis market share and encouraged cheating by OPEC members. Saudi leaders must grind their teeth over the last decade's unchanged demand for OPEC oil, while all the global growth has been among non-OPEC suppliers, principally in North America.

That may explain why, while Americans were enjoying their Thanksgiving turkeys, OPEC surprised the world. Pressed by the Saudis and other rich Persian Gulf producers, it refused to cut output despite a 38 percent drop in the price of Brent crude, the global benchmark, since June.

OPEC, in effect, is challenging other producers to a game of chicken. Sure, the wealthier producers need almost $100 a barrel to finance bloated budgets. But they also have huge cash reserves, which they figure will outlast the cheaters and the U.S. shale-oil producers when prices are low.

The Saudis also seized the opportunity to damage their opponents, especially Iran and what they see as Iran-dominated Iraq, in the Syria conflict. They also want to help allies Egypt and Pakistan reduce expensive energy subsidies as prices fall.

Then there's Russia, another Saudi opponent in Syria, with its dependence on oil exports to finance imports and 42 percent of government outlays. With the ruble collapsing, the Russian central bank let the currency float in November after blowing through $75 billion to support it. Then the central bank tried to stop the free fall by raising interest rates by 6.5 percentage points to 17 percent on Dec. 15.

Still, the Russian currency is floundering, along with the economy. Consumer prices in Russia rose 9.1 percent in November from a year earlier. The economy will be in recession next year, the website of the Russian economy ministry acknowledged for a few hours on Dec. 2, before the posting was deleted.

Venezuela is also suffering. The government needs $125-a-barrel oil to cover its spending, of which 65 percent depends on oil exports. Its crude production is down a third since 2000. With inflation raging, the bolivar officially sells for 6.29 a dollar, but for 180 on the black market.

In Nigeria, where oil and natural gas account for 80 percent of government revenue and almost all its exports, the naira has fallen 11 percent versus the greenback so far this year.

How low can oil prices go?

In the current price war, the global market price needed to support government budgets isn't really the main issue. Nor are the total costs for exploration, drilling and transportation.

What matters are marginal costs -- the expense of retrieving oil once the holes have been drilled and pipelines laid. That number is more like $10 to $20 a barrel in the Persian Gulf, and about the same for U.S. shale-oil producers. The estimated $50 to $69 a barrel break-even point for most new U.S. shale-oil production is less relevant.

Developing countries that depend on commodity exports for hard currencies to service foreign debt will produce and export even at prices below their marginal cost. Until some major producer chickens out and cuts production, oil prices should remain low. They could decline a lot more than the 50 percent drop so far.

Arius

Tylers - the headline is misinterpretating what kazakh states. They already have plans for 40 ... what they are saying is Bring it On ... the ball is in your court ... You dig?

Arius

The question is how low can the banks bring the oil prices without the oil derivatives exploding?

the kazakh are saying at 50 or 40 we dont care ... now hold or fold? Game ON

Jumbotron

Ahem......peak oil is still here. The Saudi's are cutting with water more and more. Shale had not even got us back to domestic peak in 1970. The GOM is not producing any more big finds. Alaska is in terminal decline. North Sea is in terminal decline. Mexico is in terminal decline. Canada has to scrape the bottom of the toilet bowl (Tar Sands) to be an oil player.

And we are on the cusp of the Great Collapse of the Great Ponzi (2020-2025) so there will be no investment available for REALLY hard to get at places like the Artic.

KansasCrude

No we are spending a barrels worth of energy to get a barrels and a half worth of energy with shale. Try running our society with that kind of net energy. No freaking way the only reason we are not seeing well over $100 is because our economy sucks so bad we are using 4 million barrels a day less than 2008. Quit kidding yourself the cheap easy stuff is gone. If we are going to see the economies of the world continue to suck then we are going to see oil remain cheaper than $150 IF the dollar doesn't desinigrate. If we get the USD valued at reality then maybe that will look cheap.

The Bakken is peaking now.....Eagle Ford soon. Shale oil is a scam.

noben

Think outside the barrel, outside the Petrodollar: If the USD can be backed by a Real Asset like Petroleum, so can every other currency. Or be backed by PM.

