|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Jan | Feb | Mar | Apr | May | June | July | Aug | Sep | Oct | Nov | Dec |

|

|

|

|

This one year old selection of news. It's really funny to read forecasts that are just one year old.

Note: Despite doom and gloom stock market went from 1260 to 1460 in one year. This new stock and bonds bubble was supported by Fed.

The Washington Post

U.S. shoppers spent cautiously this holiday season, a disappointment for retailers who slashed prices to lure people into stores and now must hope for a post-Christmas burst of spending.

Sales of electronics, clothing, jewelry and home goods in the two months before Christmas increased 0.7 percent compared with last year, according to the MasterCard Advisors SpendingPulse report.

Top search terms of 2012

Google, Yahoo and Bing released their list of top search terms for 2012. Here's a recap of the year as seen through queries.

China has opened the world's longest high-speed rail line, which runs 1,428 miles from Beijing to Guangzhou.

.That was below the healthy 3 to 4 percent growth that analysts had expected - and it was the worst year-over-year performance since 2008, when spending shrank sharply during the Great Recession. In 2011, retail sales climbed 4 to 5 percent during November and December, according to ShopperTrak.

This year's shopping season was marred by bad weather and rising uncertainty about the economy in the face of possible tax hikes and spending cuts early next year. Some analysts say the massacre of schoolchildren in Newtown, Conn., earlier this month may also have chipped away at shoppers' enthusiasm.

Retailers still have time to make up lost ground. The final week of December accounts for about 15 percent of the month's sales, said Michael McNamara, vice president for research and analysis at MasterCard Advisors SpendingPulse.

Still, this season's weak sales could have repercussions for 2013, McNamara said. Retailers will make fewer orders to restock their shelves, and discounts will hurt their profitability. Wholesalers will buy fewer goods and orders to factories will likely drop in the coming months.

Steep discounts weren't enough to get people into stores, said Marshal Cohen, chief analyst at the market research firm NPD Inc.

"A lot of the Christmas spirit was left behind way back in Black Friday weekend," Cohen said, referring to the traditional retail rush the day after Thanksgiving. "We had one reason after another for consumers to say, 'I'm going to stick to my list and not go beyond it.'"

Holiday sales are a crucial indicator of the economy's strength. November and December account for up to 40 percent of annual sales for many retailers. If those sales don't materialize, stores are forced to offer steeper discounts. That's a boon for shoppers, but it cuts into stores' profits.

Spending by consumers accounts for 70 percent of overall economic activity, so the eight-week period encompassed by the SpendingPulse data is seen as a critical time not just for retailers but for manufacturers, wholesalers and companies at every other point along the supply chain.

The SpendingPulse data released Tuesday, which captures sales from Oct. 28 through Dec. 24 across all payment methods, is the first major snapshot of holiday retail sales. A clearer picture will emerge next week as retailers like Macy's and Target report revenue from stores open for at least a year. That sales measure is widely watched in the retail industry because it excludes revenue from stores that recently opened or closed, which can be volatile.

In the run-up to Christmas, analysts blamed bad weather for putting a damper on shopping. In late October, Superstorm Sandy battered the Northeast and mid-Atlantic states, which account for 24 percent of U.S. retail sales.

Shopping picked up in the second half of November, but then the threat of the country falling off a "fiscal cliff" gained strength, throwing consumers off track once again.

Lawmakers have yet to reach a deal that would prevent tax increases and government spending cuts set to take effect at the beginning of 2013. If the cuts and tax hikes kick in and stay in place for months, the Congressional Budget Office says the nation could fall back into recession.

Shopping over the past two months was weakest in areas affected by Sandy and a more recent winter storm in the Midwest. Sales declined by 3.9 percent in the mid-Atlantic and 1.4 percent in the Northeast compared with last year. They rose 0.9 percent in the north central part of the country.

The West and South posted gains of between 2 percent and 3 percent, still weaker than the 3 percent to 4 percent increases expected by many retail analysts.

Online sales, typically a bright spot, grew only 8.4 percent from Oct. 28 through Saturday, according to SpendingPulse. That's a dramatic slowdown from the online sales growth of 15 to 17 percent seen in the prior 18-month period, according to the data service.

Online sales did enjoy a modest boost after the recent snowstorm that hit the Midwest, McNamara said. Online sales make up about 10 percent of total holiday business.

Yahoo! Finance

Gary Shilling has been a long-time advocate of bonds, and he's not changing his tune as the market heads into the new year.

Stocks, up four years running, will be trying in 2013 to extend the rally that started all the way back in March 2009. But Shilling, president of economic consulting firm A. Gary Shilling & Co., says the impending recession requires investors to be cautious about equities.

"I think you play it with a 'risk-off' kind of approach," he says in an interview with The Daily Ticker. "And that means you probably look for more appreciation in long-term Treasury bonds, which have been a favorite of mine since 1981."

Shilling has been a believer in bonds for more than three decades and he's not altering that position now.

"Stocks are vulnerable," he notes. Looking ahead, he's expecting the yield on the 30-year Treasury to decline to 2% and for the yield on the 10-year note to drop to 1% from current levels.

Related: Bill Gross: Fed's "Hot Air" Will Keep Bond Bubble Afloat in 2013

Shilling isn't after yield here, so his goal is to make money from higher bond prices (bond yields move in the opposite direction of bond prices), and he's reiterating his view that a downturn is imminent.

"I've only bought Treasuries for appreciation," he says. "I couldn't care less what the yield is, as long as it's going down."

Shilling's concerned about lower corporate earnings next year, which have the potential to drag on stock prices. His worries are three-fold: A global recession will occur, hurting revenue and by extension earnings; profit margins are about as good as they can get with companies having already implemented extensive cost-cutting; a strong dollar will weigh on U.S. corporations' foreign profits and overseas operating expenses.

Shilling continues to remain bearish on the housing market because, as he sees it, the market has at least one major factor working against it.

Related: Housing Recovery Has Legs for Another 2-4 Years: Mark Zandi

"The fundamental problem with housing is still excess inventories," he says. In other words, there are too many vacant homes, whether they're being officially reported in the market or not.

"We think in total there's probably 1.9 million extra houses over and above normal working levels, and excess inventories are the mortal enemy of prices," he adds.

More from The Daily Ticker:

Bill Gross' Tips for "Beating the Wealth Tax"

Energy Prices Will Fall Next Year as Supplies Outpace Demand: Jefferies

Equities, New Tech, and Emerging Market Debt Is The Way To Go in 2013: Josh Brown

Yahoo! Finance

In 2012, investors' long-harbored suspicion that the stock market was a rigged game became something of a majority opinion.

This year, exasperation over the predominantly electronic mechanics of trading stocks, in which hyper-fast computer algorithms maneuver against one another for fractions of pennies collected over microseconds, boiled over. The level of disgust has gotten broad enough, in fact, that authorities might be prepared to rethink some of the basic rules and processes driving the system.

The opaque and complex structure for trading stocks electronically across dozens of exchanges and alternative networks has long been justified by industry leaders and regulators as the messy but logical result of investor-friendly reforms. Technology has enabled mind-melting speed, unfathomable communications capacity and brutal competition for order flow – all of which have made trading cheaper and faster than ever.

Yet by squeezing out traditional market makers who once collected low-risk, protected profits by mediating among buyers and sellers, rules and technology have tilted the power toward "high-frequency traders." And in 2012, the fragility produced by so much layered complexity became too obvious, and produced too many market-jarring failures, to be considered merely the price of progress.

A List of Failures

In March of 2012, BATS Trading, an upstart exchange that sees a large percentage of its volume from HFT firms, botched its own initial public offering. First unable to process the initial trades, BATS ultimately canceled the IPO.

In May, the Facebook (FB) initial public offering was mishandled by Nasdaq, whose systems couldn't keep up with the flood of electric orders. Many small investors just mustering the will to wade back into the market to own a piece of FB were turned off by the fiasco.