At this rate... given that all currencies that are getting hammered by the USD will only be able to trade with EACH OTHER anyway, why not accept and front-run this thing?

IOW: Your citizens and businesses have in effect been forced to drop the USD anyway (can't afford to import goods from US, EU), so you might as well make it official: "The currency of our country will no longer by indexed to the USD, but to PMs, Petroleum or the CNY". That would kill the USD in weeks.

Kaboom, Dollar Kabal!

NoDebt

This is awesome. It's just like a depression but without the stock market crash. Someday in the far future we'll understand just what REALLY was going on these last few years. Cause we're sure as hell not getting the truth right now. (Secret E.O.'s anybody?)

Al Huxley

You know, the only thing bothering me is I must have missed the part in J-Bag's speech last week where she promised that the Fed would cover any bad debt resulting from the collapse of the shale industry. But no big deal, she must have mentioned it somewhere along the way.

sun tzu

You can check their balance sheet weekly. It's still growing.

http://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

Click on view as table.

Oct 1, 2014 = $4.450 trillion

Dec 17, 2014 = $4.502 trillion

An increase of over $50 billlion in 10 weeks. That's $5 billion per week of bonds they're still buying after QE3 "ended"

cowdogg

Gary Shilling is an idiot and always has been. The fact is there are no free lunches and nobody is going to produce something below cost for long. All in costs for oil production no matter where is above $80 and continually going up because what is produced has to be replaced at much higher prices or you are in the process of going out of business.

YHC-FTSE

I don't care how fucking sluggish the demand is, $20 is ridiculous. This isn't 1979 and the demand is multiples higher than it was 30+ years ago.

The thing with commodities, it's mostly dug out where the owners of the land are shit ignorant. First it was glass beads, next it was coins, and now we give them the alluring choice between shiny toilet paper or bullets and bombs. With the exception of the sheep fucking president of Kazhakstan, I seriously doubt anyone sane would be willing to sell their oil at $20. That's is so fucking stupid, it's almost Obamic.

Al Huxley

Saudis have magnanimously decided to supply the entire global demand at .80/barrel. Suspend your judgement and critical thinking, get long the S&P, DOW and NASDAQ and enjoy the party! You'll be able to pay for your $1/gallon gas with the daily profits on your market investments, and employment won't be a problem because you'll be making enough off the market to pay for everything, especially with the radically reduced cost of living that will come from more-or-less free commodities.

As NoDebt said, it's all the best parts of a depression, but without a crashing stock market, so just get into the market with all you've got and you'll be fine.

HowdyDoody

Courtesy of derivatives, the $ price can be anything those with power want it to be. The $ price of everything is fixed.

BouncingCat

What the shale oil boom has produced is a ceiling for the price of oil. If OPEC wants all the oil revenue, they just have to keep the price down below other producer's costs. So if shale has a marginal cost of 50-69, that becomes OPECs ceiling until demand increases.

techstrategy

The shape of the supply curve is changing rapidly over time. With 30-40% depletion rates, we lose 2 million barrels if domestic shale per year absent new drilling.

The full lifecycle cost becomes relevant far faster than people are projecting. Depletion rates in traditions fields are on the order of 5-7%, which means at least another 5 MM BPD absent global drilling. Coupled with elasticity of demand (increase in quantity demanded at lower prices) and we'll work through this "glut" much more rapidly than Shilling and shills appreciate.

The isn't the excess housing stock. We have to run hard to stay in place with petroleum production.

CitizenPete

Before you all go steppin on each other with too much gusto, perhaps you need to agree to the definition of the term "Peak Oil". Then you can chase each other in circles doing the russian squat dance. You could actually be in violent agreement at this point.

When someone says 'oil has already peaked' or 'peak isn't until 2020', what do they mean? Peak Oil can (and will) have many definitions. It would benefit policy debates and discussions if there were a universal, agreed-upon definition. The most common is the year in which global crude oil production reaches its maximum sustained level, followed by a permanent decline. Some (Ken Deffeyes) define Peak as the date when 50% of the world's oil has been used irrespective of the annual flow rate (presumably, we could have used 50%+ of our oil and still have rising production if technology is allowing us to borrow from what would have been a bell shaped curve.)

Other definitions differ in what is included as 'oil'. The most restrictive includes only oil graded as "Light Sweet". More common definitions include condensate and Natural Gas Plant Liquids (NGPL).

Still broader definitions include the heavy oils, the Orinoco oil sands, and the Alberta tar sands. And the broadest measure of 'what is oil' might include corn and sugarcane turned to ethanol, palm nuts turned to biodiesel, and coal turned to diesel fuel. This is referred to as "All liquids" and is what is commonly reported as total oil production in the media."

hendrik1730

The "marginal cost" for shale oil production is not comparable to classical wells since they run virtually dry in 3 years. Their true average production cost per barrel MUST be at least 3 times higher than that for classical wells - if not more. Why does one think the shale oil producers are drilling additional wells like crazy ( now dropping steeply because of no longer viable economically )? Not for increasing production, just for keeping output more or less constant. Also bear in mind that virtually all the "sweet spots" in the Bakken have already been drilled empty, so oil extraction cost is on the rise and the hangover is on its way ....

Quinvarius

When the stupid predictions start coming out of Wall Street that means that a large move has already happened, the trend is probably coming to an end. No one is going to let 20 oil happen. And now that Wall Street says they want it, it will be resisted.

No matter what Saudi Arabia says, they are being destroyed. They cannot take these prices any more that anyone else without a bailout, probably less so.

December 22, 2014 | IMF

(Versions in 中文, Français, and Русский)

Oil prices have plunged recently, affecting everyone: producers, exporters, governments, and consumers. Overall, we see this as a shot in the arm for the global economy. Bearing in mind that our simulations do not represent a forecast of the state of the global economy, we find a gain for world GDP between 0.3 and 0.7 percent in 2015, compared to a scenario without the drop in oil prices. There is however much more to this complex and evolving story. In this blog we examine the mechanics of the oil market now and in the future, the implications for various groups of countries as well as for financial stability, and how policymakers should address the impact on their economies.

In summary:

- We find both supply and demand factors have played a role in the sharp price decline since June. Futures markets suggest that oil prices will rebound but remain below the level of recent years. There is however substantial uncertainty about the evolution of supply and demand factors as the story unfolds.

- While no two countries will experience the drop in the same way, they share some common traits: oil importers among advanced economies, and even more so emerging markets, stand to benefit from higher household income, lower input costs, and improved external positions. Oil exporters will take in less revenue, and their budgets and external balances will be under pressure.

- Risks to financial stability have increased, but remain limited. Currency pressures have so far been limited to a handful of oil exporting countries such as Russia, Nigeria, and Venezuela. Given global financial linkages, these developments demand increased vigilance all around.

... ... ...

Again, our simulations of the impact of the oil price drop do not represent a forecast for the state of the world economy in 2015 and beyond. This we will do in the IMF's next World Economic Outlook in January, where we will also look at many other cross-currents driving growth, inflation, global imbalances and financial stability.

... ... ...

Oil prices have fallen by nearly 50 percent since June, 40 percent since September (see Chart 1).[2] Metal prices, which typically react to global activity even more than oil prices, have also decreased but substantially less so than oil (see Chart 2). This casual observation suggests that factors specific to the oil market, especially supply ones, could have played an important role in explaining the drop in oil prices.

On the supply side, the evidence points to a number of factors, including surprise increases in oil production. This is in part due to faster than expected recovery of Libyan oil production in September and unaffected Iraq production, despite unrest.[3]

A major factor, however, is surely the publicly announced intention of Saudi Arabia - the biggest oil producer within OPEC - not to counter the steadily increasing supply of oil from both other OPEC and non-OPEC producers, and the subsequent November decision by OPEC to maintain their collective production ceiling of 30 million barrels a day in spite of a perceived glut.

The steady increase in global oil production could be seen as "the dog that didn't bark." In other words, oil prices had stayed relatively high in spite of the upward trajectory in global oil production due to the perception at the time of OPEC's induced floor price. The resulting shift by the swing producer however helped trigger a fundamental change in expectations about the future path of global oil supply, in turn explaining both the timing and magnitude of the fall in oil prices, bringing the latter closer to the level of a competitive market equilibrium. A similarly dramatic drop took place in 1986, when Saudi Arabia voluntarily stopped being the swing producer, causing oil prices to fall from $27 to $14 per barrel, only to recover fifteen years later, in 2000.