Only months later, Knight Capital Group (KCG), a premier electronic stockbroker and market maker, nearly went under when a trading-software upgrade went rogue and spewed orders without human intention or limit. Knight is now being acquired by HFT powerhouse Getco.

A process that began in 2000, when regulators and exchanges moved to quote stocks in pennies -- making it easier for automated scalpers to "improve" a quote by one cent to legally front-run real orders while reducing the amount of stock behind each bid or offer -- has now agglomerated to a point that almost no one is satisfied. A recent publication of the staid New York Society of Security Analysts declared that "public confidence in the integrity of equity trading markets appears to be at a once-in-a-generation low." This is a trend measured in the nearly $300 billion retail investors have yanked from traditional equity mutual funds since 2009.

Do Robots Really Run the Market?

But do the hyper-fast, disembodied trading robots really run the market for their own profit?

There is some irony in the fact that the public is so embittered about what they believe to be a market rigged against them, when, for most, stock trading has never been easier or less costly. For a flat $8 commission, a stay-at-home investor can instantly execute a trade in almost any stock with little noticeable friction. If, at times, an opportunistic algorithm steps ahead of that order by, say, bidding a penny more and driving the price up a couple of cents, that charge is vastly less than the 25-cent spread Nasdaq market makers used to take on almost every trade. If anything, the small investor is better served by the current trading arrangements than are large institutional investors, whose need to execute large, sensitive orders is compromised by the software spies' efforts to step in front of their trading flows.

Indeed, even the dominance of high-frequency trading, once said to participate in a sizable majority of stock orders, has passed its peak, thanks to competition and lower market volatility reducing their opportunities.

Still, somehow the opacity and bloodlessness of the automated quasi market-makers rankles more, especially when investors are less confident of unending stock market appreciation than they were in the late 1990s and early 2000s.Perception Becomes Reality

The measure of disaffection with today's market structure by both professionals and individuals means that, even if the financial impact to the typical trader isn't onerous, the sour perception in itself diminishes market quality and vitality.

And sentiment isn't helped by the ongoing round-up of alleged insider-trading conspirators among employees of major investment firms, which has made headlines that prove the authorities are paying attention while also hinting to the little guy that investing profits are often ill-gotten.

The good news in all the frustration with our tangled trading system is a renewed focus on rationalizing it. At a Senate Banking Committee hearing on electronic trading in late December, a rough consensus among exchange officials showed a desire for Congress to lay out clearer order-handling rules. The recently announced merger of electronic derivatives exchange ICE with NYSE Euronext could provide further impetus for a fresh look at the trading landscape.

Several years ago, Jim Maguire -- a NYSE floor veteran and longtime specialist for Warren Buffett's Berkshire Hathaway Inc. (BRKA, BRKB) shares -- began promoting a small but potentially helpful reform: quoting stocks in minimum increments of nickels rather than pennies. The idea was to create greater incentive for middlemen to provide a deep and fair market for public orders. Dubbed "Mr. Nickel" by Barron's, Maguire was viewed as a charming little anachronism. Yet on Feb. 5, the SEC is holding a panel discussion to discuss "the impact of tick sizes on securities markets." There is also now a more open discussion over charging high-speed traders for the massive system capacity they use.

The now deeply ingrained sense that stock trading is a game rigged by privileged sharpies with their omnipotent machines will not dissipate soon or easily. But as we enter 2013, it appears at last that those able to take action to foster greater faith in the integrity of the markets are at least focused on the issue.

Fed's Hotel California

Commentary and weekly watch by Doug NolandAt least for today (perhaps because I'm a little under the weather), when it comes to the Federal Reserve I'm about all ranted out. So this isn't supposed to be a rant, but more an effort to tie together some loose analytical ends. Key facets of my macro credit theory analysis seem to be converging: the myth of deleveraging, "liquidationist" historical revisionism, rules versus discretion monetary management, and "Keynesian"/inflationist dogma.

The Ben Bernanke Fed last week increased its quantitative easing program to monthly purchases of US$85 billion starting in January. "Operation Twist" - the Fed's clever strategy of purchasing $667 billion of bonds while selling a like amount of T-bills - is due to expire at the end of the month. The Fed will now continue buying Treasury bonds ($45 billion/month). It just won't be selling any bills, while continuing with $40 billion mortgage-backed security (MBS) purchases each month. The end result will be an unprecedented non-crisis expansion of our central bank's balance sheet (monetization). It's Professor Bernanke's "government printing press" and "helicopter money" running at full tilt.

During his Wednesday press conference, chairman Bernanke downplayed the significance of the change from "twist" to outright balance sheet inflation. Wall Street analysts have generally downplayed this as well. Truth be told, no one has a clear view of the consequences of taking the Fed's balance sheet from about $3 trillion to perhaps $4 trillion over the coming year or so. It's worth noting that in previous periods of rapid balance sheet expansion, the Fed was essentially accommodating de-leveraging by players (hedge funds, banks, proprietary trading desks, real estate investment trusts, etc) caught on the wrong side of a market crisis.

Does the Fed's next trillion's worth of liquidity injections spur more speculation in bonds, stocks and global risk assets? Or, instead, will our central bank again provide liquidity for leveraged players looking to sell (many increased holdings with the intention of eventually offloading to the Fed)? It's impossible to know today the ramifications of the Fed's latest tack into uncharted policy territory. It will stoke some inflationary consequence no doubt, although the impact on myriad credit bubbles around the globe is anything but certain.

Clearer is that the Fed has again crossed an important line. There has been previous talk of Fed "exit strategies". I'll side with Richard Fisher, president of the Federal Reserve Bank of Dallas, who on Friday warned of "Hotel California" risk ("... Going back to the Eagles song which is, 'you can check out any time you want but you can never leave... '"). There has also been this notion that the US economy is progressing through a ("beautiful") deleveraging process.

Yet there should be little doubt that the Fed has now resorted to blatantly orchestrating a further leveraging of the US economy. It will now become only that much more difficult (think impossible) for the Federal Reserve to extricate itself from this inflationary process.

I've read quite sound contemporaneous analysis written during the "Roaring Twenties". There was keen appreciation at the time for the risks associated with rampant credit growth and speculative excesses throughout the markets and economy. The "old codgers" argued that a massive credit inflation that commenced during the Great War (World War I) was being precariously accommodated by loose Federal Reserve policies. Chairman Bernanke has throughout his career disparaged these "bubble poppers".

To this day the "liquidationists" are pilloried for their view that there was no viable alternative than to wring financial excess and economic maladjustment out of the system through wrenching adjustment periods. Through their empirical studies, quantitative models, and sophisticated theories, contemporary academics - led by Bernanke - have proven (without a doubt!) that the misguided "bubble poppers" and "liquidationists" were flat out wrong. Our central bankers are now determined to prove them (along with their contemporary critics) wrong in the real world. Yet there remains one rather insurmountable dilemma: The contemporaneous credit bubble antagonists were right.

The Dallas Fed's Fisher stated Friday that the rate-setting Federal Open Market Committee "is probably the most academically driven in history". Well, I'll say that a world of unconstrained market-based finance "regulated" by inventive and activist academics has proved one explosive monetary concoction. The Wall Street Journal's Jon Hilsenrath (with Brian Blackstone) had two insightful pieces this week, "MIT Forged Activist Views of Central Bank Role and Cinched Central Banker Ties", and "World Central Bankers United by Secret Basel Talks and MIT Connections".

Inflationary cycles always create powerful constituencies. After all, credit booms and the government printing press provide incredible wealth-accumulating opportunities for certain segments of the economy. Moreover, it is the nature of things that late in the cycle the pace of wealth redistribution accelerates as the monetary inflation turns more unwieldy. Throw in the reality that asset inflation (financial and real) has been a prevailing inflationary manifestation throughout this extraordinary credit boom, and you've guaranteed extraordinarily powerful constituencies.

By now, "activist" central banking doctrine - with pegged rates, aggressive market intervention/manipulation and blatant monetization - should already have been discredited. Instead, policy mistakes lead to only bigger policy mistakes, just as was anticipated generations ago in the central banking "Rules vs Discretion" debate.

Today, a small group of global central bank chiefs can meet in private and wield unprecedented power over global markets, economies and wealth distribution more generally. They are said to somehow be held accountable by politicians that have proven even less respectful of sound money and credit. In the US, Europe, the UK, Japan and elsewhere, central bankers have become intricately linked to fiscal management. As such, disciplined and independent central banking, a cornerstone to any hope for sound money and credit, has been relegated to the dustbin of history.

Considering the global monetary policy backdrop, it's not difficult to side with the view of an unfolding inflation issue. At the same time, the "liquidationist" perspective - that to attempt sustaining highly inflated market price and economic structures risks financial and economic catastrophe - has always resonated.

The markets' response to Wednesday's dramatic Fed announcement was notably underwhelming. This could be because it was already discounted. Perhaps "fiscal cliff" worries are restraining animal spirits. Then again, perhaps the more sophisticated market operators have been waiting for this opportunity to reduce their exposures. After all, the Fed moving to $85 billion monthly of quantitative easing five years into an aggressive fiscal and monetary reflationary cycle is pretty much an admission of defeat.

I've argued that, primarily due to unrelenting fiscal and monetary stimulus, the US economy has been avoiding a necessary deleveraging process. Some highly intelligent and sophisticated market operators have argued the opposite. They point to growth in incomes and gross domestic product, while total (non-financial and financial) system credit has contracted marginally. I can point specifically to total non-financial debt that closed out 2008 at $34.441 trillion and ended September 30, 2012, at a record $39.284 trillion. But the deleveraging debate will not be resolved with data.

The old "liquidationists" (and "Austrians") would have strong views about contemporary "deleveraging". They would shout "inflated price levels", "non-productive debt", "unsupportable debt loads", "excess consumption", "distorted spending patterns and associated malinvestment", "deep economic structural imbalances" and "intractable current account deficits!" They would argue that to truly "deleverage" one's economy would require a tough weaning from system credit profligacy.

Only by consuming less and producing more can our economy reduce its debt dependency and get back on a course toward financial and economic stability. The "bubble poppers" would profess that in order to commence a sustainable cycle of sound credit and productive investment first requires a cleansing ("liquidation") of unproductive ventures and unserviceable debts. It's painful and, regrettably, shortcuts only short-circuit the process. I'm convinced that they would hold today's so-called "deleveraging" - replete with massive deficits, central bank monetization and ongoing huge US trade deficits - in complete and utter disdain.

In a CNBC interview on Wednesday evening, the Wall Street Journal's Jon Hilsenrath called Bernanke a "gunslinger". Our Fed chairman is highly intelligent, thoughtful, polite, soft-spoken, seemingly earnest and a huge, huge gambler. And he's not about to fold a bad hand. Almost four years ago, I wrote that Fed reflationary measures were essentially "betting the ranch". This week they again doubled down.

With his perspective and theories, Bernanke has pushed the envelope his entire academic career. He is now surrounded by a group of likeminded "Keynesian" academics, and they together perpetuate groupthink in epic proportions. These issues will be debated for decades to come - and who knows how that will all play out.

But as a contemporary analyst and keen observer, there's no doubt these unchecked "academics" are operating with dangerously flawed theories and doctrine. It's not the way central banking was supposed to work. Ditto capitalism and democracies. Whatever happened to sound money and credit?

The following CNBC guest blog is from Mohamed El-Erian, the CEO and Co-CIO of PIMCO, which oversees nearly $1.8 trillion in assets and runs the Pimco Total Return Fund, the largest bond fund in the world.

Here is a simple way to think about the political calculus of Washington's latest twists and turns. And -- unfortunately -- it suggests that economic and market dislocations may be needed to get our politicians to cooperate and govern properly.

A major issue from day one was the extent to which the lack of trust between our political parties undermined Washington's ability to govern. (Read More: Boehner Says GOP Open to Deal; Congress Breaks)

Hoping to resolve this problem and thus deliver consensus, party leaders opted in the summer of 2011 for a very big stick: threaten the country with a major economic setback as a way to get the rank and file of both parties to cooperate.

This, of course, was the strategic underpinning of the fiscal cliff: By designing large and blunt spending cuts and tax hikes that would automatically go into effect, and thus push the country into a costly recession, political leaders hoped to impose compromise among bickering and dithering politicians - particularly among those with very different views of the past, present and future.

The stick succeeded in catalyzing serious negotiations between President Obama and House Speaker Boehner. But the stick was not big enough to overcome differences and force a cooperative outcome. And with Republicans facing the bigger risk of being blamed by the country for the failure, Speaker Boehner opted for his Plan B.

Now the situation has taken an even more interesting turn.

The Speaker's inability Thursday to unite Republicans behind his plan highlights the extent to which mutual trust is also seriously lacking WITHIN the political parties - and not just between them. This meaningfully complicates the cooperative solution. (Read More: Boehner Abruptly Scraps 'Plan B' Vote in Setback)

How about the future?

Let us start with the obvious. In order to avoid a recession that would aggravate the country's unemployment problem and reignite concerns about housing and household finances, Democrats and Republicans need quickly to find a way to work together. While possible, it is hard to see how this happens endogenously. There are lots of divisions, and at many levels.

If an internal resolution mechanism is indeed lacking, than cooperation will need to be forced by an outside event. This is where economic and market volatility comes in.

Thursday's collapse of Speaker Boehner's Plan B unfortunately makes it more likely that the fiscal cliff may materialize, constituting a blow to a recovering US economy. Absent some last minute messy deal that buys a few weeks at best, that would constitute stage one.

The question about stage two is how much time do political parties then need to find a solution and avoid a bigger economic and financial implosion.

The 2008 experience with TARP - where the market and economic dislocations that followed the initial congressional vote rejection quickly forced politicians to cooperate - suggests that there is nothing like visible turmoil to get our bickering political parties to come together properly in the national interest.

Let us hope that the political system responds in a similar fashion in the coming weeks, if not earlier. There is a lot at stake.

Sen. Dick Durbin (D-Ill.) has been battling the banks the last few weeks in an effort to get 60 votes lined up for bankruptcy reform. He's losing.

On Monday night in an interview with a radio host back home, he came to a stark conclusion: the banks own the Senate.

"And the banks -- hard to believe in a time when we're facing a banking crisis that many of the banks created -- are still the most powerful lobby on Capitol Hill. And they frankly own the place," he said on WJJG 1530 AM's "Mornings with Ray Hanania." Progress Illinois picked up the quote.

Earlier Wednesday, Senate Majority Leader Harry Reid (D-Nev.) told the Huffington Post that the most important provision of bankruptcy reform -- the authority for a bankruptcy judge to renegotiate mortgages, known as cramdown, which banks strongly oppose -- could get ripped out of the bill. Speaker Nancy Pelosi (D-Calif.) pushed back, saying that a bill without such a provision wouldn't be reform at all.

While Durbin has been negotiating with individual banks over the last several weeks, bank lobbyists and Senate Minority Whip Jon Kyl (R-Ariz.) have been whipping up opposition to it. A growing number of Democrats have announced opposition to cramdown, including Ben Nelson (Neb.), Mary Landrieu (La.) and Jon Tester (Mont.).

"There's been a tendency on the part of some who are advocates for the legislation to overestimate the number of votes in favor," said Sen. Evan Bayh (D-Ind.). "When I was actively involved at the moment it broke down it was my impression there were no Republicans who were willing to support it and at least a few Democrats have stated openly on the record that they were in opposition. How you get to 60 with those numbers is a mathematical problem."