Beyond traditional demand and supply factors, some have pointed to "financialization"-oil and other commodities considered by financial investors as a distinct asset class-and "speculation" as contributors to the price decline.[4] We see little evidence that this is the case. According to the latest report from the International Energy Agency, oil inventories have reached their highest level in two years, suggesting expectations of price increases, not price declines.

How persistent is this supply shift likely to be?

This depends primarily on two factors:

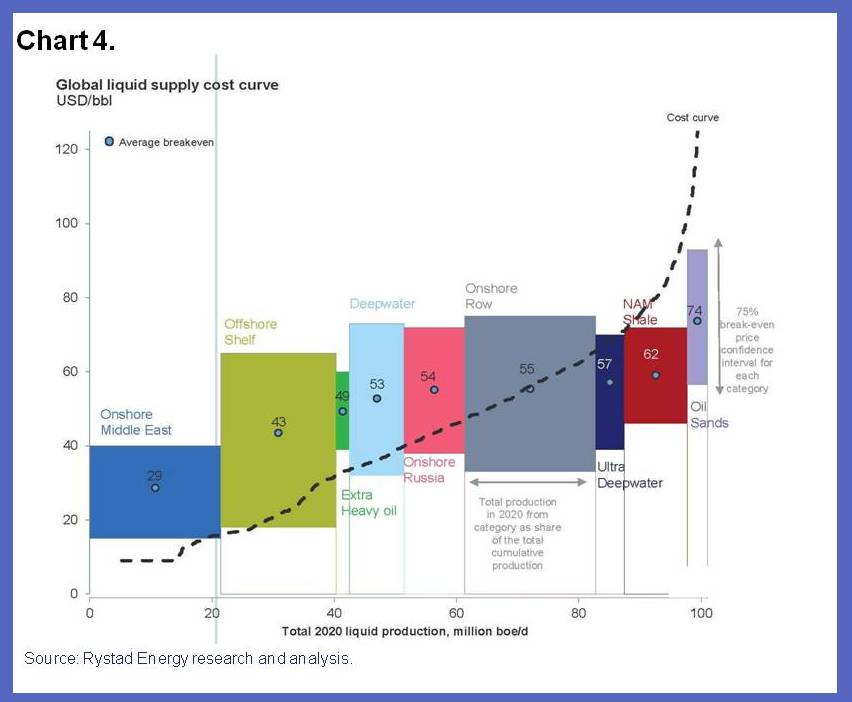

The first is whether OPEC, and in particular Saudi Arabia, will be willing to cut production in the future. This in turn depends in part on the motives behind its change in strategy, and the relative importance of geopolitical and economic factors in that decision. One hypothesis is that Saudi Arabia has found it too costly, in the face of steady increases in non-OPEC supply, to be the swing producer and maintain a high price. If so, and unless the pain of lower revenues leads other OPEC producers and Russia to agree to share cuts more widely in the future, the shift in strategy is unlikely to change soon. Another hypothesis is that it may be an attempt by OPEC to reduce profits, investment, and eventually supply by non-OPEC suppliers, some of whom face much higher costs of extraction than the main OPEC producers (see Chart 4, which gives the world marginal cost curve, showing how much it costs to produce an additional barrel by type of oil extraction).

The second factor is how investment and in turn oil production will respond to low oil prices. There is some evidence that capital expenditure on oil production has started to fall. According to Rystad Energy, overall capital expenditure of major oil companies is 7 percent lower for the third quarter of 2014 compared to 2013.