By BRUCE BARTLETT, The Fiscal Times

December 21, 2012

Many on the left are puzzled by Barack Obama's apparent willingness to support dramatic reductions in federal social spending. It is only because Republicans demand even more radical cuts in spending that Obama's fiscal conservatism is invisible to the general public. But those on the political left know it and are scared.Yesterday, left-leaning law professor Neil Buchanan penned a scathing attack on Obama for abandoning the Democratic Party's long-held policies toward the poor, and for astonishing naiveté in negotiating with Republicans. Said Buchanan:

"The bottom line is that President Obama has already revealed himself to be unchanged by the election and by the last two years of stonewalling by the Republicans. He still appears to believe, at best, in a milder version of orthodox Republican fiscal conservatism – an approach that would be a fitting starting position for a right-wing politician in negotiations with an actual Democrat. Moreover, he still seems to believe that the Republicans are willing to negotiate in good faith."

Others on the left, such as New York Times columnist Paul Krugman, former Secretary of Labor Robert Reich and others raise similar concerns. They cannot understand why Obama, having won two elections in a row with better than 50 percent of the vote – something accomplished only by presidents Dwight Eisenhower and Ronald Reagan in the postwar era – and holding a powerful advantage due to the fiscal cliff, would seemingly appear willing to gut social spending while asking for only a very modest contribution in terms of taxes from the wealthy.

The Fiscal Times FREE Newsletter

The dirty secret is that Obama simply isn't very liberal, nor is the Democratic Party any more. Certainly, the center of the party today is far to the right of where it was before 1992, when Bill Clinton was elected with a mission to move the party toward the right. It was widely believed by Democratic insiders that the nation had moved to the right during the Reagan era and that the Democratic Party had to do so as well or risk permanent loss of the White House.

It is only the blind hatred Republicans had for Clinton that prevented them from seeing that he governed as a moderate conservative – balancing the budget, cutting the capital gains tax, promoting free trade, and abolishing welfare, among other things. And it is only because the political spectrum has shifted to the right that Republicans cannot see to what extent Obama and his party are walking in Clinton's footsteps.

One of the few national reporters who has made this point is the National Journal's Major Garrett. In a December 13 column, he detailed the rightward drift of the Democratic Party on tax policy over the last 30 years.

"In ways inconceivable to Republicans of the 1970s, 1980s, and 1990s, Democrats have embraced almost all of their economic arguments about tax cuts. Back then, sizable swaths of the Democratic Party sought to protect higher tax rates for all. Many opposed President Reagan's 1981 across-the-board tax cuts and the indexing of tax brackets for inflation. Many were skeptical of Reagan's 1986 tax reform that consolidated 15 tax brackets into three and lowered the top marginal rate from 50 percent to 28 percent (with a "bubble rate" of 33 percent for some taxpayers). They despised the expanded child tax credit and marriage-penalty relief called for under the GOP's Contract With America.

"Now all of that is embedded in Democratic economic theory and political strategy. The only taxes that the most progressive Democratic president since Lyndon Johnson wants to raise are those affecting couples earning more than $267,600 and individuals earning more than $213,600 (these are the 2013 indexed amounts from President Obama's 2009 proposal of $250,000 for couples and $200,000 for individuals). Yes, some of this increase would hit some small businesses. But that can be finessed."

I think that a lot of the Democratic Party's rightward drift resulted from two factors.

- First is the continuing decline of organized labor from 24 percent of the labor force in 1973 to less than half that percentage in 2011. And the decline among private sector workers has been even more severe. When the AFL-CIO was strong, it looked out for the working class as a whole. Its leadership understood that improving the pay and benefits of all workers was ultimately to the benefits of unionized workers. Labor support was critical to the passage of every important piece of social welfare legislation since the 1930s. Hence the decline of unionization has deprived liberals of their most important ally.

- Secondly, the collapse of the Soviet Union essentially led to the collapse of support for socialism worldwide. I think voters bought the idea that the economist F.A. Hayek made during World War II that socialism impoverishes people and necessarily becomes totalitarian eventually. The disappearance of socialism as a viable political philosophy deprived liberals of their ideological anchor, causing liberalism itself to drift rightward with the tide.

There are other factors as well, such as the dependence of Democrats on campaign contributions from Wall Street, but I think these are the most important. But whatever the reason, the result is that the nation no longer has a party of the left, but one of the center-right that is akin to what were liberal Republicans in the past – there is no longer any such thing as a liberal Republican – and a party of the far right.

In a little-noticed comment on Spanish-language television on December 14, Obama himself confirmed this typology of today's political spectrum. Said Obama,

"The truth of the matter is that my policies are so mainstream that if I had set the same policies that I had back in the 1980s, I would be considered a moderate Republican."

I think this is correct and explains a great deal about why Obama refuses to use his leverage to pursue liberal policies and keeps inviting Republicans back to the negotiating table again and again on the budget. He wants a deal, he wants to cut spending and balance the budget if possible. This may or may not be a wise course for a Democratic president to follow, but that is who Obama is.

I think Justin Wolfer's claim that there are now three parties, the Democrats, the Republicans, and the Tea Party, at odds in the House is correct. That appears to be working in the president's favor, at least for the moment:

Playing Taxes Hold 'Em, by Paul Krugman, Commentary, NY Times: A few years back, there was a boom in poker television - shows in which you got to watch the betting and bluffing of expert card players. Since then, however, viewers seem to have lost interest. But I have a suggestion: Instead of featuring poker experts, why not have a show featuring poker incompetents - people who fold when they have a strong hand or don't know how to quit while they're ahead?On second thought, that show already exists. It's called budget negotiations, and it's now in its second episode.

The first episode ran in 2011, as President Obama made his first attempt to cut a long-run fiscal deal - a so-called Grand Bargain... Mr. Obama was holding a fairly weak hand... The deal, if implemented, would have been a huge victory for Republicans... But ... Mr. Boehner and members of his party couldn't bring themselves to accept even a modest rise in taxes. And their intransigence saved Mr. Obama from himself.

Now the game is on again - but with Mr. Obama holding a far stronger hand. ...

Yet earlier this week progressives suddenly had the sinking feeling that it was 2011 all over again, as the Obama administration made a budget offer that .. involved giving way on issues where it had promised to hold the line... Are we about to see another round of the president negotiating with himself, snatching policy and political defeat from the jaws of victory?

Well, probably not. Once again, the Republican crazies ... have saved the day. ... Mr. Boehner had evident problems getting his caucus to support Plan B, and he took the plan off the table Thursday night; it would have modestly raised taxes on the really wealthy, the top 0.1 percent, and even that was too much for many Republicans. ...

As in 2011, then, the Republican crazies are doing Mr. Obama a favor, heading off any temptation he may have felt to give away the store in pursuit of bipartisan dreams.And there's a broader lesson... This is no time for a Grand Bargain, because the Republican Party, as now constituted, is just not an entity with which the president can make a serious deal. If we're going to get a grip on our nation's problems ... the power of the G.O.P.'s extremists, and their willingness to hold the economy hostage if they don't get their way, needs to be broken. And somehow I don't think that's going to happen in the next few days.

[Dec 19, 2012] He also points to the SPDR S&P Emerging Markets Dividend fund (EDIV), which carries a 6.9% yield and all the upside (and of course downside too) that the developing markets may bring.

One of the traits that made Ron Popeil one of the greatest salesmen of all time was his ability to make a product seem better and better. Just when you thought the case for owning a particular gadget couldn't possibly get any better, Popeil would deliver his famous line, "but wait -- there's more," and further compel you to reach for your wallet.

While speaking with Tom Lydon, editor of ETFtrends.com, I had a Ron Popeil moment. Lydon's latest investment strategy seemed to be bordering on too-good-to-be-true. Not only is he making the case for the outsized growth opportunity that is available from Emerging Markets in an otherwise lackluster world, but in the attached video he's also working in a way that let's you get paid while you wait.

Emerging market countries and companies, Lydon points out, are often in much better shape than than their counterparts in the U.S. and Europe. "Oh and by the way, they're making a lot of money and kicking off some pretty good dividends too," he adds.

Ten years ago, iShares MSCI Emerging Markets (EEM) used to be the place "for your speculative money," but Lydon says that has changed. In fact he says 55% of global market cap comes from outside the U.S., not to mention mention most of the world's GDP growth.

"If you can get on average four, five, and in some cases, 6% dividend yield while you're waiting for global markets to get traction; not a bad yield."

One such fund that seeks this sort of hybrid return is the Wisdom Tree Emerging Markets Equity Income (DEM), which Lydon says utilizes an automated stock picking process that adds the top 1/3 of dividend payers annually to their portfolio.

He also points to the SPDR S&P Emerging Markets Dividend fund (EDIV), which carries a 6.9% yield and all the upside (and of course downside too) that the developing markets may bring.

While some have questioned the impact that pending tax changes might have on dividend paying stocks domestically, Lydon falls into the ''they'll be fine'' camp, based upon his belief that the demand for income won't go away and the reality that as much as half of all dividend paying stocks are currently held in tax-sheltered accounts, so an increase would not be felt anyways.

"Six months from now, we're going to be passed all of this and what are we going to be looking for?" he asks, "some of the same the things we're looking for today."

We are going to learn quite a bit about America over the next eighteen months. This talk gives us a framework in which to place certain events.

Models Behaving Badly by Robert Skidelsky

"Why did no one see the crisis coming?" Queen Elizabeth II asked economists during a visit to the London School of Economics at the end of 2008. Four years later, the repeated failure of economic forecasters to predict the depth and duration of the slump would have elicited a similar question from the queen: Why the overestimate of recovery?Consider the facts. In its 2011 forecast, the International Monetary Fund predicted that the European economy would grow by 2.1% in 2012. In fact, it looks certain to shrink this year by 0.2%. In the United Kingdom, the 2010 forecast of the Office for Budget Responsibility (OBR) projected 2.6% growth in 2011 and 2.8% growth in 2012; in fact, the UK economy grew by 0.9% in 2011 and will flat-line in 2012. The OECD's latest forecast for eurozone GDP in 2012 is 2.3% lower than its projection in 2010.

Likewise, the IMF now predicts that the European economy will be 7.8% smaller in 2015 than it thought just two years ago. Some forecasters are more pessimistic than others (the OBR has a particularly sunny disposition), but no one, it seems, has been pessimistic enough.

Economic forecasting is necessarily imprecise: too many things happen for forecasters to be able to foresee all of them. So judgment calls and best guesses are an inevitable part of "scientific" economic forecasts.

But imprecision is one thing; the systematic overestimate of the economic recovery in Europe is quite another. Indeed, the figures have been repeatedly revised, even over quite short periods of time, casting strong doubt on the validity of the economic models being used. These models, and the institutions using them, rely on a built-in theory of the economy, which enables them to "assume" certain relationships. It is among these assumptions that the source of the errors must lie.

Two key mistakes stand out. The models used by all of the forecasting organizations dramatically underestimated the fiscal multiplier: the impact of changes in government spending on output. Second, they overestimated the extent to which quantitative easing (QE) by the monetary authorities – that is, printing money – could counterbalance fiscal tightening.

Until recently, the OBR, broadly in line with the IMF, assumed a fiscal multiplier of 0.6: for every dollar cut from government spending, the economy would shrink by only 60 cents. This assumes "Ricardian equivalence": debt-financed public spending at least partly crowds out private spending through its impact on expectations and confidence. If households and firms anticipate a tax increase in the future as a result of government borrowing today, they will reduce their consumption and investment accordingly.

On this view, if fiscal austerity relieves households of the burden of future tax increases, they will increase their spending. This may be true when the economy is operating at full employment – when state and market are in competition for every last resource. But when there is spare capacity in the economy, the resources "freed up" by public-sector retrenchment may simply be wasted.

Forecasting organizations are finally admitting that they underestimated the fiscal multiplier. The OBR, reviewing its recent mistakes, accepted that "the average [fiscal] multiplier over the two years would have needed to be 1.3 – more than double our estimate – to fully explain the weak level of GDP in 2011-12." The IMF has conceded that "multipliers have actually been in the 0.9 and 1.7 range since the Great Recession." The effect of underestimating the fiscal multiplier has been systematic misjudgment of the damage that "fiscal consolidation" does to the economy.

This leads us to the second mistake. Forecasters assumed that monetary expansion would provide an effective antidote to fiscal contraction. The Bank of England hoped that by printing £375 billion of new money, ($600 billion), it would stimulate total spending to the tune of £50 billion, or 3% of GDP.

But the evidence emerging from successive rounds of QE in the UK and the US suggests that while it did lower bond yields, the extra money was largely retained within the banking system, and never reached the real economy. This implies that the problem has mainly been a lack of demand for credit – reluctance on the part of businesses and households to borrow on almost any terms in a flat market.

These two mistakes compounded each other: If the negative impact of austerity on economic growth is greater than was originally assumed, and the positive impact of quantitative easing is weaker, then the policy mix favored by practically all European governments has been hugely wrong. There is much greater scope for fiscal stimulus to boost growth, and much smaller scope for monetary stimulus.

This is all quite technical, but it matters a great deal for the welfare of populations. All of these models assume outcomes on the basis of existing policies. Their consistent over-optimism about these policies' impact on economic growth validates pursuing them, and enables governments to claim that their remedies are "working," when they clearly are not.

This is a cruel deception. Before they can do any good, the forecasters must go back to the drawing board, and ask themselves whether the theories of the economy underpinning their models are the right ones.

12 December 2012

Gold Daily And Silver Weekly Charts - FOMC and 12-12-12

The Fed did the completely expected today, pledging to continue to expand its balance sheet in buying sovereign and mortgage debt at the pace of $85 billion per month until unemployment drops below 6.5% and/or inflation rises above 2.5%.Considering that both measures are tacitly rigged and phony, that pretty much means that Benny will print until the exhaustion and collapse of the dollar, or until it suits their interests not to do it.

The only surprise in Benjy's press conference was that he grew up in rural South Carolina and goes back for visits. I didn't see that one coming.

The money shot today was when the male spokesmodel on Bloomberg said 'and gold is up only five dollars after that Fed announcement.' All that capping just to try and make the impression that QE until hell freezes over isn't inflationary? I hope it was worth it.

Stocks pulled back from the necklines on their inverse head and shoulders, and gold and silver rallied back, but the pop higher was pale in context because of the pounding the metals had taken for the past week. There were no big drops, but lots of cheap shots and quick hits.

So what next. It's all fiscal cliff now, all the time, until the end of the year. Or the real Mayan calendar end date, which is not 12-12-12 like so many think. It is 21 December 2012, which is also the last date by which legislation can be submitted to the US Congress for consideration this year. So if you are planning on the end the world, its time to RSVP.

I really cannot say what these fiscal cliff jokers are going to do, but I do know that Obama has the whip hand, even if it was ten years in the making, and after the previous twenty times that the Republicans used and abused his good will gestures in negotiating against himself, he is likely to let it ride.

The cliff is phony anyway, although I am sure it will be used as a looting opportunity on Wall Street.

Once the cliff passes, 70% of the deficit evaporates. Horrors! And they have plenty of time to tweak it in the new Congress so the effects are very unlikely to be lasting.

I am almost positive the US is heading into a recession next year anyway, the policy decisions are so cockeyed against the median wage earner and consumer. They might try and hide it by throwing money at it, and there lies stagflation, even if they hide the inflationary part.

El Cliffo Fiscal gives the Republicans political cover, because now the tax cuts expire and they cannot be blamed for raising taxes. So Grover and his bully boys cannot be madder than usual that they are not warlords in Somalia rather than citizens in a Republic. And then the Republicans can cut a deal and lower taxes somewhat and look like heroes.

I don't have a lot of confidence (lot = greater than zero) in Obama and the Dems making a decent deal for the American people. The Republicans are whores for the monied interests and are as bad or worse. I think it was Gore Vidal who said that the Dems and GOP are just two different wings of the Big Money Party, and that sounds about right.

So let's see what happens.

In the short term, the short side of a hedged stock/bullion pair seems like the thing to do.

Modern Monetary Theory And Its Toolbox

12 December 2012 | Jesse's Café AméricainI think the essay excerpted at the bottom is a 'must read.' If you do not have time for this intro, please read it.