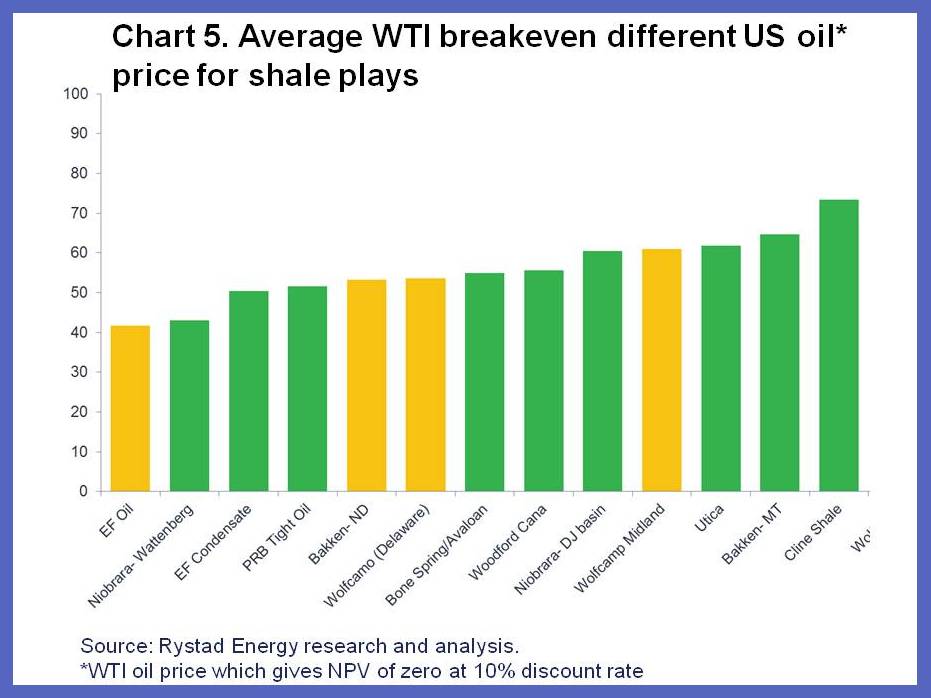

Available projections from the same source indicate that capital expenditures will fall markedly throughout 2017. For unconventional oil, such as shale, (which now accounts for 4 million out of a world supply of 93 million barrels a day), the break-even prices-the oil price at which it becomes worthwhile to extract-of the main United States shale fields (Bakken, Eagle Ford and Permian) are typically below $60 per barrel (see Chart 5 which gives break-even prices for the United States shale fields).

At current prices (around $55 per barrel), Rystad Energy's projections suggest that the level of oil production could decline but only moderately by about less than 4 percent in 2015. Rates of return will be significantly lower, however, and some highly leveraged firms that did not hedge against lower prices are already under financial stress and have been cutting their capital expenditure and laying off significantly.

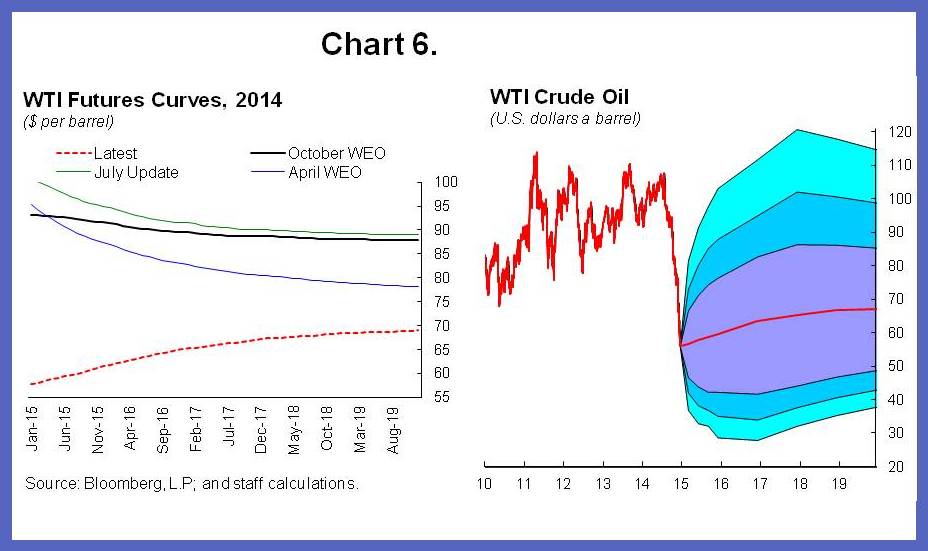

Thus, other things being equal, the dynamic effects of low prices on supply should lead to a decrease in supply relative to the initial shift and thus to a partial recovery of prices. This is what is suggested by futures markets, which show, in the left hand side panel of Chart 6, an expected recovery of prices to $73 a barrel by 2019.

The uncertainty associated with these forecasts comes not only from supply but also demand factors.

On the supply side, for example, possible changes in OPEC's strategy and geopolitical tensions in Libya, Iraq, Ukraine, and Russia should not be underestimated. On the demand side, uncertainty about global economic activity and thus the derived demand for oil remains high. This is shown, emphatically, by the size of the implied distribution of futures prices (based on options prices) in the right hand side panel of Chart 6: the 68% confidence band for the price in 2019 ranges from $48 to $85, the 95 percent band from $38 to $115; a very wide range indeed.

What are the effects likely to be on the global economy?

Overall, lower oil prices due to supply shifts are good news for the global economy, obviously with major distribution effects between oil importers and oil exporters. The crucial assumptions in quantifying the effects of those supply shifts are how large and persistent we expect them to be. These assumptions determine not only the path of adjustment, but also the initial reaction of consumers and firms.

Given the uncertainty about the relative importance of supply shifts, both now and expected in the future, we present the results of two simulations (these are ceteris paribus in nature-not projections about the global economy, and as such ignoring all other shocks likely to affect the global economy), which we see as representing a reasonable range of assumptions. The first assumes that the supply shift accounts for 60 percent of the price decline reflected in futures markets. The second also assumes that the supply shift accounts for 60 percent of the price decline at the start but that the shift is partly undone over time for the reasons described above, with its contribution to the price decline going gradually to zero in 2019.[5]

The results of the simulations shown below capture only the effects of the supply component of the oil price decline (the demand driven component of the oil price decline is a symptom of slowing global economic activity rather than a cause). The oil price projection used in the simulations is based on the IMF's price forecast, which is itself based on futures contracts.

... ... ...What are likely to be the effects on oil exporters?

As Chart 8 shows, the effect is, not surprisingly, negative for oil exporters. Here again, however, there are substantial differences across countries.

In all countries, real income goes down, and so do profits in oil production; these are the mirror images of what happens in oil importers. But the degree to which they do, and the effect of the decline in the price of oil on GDP depends very much on their degree of dependence on oil exports, and on what proportion of revenues goes to the state.

Oil exports are much more concentrated across countries than oil imports. Put another way, oil exporters depend much more on oil than oil importers.

To take some examples,

- energy accounts for 25 percent of Russia's GDP, 70 percent of its exports, and 50 percent of federal revenues.

- In the Middle East, the share of oil in federal government revenue is 22.5 percent of GDP and 63.6 percent of exports for the Gulf Cooperation Council countries.

- In Africa, oil exports accounts for 40-50 percent of GDP for Gabon, Angola and the Republic of Congo, and 80 percent of GDP for Equatorial Guinea.

- Oil also accounts for 75 percent of government revenues in Angola, Republic of Congo and Equatorial Guinea.

- In Latin America, oil contributes respectively about 30 percent and 46.6 percent to public sector revenues, and about 55 percent and 94 percent of exports for Ecuador and Venezuela.[8] This shows the dimension of the challenge facing these countries.

In most countries, a mechanical effect of the oil price decline is likely to be a fiscal deficit. One way to illustrate the vulnerabilities of oil-exporting countries is to compute the so-called fiscal break-even prices-that is, the oil prices at which the governments of oil-exporting countries balance their budgets. The breakeven prices vary considerably across countries, but they are often very high.[9]

- For Middle Eastern and Central Asian countries, the break-even prices range from $54 per barrel for Kuwait to $184 for Libya with a notable $106 for Saudi Arabia (see Chart 9).

- For countries for which we do not have available data on break-even prices, budgetary oil prices (that is, the oil prices that countries assume in preparing their budget) are another way to gauge countries' vulnerability to falling oil prices.

For Africa, those budgetary oil prices have been revised down in 2015 in light of the falling prices (See Chart 10). For Latin America, the budgetary oil prices are $79.7 for Ecuador and $60 for Venezuela.

Some countries are better equipped than in previous episodes to manage the adjustment. A few have put in place policy cushions such as fiscal rules and saving funds and have more credible monetary framework, which have helped decouple internal from external balances, such as Norway.

But, in many, the adjustment will imply fiscal tightening, lower output, and a depreciation (harder to achieve under the fixed exchange rate regimes that characterize many oil exporters). And where expectations of inflation are not well anchored, the depreciation may lead to higher inflation.