On the surface Modern Monetary Theory can seem to be an attractive proposition. And it troubles me that some people whom I like and even admire seem to be favorable to it. After a great deal of thought it appears to be the situation in which the cure is as bad as the disease, with reformers driven to pick up the tools of desperation and what looks like a quick fix.

The key objection one would naturally raise in considering Modern Monetary Theory is the protection of the value of the currency. Domestically the use of official force is an obvious if unfortunate reach. The real issue of acceptance of the currency at value comes down particularly in foreign trade where one cannot so easily enforce draconian rules designed to promote the value of the currency to some official prescription.

A short term solution is to maintain and expand your sphere of command and control until it overextends, fails, and collapses. We have seen how this worked out in the former Soviet Union.

Foreign holders have the 'right of first refusal' on debt and currency. It is almost a tautology to say that most serious instance of inflation, including hyperinflation, start outside that country.

Often people are attracted to the principles of Modern Monetary Theory because it sounds 'ethical' and fair. Why pay interest on debt to evil bankers when you can merely print your own money? Never mind that most debt is held by private people as savings vehicles, in theory at least. The current balance of trade problems and surpluses held by some foreign countries are policy aberrations. Free trade is a canard that suits multinational interests, but that is another story.

As I have said before, I do not intend to justify the current financial system which is distorted and corrupt. No system is perfect and self-regulating, but some are more prone to corruption than others.

I do wish to point out that any currency system must have some balance, some limiting factor, that is difficult for people to circumvent with respect to the expansion of the currency. A commodity standard like gold is one, since gold cannot be created. A debt based central banking approach is another, because the marketplace has some immediate ability to react to expansionary policies.

A concentration of power in few hands leads invariably to corruption and abuses.

But rather than belabor this, here is an excerpt from a recent essay from 'New Economic Perspectives' on Modern Monetary Theory. There is no need to debate this when one can merely peel back the fog of supposition and let it speak in its own words beyond the surface gloss.

The management mechanisms in the MMT toolbox are central economic planning to a far greater degree than we currently see in most developed nations, government allocation of resources, distribution of income at will, official propaganda (and presumably censorship) since the lie will tolerate none other, and foreign currency controls.

There is a juicy worm on the end of hook, but there is a hook in there nonetheless. I have read and listened to most of their spiels, to the extent that one can work their way past the browbeating and obfuscation that true believers like to deliver to doubters. I do not wish to be 'mean' but to me it seems to be an old fairy tale fraud in a new wrapper.

An Alternative Meme for Money, Part 6: Alternative Framing on Inflation

By L. Randall WrayAs we have discussed, sovereign government cannot run out of the keystrokes it uses to mark-up balance sheets as it spends...Obviously, government cannot run out of these. Government can "afford" to buy what's for sale in its own currency.

The question is not about affordability but rather concerns effects on the value of the currency and impacts on the pursuit of private interest.

a. If something is in scarce supply, more purchases of it by either government or private buyers might push up the price. A government purchase of something that is scarce can "crowd out" a private purchase. Government purchases need to be, and can be, planned to avoid undesired crowding out and price pressures.We never need rich folks' money in order to provide for the poor. We can keystroke the bank accounts of the poor so that they won't be poor. We increase taxes on the rich only when their spending threatens our currency with inflation. If there's no inflation danger, there is no point in taxing the rich before keystroking the poor.b. ...government has at its disposal a number of options to reduce price pressure, including patriotic propaganda and rationing. It also has the big gun: taxes. An excise tax raises the cost to private buyers; an income tax reduces disposable income to free up production for the public purpose.

The rich also are much more likely to endanger the currency's value by pulling out of the domestic currency and running to safe havens at the first sign of inflation... We need progressive taxes and inheritance taxes to protect our currency from antisocial behavior by the rich.

Most important: the goal of taxing the rich has nothing to do with raising government revenue. Taxes are used to keep the currency strong and to punish sin. An ideal sin tax raises no revenue because it eliminates sin. While we cannot achieve that ideal, we can make sin less enjoyable. It is fitting that those who already enjoy all the benefits of life at the top ought to suffer more when they are sinful...

To conclude:

1. When inflation threatens, in some circumstances it makes sense to raise taxes. Since the rich pose a greater inflation threat, put the taxes on them. Cash registers don't discriminate, so tax those with greater purchasing power.2. There are additional measures that can be taken when inflation pressures arise; depending on circumstances, they are probably more effective: rationing, targeted wage and price controls, patriotic saving.

3. At full employment it makes sense to tax the rich while providing income to the poor. At less than full employment, this is not necessary.

4. Government spending and taxing need not be closely linked; however, as the economy nears full employment taxes need to be raised if there are strong public purpose interests in continuing to increase government spending. The goal is not to increase government revenue, but to reduce competition for relatively scarce resources in order to direct them to the public interest.

5. Not only does the high income and thus potential spending by the rich threaten domestic value of the currency, there is a danger that the rich will speculate against the currency. This provides an additional justification for removing excessive income from them through taxes, and perhaps also for taxing their speculation. Again, the goal here is not to raise government revenue, but rather to punish the sin of anti-social excess.

6. Explaining that government cannot run out of its own keystrokes (or other records of its IOUs) does not mean that one is promoting run-away government spending. Rather, it means that one must confront the inflation danger directly, ensuring that government spending and tax policy take account of inflation pressures.

Read the entire essay here.

ShareMore From this Author

A Vikram Pandit Reality CheckAndrew Burton/Getty Image News

You can be forgiven if you watched the Department of Justice's announcement yesterday of a $1.92 billion settlement with HSBC with a sense of disappointment--and déjà vu. The event checked all the boxes in a theatrical routine that has become all too familiar.Descriptions of breathtaking misconduct involving the facilitation of massive drug trafficking and transactions with rogue terror-sponsoring nations? Check.

Broad boasts about the "historic" nature of the settlement that will certainly end the type of criminal misconduct alleged? Check.

Mea culpas from the offending institution with promises that it has really learned its lesson this time and will never ever engage in dastardly conduct again? Yep, that too.

Nothing, however, was quite as it appeared. Sure, HSBC paid a record fine, but there was something vitally important missing from yesterday's press conference: actual criminal charges for obvious criminal conduct.

Some perspective: HSBC sent more than $800 million in bulk cash from Mexico to the United States, a good chunk of which apparently represented proceeds from some of the most notorious Colombian drug cartels. As someone who tried the first narcotics money laundering case involving extradition from Colombia, let me assure you that this is a lot of money, the discovery of which usually generates vigorous prosecutions and lengthy prison sentences. And it wasn't HSBC's only dirty business: There were also hundreds of millions of more dollars of illegally disguised transactions with rogue nations such as Iran and Sudan.

Why no criminal charges? Why instead only some remedial measures and a "historical" fine that can be measured in weeks -- not years -- of earnings? It certainly wasn't for lack of evidence. No, instead the government determined that HSBC is not only too big to fail, but also too big to jail. As the New York Times first reported, even though there were strong voices within DOJ pushing for criminal charges, the big banks' best friends within the government (the Treasury Department, of course, and other unnamed regulators) were too fearful that an indictment could destabilize the global financial system. Yes, it's 2008 all over again. In the name of systemic stability, a megabank again escapes accountability for its actions, rescued by compliant officials.

In some aspects, DOJ's surrender is understandable. Notwithstanding regulatory reform efforts in the U.S. and the UK, the largest banks are in many ways even more systemically dangerous today than when we bailed them out in 2008. This indirect acknowledgment that we have failed to fix the too-big-to-fail problem has potentially dire consequences.

One of the reasons why we have a criminal justice system, of course, is to deter criminal behavior. If you know that you will be punished for putting your hand in the cash register at your local supermarket (or illegally stripping out information from a monetary transaction that identifies the source nation as Iran), you are less likely to do so. But if the government offered a blanket waiver from criminal accountability for a certain group -- let's say all left-handed people over six feet tall or a handful of banks deemed so large and so significant that their indictment could destroy the global financial system -- we would expect that those exempted would no longer be deterred from committing criminal acts. And although lefty giants may otherwise lack a predisposition for boosting cash, in recent years the largest banks have demonstrated an unbridled zeal for pushing the boundaries of the law as part of their relentless pursuit of profits. DOJ's actions with regards to HSBC are beyond unfair: They are downright terrifying for weakening the general deterrence for megabanks, both foreign and domestic, which could rationally interpret yesterday's actions as a license to steal.

The enduring presumption of bailouts in our banking system already drives the largest banks to take on too much risk with too little disclosure and too much leverage, a toxic cocktail that will inevitably lead to another financial crisis. Yesterday's action now spikes the punch with a new toxin, confirmation that criminal penalties are off the table, leaving a worst-case scenario of a fine totaling far less than even a single quarter's earnings. Given the potential profits of criminal behavior and the unlikelihood of personal consequences for the executives directing it, the message is clear: Crime pays. This will inevitably lead to more reckless risk-taking that will further undermine systemic stability and lead to an even greater financial meltdown down the road.

There is, of course, a solution for our emerging two-tier system of justice. The largest banks need to be broken up, the only realistic way to truly end both too big to fail and too big to jail. But since our government has demonstrated a reluctance to do so, perhaps the next time a megabank presents HSBC's argument that it should not be criminally charged because it would destabilize the financial system, instead of capitulating to this threat, DOJ should require at a bare minimum that in return for allowing the bank to survive, it must break itself up, ensuring that it could never hold the justice system hostage again. Otherwise, we can look forward to many more press conferences that are long on drama but short on impact.

Neil Barofsky was the Special United States Treasury Department Inspector General to oversee the Troubled Assets Relief Program from 2009 until his resignation in February 2011. He is currently a senior fellow at the NYU School of Law and is the author of Bailout (Free Press, 2012).

December 13, 2012For the first time, the Federal Reserve has explicitly linked interest rates to unemployment.

Rates will remain near zero "at least as long" as unemployment remains above 6.5 percent and if inflation is projected to be no more than 2.5 percent, said the Federal Open Market Committee in a statement Wednesday.

Put to one side the question now obsessing stock and bond traders - whether the new standard means higher interest rates will kick in sooner than the middle of 2015, which had been the Fed's previous position.

By linking interest rates directly to the rate of unemployment, Bernanke is explicitly acknowledging that the Federal Reserve Board has two mandates - not just price but also employment. "The conditions now prevailing in the job market represent an enormous waste of human and economic potential," said Fed Chairman Ben S. Bernanke.

These are refreshing words at a time when Congress and the White House seem more concerned about reducing the federal budget deficit than generating more jobs.

But the sad fact is near-zero interest rates won't do much for jobs because banks aren't allowing many people to take advantage of them. If you've tried lately to refinance your home or get a home equity loan you know what I mean.

Banks don't need to lend to homeowners. They can get a higher return on the almost-free money they borrow from the Fed by betting on derivatives in the vast casino called the global capital market.

Besides, they've still got a lot of junk mortgage loans on their books and don't want to risk adding more.

Low interest rates also lower the cost of capital, which in theory should encourage companies to borrow for expansion and more hiring. But companies won't expand or hire until they have more customers. And they won't have more customers as long as most people don't have additional money to spend.

And here we come to the crux of the problem. Consumers don't have additional money. The median wage keeps dropping, adjusted for inflation. Most of the new jobs in the economy pay less than the jobs they replaced.

Corporate profits are taking a higher share of the total economy than they have since World War II, but wages are taking the smallest share since then (see graph).

Self-Love Stifles Our Being and Becoming"The logic of worldly success rests on a fallacy: the strange error that our perfection depends on the thoughts and opinions and applause of other men...

The selfishness of an age that has devoted itself to the mere cult of pleasure has tainted the whole human race with an error that makes all our acts more or less lies against God...

The devil is no fool. He can get people feeling about heaven the way they ought to feel about hell. He can make them fear the means of grace the way they do not fear sin.

And he does so, not by light but by obscurity, not by realities but by shadows; not by clarity and substance, but by dreams and the creatures of psychosis. And men are so poor in intellect that a few cold chills down their spine will be enough to keep them from ever finding out the truth about anything...

Only the man who has had to face despair is really convinced that he needs mercy. Those who do not want mercy never seek it. It is better to find God on the threshold of despair than to risk our lives in a complacency that has never felt the need of forgiveness.

A life that is without problems may literally be more hopeless than one that always verges on despair...

Indeed, the truth that many people never understand, until it is too late, is that the more you try to avoid suffering, the more you suffer, because smaller and more insignificant things begin to torture you, in proportion to your fear of being hurt.

The one who does most to avoid suffering is, in the end, the one who suffers the most: and his suffering comes to him from things so little and so trivial that one can say that it is no longer objective at all. It is his own existence, his own being, that is at once the subject and the source of his pain, and his very existence and consciousness is his greatest torture...

Despair is the absolute extreme of self-love. It is reached when a person deliberately turns his back on all help from anyone else in order to taste the rotten luxury of knowing himself to be lost...

It is therefore of supreme importance that we consent to live not for ourselves but for others. When we so this we will be able first of all to face and accept our own limitations.

As long as we secretly adore ourselves, our own deficiencies will remain to torture us with an apparent defilement. But if we live for others, we will gradually discover that no expects us to be "as gods". We will see that we are human, like everyone else, that we all have weaknesses and deficiencies, and that these limitations of ours play a most important part in all our lives.

It is because of them that we need others and others need us. We are not all weak in the same spots, and so we supplement and complete one another, each one making up in himself for the lack in another...

To say that I am made in the image of God is to say that Love is the reason for my existence, for God is love. Love is my true identity. Selflessness is my true self. Love is my true character. Love is my name."

Thomas Merton

But it is our benchmark, our touchstone. It is how we are able to determine if what we say or do or hold dear is founded in goodness and life, or in a destructive snare, a willfulness, the cult of the self, and death.

For love takes us out of ourselves and completes us. And the opposite of love is not hatred, but the selfishness of self-love, and the dark angel's first sin, pride.

"I think that the depth of Satan's pride is difficult for humans to understand, and therefore it is easy to fall into this error and partake of it, thinking, all the while, that we are instead doing something great and beautiful."Posted by Jesse at 11:18 AMFyodor Dostoyevsky

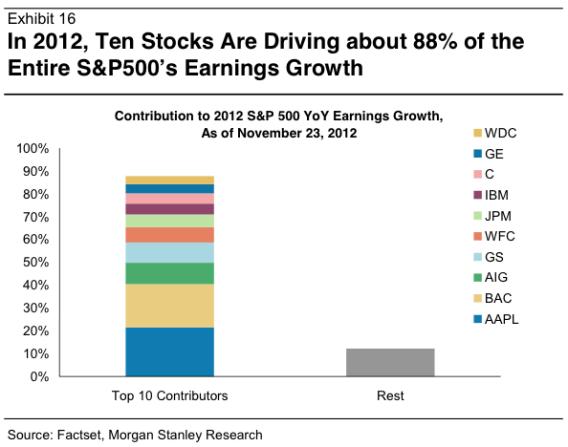

01 December 2012 Look at the concentration of financially related stocks in that top ten. That speaks volumes about the nature of this Fed generated 'recovery.'

h/t The Big Picture

Posted by Jesse at 5:38 PM

As Ochberg implies, psychopaths don't have ethical considerations, and narcissists and asocial personalities don't care.In layman's terms I think most of these fellows have a great hole in their being. They know that something is not right with them, but their egos will not allow them to acknowledge it.

Those who gravitate toward the corporate power structures can be quite successful in some organizations. But despite outward success they are always restless, unfulfilled, and tend to project their dissatisfaction outward and ascribe it to others. If they succeed it is all them, but if they fail, someone else is at fault.