What are the financial implications?

Declines in oil prices have financial implications, directly through the effects of oil prices themselves, and indirectly through the induced adjustment of exchange rates.

Lower oil prices weaken the financial position of firms in the energy sector, especially those that have borrowed in dollars, and by implication weaken the position of banks and other institutions with substantial claims on the energy sector. The proportion of energy firms with an interest coverage ratio (the ratio of cash flows to interest payments) below 2 stands at 31 percent in emerging countries, indicating that some of these companies may indeed be at risk. CEMBI spreads, which reflect spreads on high yield emerging market corporates, have increased by 100 basis points since June.

Stress tests carried out in the context of our financial stability assessments over the past few years in a number of oil exporting countries had found only a few countries where some banks did not pass the tests, implying recapitalization needs of a few points of GDP at most. However, those stress tests results may not be very informative since the capital buffers at the time of the tests may have changed, as well as the profitability of banks. Russia is a good example of rapidly evolving conditions in both respects considering the effect of sanctions on its financial sector. Overall the impact of lower oil prices on banks in oil-exporting countries will depend critically on how persistent the fall in price is and its impact on economic activity and in turn on prevailing buffers.

Lower oil prices also typically lead to an appreciation of oil importers' currencies, in particular the dollar, and to a depreciation of oil exporters' currencies. The drop in oil price has contributed to an abrupt depreciation of currencies in a number of oil exporting countries including Russia and Nigeria. While the decrease in the price of oil is only one of the reasons behind the fall of the rouble, the Russian currency has depreciated by 40 percent so far this year, and 56 percent since September. While controlled depreciations can help oil exporters adjust, they also exacerbate financial problems for those firms and governments whose debt is denominated in dollars. And, in countries where expectations are not well anchored, uncontrolled depreciations can lead quickly to very high inflation.

If sustained, the oil price slump will thus have a concentrated and material impact on those bondholders and banks with high dollar and energy sector exposures. However, the global banking system's exposure is likely not to be large enough to cause more than a moderate increase in provisioning requirements and should be partially offset by improving credit quality in oil importing countries and sectors. Some oil importers may nevertheless have financial sector linkages to oil exporters, and may be exposed to economic and financial developments in the latter. For example, Austrian banks have significant exposure to Russia, and some have seen a very sharp decline in their equity price recently.

This relatively optimistic assessment must however come with a clear warning. One of the lessons from the Great Financial Crisis is that large changes in prices and exchange rates, and the implied increased uncertainty about the position of some firms and some countries can lead to increases in global risk aversion, with major implications for repricing of risk, and for shifts in capital flows. This is all the more true when combined with other developments such as what is happening in Russia. One cannot completely dismiss this tail risk.

Zero Hedge

Latina LoverJames_ColeAnother example of the Bankster takedown of the economy. Drive the price of oil down via naked shorts, bankrupt the domestic independent oil industry, buy their assets on the cheap, and then raise the price of oil by covering naked shorts. Wash, rinse, repeat.

The Manhattan Institute does not disclose its corporate funding, but the Capital Research Center listed its contributors as Bristol-Myers Squibb, ExxonMobil, Chase Manhattan, Cigna, Sprint Nextel, Reliant Energy, Lincoln Financial Group Foundation, and Merrill Lynch. Throughout the 1990s the tobacco industry was a major funding source for the institute.

Fed starts the bailout in...3.....2.....

Bangin7GramRocks

The jobs are temporary. Raping of the land is permanent. Sorry Mr. Roughneck, I hope you didn't overextend yourself during the boom times.

Karaio

An incandescent lamp or sun emit more energy / light before go out.

This oil boom in the US is very similar.

The great aggravating shit is the contamination of the water table.

The President gave a shot in both feet.

The first in Ukraine, the second was the agreement to lower the price of oil in Saudi Arabia.

The sons of bitches in his government did not measure consequences, thought the short term, will now have to swallow a "mush pit" - can not find a translation of this expression.

Bird eating stones knows the ass you have.

hehe.

AGuy

"According to Boone Pickens, OPEC is no longer a cartel. And we'll have $100 oil inside 18 months. I'm buying"