They are incapable of trust, because everything they do is a facade, a lie. Therefore they rarely have a real relationship with their families, and at best view them as a desirable addition to their collection. They have utter contempt for other people, although they will use flattery and other means to create a dependency while they are using them. And after that is done, they will be discarded without another thought.

They are like sharks, endlessly seeking to fill their terrible emptiness with possessions, be they things or other people. They are literally insatiable in their needs, and highly focused in their pursuit of them.

They are very clever in finding the weaknesses in people and organizations, and will exploit them ruthlessly. Ethics and conscience provide no brake or boundaries on their willingness to say and do anything that is required to achieve their ends. If you attempt to thwart, be prepared for something a little different, and completely off the hook in response.

It is really something to see them at work. The destruction they can wreak, sometimes with remarkably superficial charm and high verbal acuity, is hard to describe until you see it in action.

They are always a challenge to the HR and compliance departments, and frequently end up badly, one way or the other. It becomes a personal challenge to see how far one can go without being stopped, far beyond any personal needs or requirements. Flouting the rules becomes a game in itself.

Posted by Jesse at 10:05 PM

"When I despair, I remember that all through history the ways of truth and love have always won.There have been tyrants, and murderers, and for a time they can seem invincible, but in the end they always fall.

Think of it--always."

Mohandas K. Gandhi

"For we wrestle not against flesh and blood, but against principalities and powers, against the rulers of the darkness of this world, against spiritual wickedness in high places."Ephesians 6:12

"Good men and bad men alike are capable of weakness. The difference is simply that a bad man will be proud all his life of one good deed - while an honest man is hardly aware of his good acts, but remembers a single sin for years on end...Human groupings have one main purpose: to assert everyone's right to be different, to be special, to think, feel and live in his or her own way. People join together in order to win or defend this right.

But this is where a terrible, fateful error is born: the belief that these groupings in the name of a race, a God, a party or a State are the very purpose of life and not simply a means to an end.

No! The only true and lasting meaning of the struggle for life lies in the individual, in his modest peculiarities and in his right to these peculiarities...

I have seen that it is not man who is impotent in the struggle against evil, but the power of evil that is impotent in the struggle against man.

The powerlessness of kindness, of senseless kindness, is the secret of its immortality. It can never by conquered. The more stupid, the more senseless, the more helpless it may seem, the vaster it is.

Evil is impotent before it. The prophets, religious teachers, reformers, social and political leaders are impotent before it.

This dumb, blind love is man's meaning. Human history is not the battle of good struggling to overcome evil. It is a battle fought by a great evil, struggling to crush a small kernel of human kindness.

But if what is human in human beings has not been destroyed even now, then evil will never conquer."

Vasily Grossman, Life and Fate

Society

Groupthink : Two Party System as Polyarchy : Corruption of Regulators : Bureaucracies : Understanding Micromanagers and Control Freaks : Toxic Managers : Harvard Mafia : Diplomatic Communication : Surviving a Bad Performance Review : Insufficient Retirement Funds as Immanent Problem of Neoliberal Regime : PseudoScience : Who Rules America : Neoliberalism : The Iron Law of Oligarchy : Libertarian Philosophy

Quotes

War and Peace : Skeptical Finance : John Kenneth Galbraith :Talleyrand : Oscar Wilde : Otto Von Bismarck : Keynes : George Carlin : Skeptics : Propaganda : SE quotes : Language Design and Programming Quotes : Random IT-related quotes : Somerset Maugham : Marcus Aurelius : Kurt Vonnegut : Eric Hoffer : Winston Churchill : Napoleon Bonaparte : Ambrose Bierce : Bernard Shaw : Mark Twain Quotes

Bulletin:

Vol 25, No.12 (December, 2013) Rational Fools vs. Efficient Crooks The efficient markets hypothesis : Political Skeptic Bulletin, 2013 : Unemployment Bulletin, 2010 : Vol 23, No.10 (October, 2011) An observation about corporate security departments : Slightly Skeptical Euromaydan Chronicles, June 2014 : Greenspan legacy bulletin, 2008 : Vol 25, No.10 (October, 2013) Cryptolocker Trojan (Win32/Crilock.A) : Vol 25, No.08 (August, 2013) Cloud providers as intelligence collection hubs : Financial Humor Bulletin, 2010 : Inequality Bulletin, 2009 : Financial Humor Bulletin, 2008 : Copyleft Problems Bulletin, 2004 : Financial Humor Bulletin, 2011 : Energy Bulletin, 2010 : Malware Protection Bulletin, 2010 : Vol 26, No.1 (January, 2013) Object-Oriented Cult : Political Skeptic Bulletin, 2011 : Vol 23, No.11 (November, 2011) Softpanorama classification of sysadmin horror stories : Vol 25, No.05 (May, 2013) Corporate bullshit as a communication method : Vol 25, No.06 (June, 2013) A Note on the Relationship of Brooks Law and Conway Law

History:

Fifty glorious years (1950-2000): the triumph of the US computer engineering : Donald Knuth : TAoCP and its Influence of Computer Science : Richard Stallman : Linus Torvalds : Larry Wall : John K. Ousterhout : CTSS : Multix OS Unix History : Unix shell history : VI editor : History of pipes concept : Solaris : MS DOS : Programming Languages History : PL/1 : Simula 67 : C : History of GCC development : Scripting Languages : Perl history : OS History : Mail : DNS : SSH : CPU Instruction Sets : SPARC systems 1987-2006 : Norton Commander : Norton Utilities : Norton Ghost : Frontpage history : Malware Defense History : GNU Screen : OSS early history

Classic books:

The Peter Principle : Parkinson Law : 1984 : The Mythical Man-Month : How to Solve It by George Polya : The Art of Computer Programming : The Elements of Programming Style : The Unix Hater’s Handbook : The Jargon file : The True Believer : Programming Pearls : The Good Soldier Svejk : The Power Elite

Most popular humor pages:

Manifest of the Softpanorama IT Slacker Society : Ten Commandments of the IT Slackers Society : Computer Humor Collection : BSD Logo Story : The Cuckoo's Egg : IT Slang : C++ Humor : ARE YOU A BBS ADDICT? : The Perl Purity Test : Object oriented programmers of all nations : Financial Humor : Financial Humor Bulletin, 2008 : Financial Humor Bulletin, 2010 : The Most Comprehensive Collection of Editor-related Humor : Programming Language Humor : Goldman Sachs related humor : Greenspan humor : C Humor : Scripting Humor : Real Programmers Humor : Web Humor : GPL-related Humor : OFM Humor : Politically Incorrect Humor : IDS Humor : "Linux Sucks" Humor : Russian Musical Humor : Best Russian Programmer Humor : Microsoft plans to buy Catholic Church : Richard Stallman Related Humor : Admin Humor : Perl-related Humor : Linus Torvalds Related humor : PseudoScience Related Humor : Networking Humor : Shell Humor : Financial Humor Bulletin, 2011 : Financial Humor Bulletin, 2012 : Financial Humor Bulletin, 2013 : Java Humor : Software Engineering Humor : Sun Solaris Related Humor : Education Humor : IBM Humor : Assembler-related Humor : VIM Humor : Computer Viruses Humor : Bright tomorrow is rescheduled to a day after tomorrow : Classic Computer Humor

The Last but not Least Technology is dominated by two types of people: those who understand what they do not manage and those who manage what they do not understand ~Archibald Putt. Ph.D

Copyright © 1996-2021 by Softpanorama Society. www.softpanorama.org was initially created as a service to the (now defunct) UN Sustainable Development Networking Programme (SDNP) without any remuneration. This document is an industrial compilation designed and created exclusively for educational use and is distributed under the Softpanorama Content License. Original materials copyright belong to respective owners. Quotes are made for educational purposes only in compliance with the fair use doctrine.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to advance understanding of computer science, IT technology, economic, scientific, and social issues. We believe this constitutes a 'fair use' of any such copyrighted material as provided by section 107 of the US Copyright Law according to which such material can be distributed without profit exclusively for research and educational purposes.