|

|

Home | Switchboard | Unix Administration | Red Hat | TCP/IP Networks | Neoliberalism | Toxic Managers |

| (slightly skeptical) Educational society promoting "Back to basics" movement against IT overcomplexity and bastardization of classic Unix | |||||||

| Jan | Feb | Mar | Apr | May | June | July | Aug | Sep | Oct | Nov | Dec |

|

|

|

|

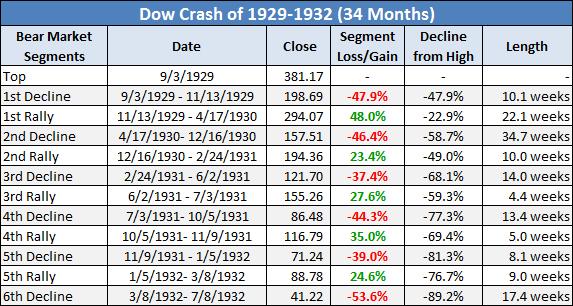

Paper Economy

The following charts provide a simple comparison between the big stock bounce that occurred in the wake of the DOW crash of 1929 and the bounce we are seeing today in the S&P 500 index.

The method of alignment was simple… take the first definitive up trading day off the bottom of the preceding bear market low and set that as the start of the series… then simply re-base both series to a value of 100 so that they can be compared side-by-side.

The lower bar chart plots the cumulative percentage change since the start of each bounce.

The S&P 500 is up over 42% in just about 120 trading days… a very aggressive run with an obvious note of mania to it… and wholly comparable to yet even notably stronger than the price movement seen in the 1930s-era DOW rally.

At this point for the 30s-era DOW, the bull-run was over as the bear trend resumed in earnest… today though the Bull is on the move… how long will this boom last?

Only time will tell… But for now, let’s continue to keep a watchful eye…

One of the most remarkable aspects of the success of Wall Street in subordinating the real economy to its wishes and needs is the con job implicit in the application of the word "innovation" to what might more accurately be described as tax evasion, regulatory arbitrage, and chicanery. Martin Mayer once described innovation as "using new technology to do that which was forbidden under the old technology."Rob Johnson, former economist to the Senate Banking Committee, has a new article that parses how the financial services industry has managed to wrap itself in the mantle of progress, when if anything its new products have been a force for destruction rather than creation. We had a wave of new OTC derivative products sold, starting in the early 1990s, whose high profits for the most part depended on the fact that they allowed investors to game ratings or mask the economic substance of transactions or fob risk off on to people who really did not understand it. The industry managed to co-opt SEC chairman Arthur Levitt and fight a delaying action until the media got bored and went on to other matters, A collateralized debt obligation market blew up in the late 1990s only to be reborn in the new millennium in only slightly modified form to wreak havoc on a much greater scale. Abuses of off-balance-sheet vehicles by Enron did not lead to reforms that affected the financial services industry much, since huge carve outs were made so as to keep mortgage securitization alive. And I will admit to having been unable to keep up on the news as fully as I once did, but I don't recall any of the proposed fixes for the securitization market calling for changes in deal structures and servicer contracts so as to make mortgage mods easier and more attractive.

From Johnson:

Innovation. It is a lovely word that teases the mind with the notion of expansive possibilities... A win-win game. Just as Americans once expanded westward to relieve social tensions, we are now exhorted to have a rather imprecise faith in the notion of technological change to deliver us from our current troubles. Embracing that starship to unlimited possibility and deliverance requires a faith that cannot be easily refuted: Who, after all, is against progress?David Noble, who has written so powerfully about this in his series of books including America by Design, Religion of Technology and Beyond the Promised Land, has explored this mythology of redemption and salvation through changes in technique and deference to undefined dreams of “possibility.” It is time to apply his perspective to the religion of financial innovation.

We have seen the financial sector, with its massive resources and access to the best minds of public relations, work to create what Stuart Ewen calls “spin.” ....we have been ever-so-persistently encouraged to draw the comparison between developments in financial products and the great leap forward in social uses of computers and the Internet, or advances in biomedical research. Former mathematicians, physicists, and computer scientists redirected their energies and Ph.D. tenacity to the domain of finance. Financial innovation was presented to us in a way that suggested that great things were happening for mankind. The presentations were usually vague. To understand them, we had only the power of our own imaginations, or perhaps, failing that, our awe in the face of this powerful expertise, confidently propelling us to a greater future.

Skeptical questioning–”Where are the benefits to be found?”–was frowned upon or ignored. ”Just doesn’t get it,” the whisperers would say. The skeptic was discredited with the insinuation that he or she was either 1) jealous of those who were making money and progress at the same time, or 2) had fallen down like a tired horse and just could not keep up with the new breed of thoroughbreds on Wall Street. After all, what kind of human spirit would get in the way of progress?

The reason I bring forward the notion of “spin” is that I sense that the great benefits of financial innovation were not self-evident, and that some form of intimidation or coercion was needed to keep the genie of doubt in its bottle. If a great Wall Street luminary were actually forcefully questioned, could he really convince grandma and you and me that he was making the world a better place? The point of the exercise, the spin, was to create deference to this process, to deter questioning and create social license, to make what those rocket scientists were doing appear as though their work was not merely profitable but something that would benefit us all. It was presented like a free option to the public: Wall Street pays these guys and “shazam!” They do things that make us all better off. No reason to get in the way of that, or even suggest that your Congressman or friendly bank regulator keep an eye on the proceedings. The subtle message was, “Get out of the way.” Such was the Kool-Aid poured into our glass by the financial press and pundits. That capital avoidance and tax avoidance and regulatory evasion were involved in offshore and off- balance-sheet methods was rarely emphasized, as the notion of innovation was paraded like a badge of valor.

Then we had the crisis. The side effects and spillovers and bailouts reminded us that what we had allowed to unfold was not a free option on progress but something that had a downside, too. It’s funny how a crisis changes your perceptions....

Despite these recent protestations, I am witnessing the lingering hangover of deference to so-called “innovation.” It permeates the debate on regulation. We hear that getting in the way of new technique may cause more problems than it solves. Or that the innovators can always outrun the regulators. Or, and this is my favorite, that nothing you do to stifle these new derivative products like credit default swaps will (ominous music in the background) lead to “systemic risk.” Systemic risk is the new stun-gun phrase to impart dread to those who would tamper with this delicate machine.

Malarky. This is all code for defer to the wishes of those who make money from these techniques.

Financial engineers on Wall Street are employed to make money for Wall Street firms and themselves. There is no hidden code that says they will design their products to align private and social benefits and costs. That is precisely where a healthy role for regulation and laws and enforcement can be envisioned. At the same time, it is important not to be romantic about that vision, though. Regulatory policy often does not live up to the romantic appeal, as theories of collective action and regulatory capture have illuminated.

My takeaway is distinctly unromantic. It is that, devoid of these religious-like connotations, innovation simply implies the use of a new method or technique. It can be harmful or it can be helpful. Let’s keep score. It can benefit us both, or it can harm us both, or it can make you better off and me worse off, or vice versa. That sober reality, and the notion that we are a society, sets the stage for critical thinking about these methods. If credit default swaps serve a purpose and are economically viable when proper capital and margin requirements are in place, then let the proponents bear the burden of proof in convincing us of the benefits to society according to some real social goals, rather than the vague myth of intangible progress. Protecting the profit margins of large investment firms is not a social goal.

We have a serious and real problem right now as a society that employs complex technique. Experts in the financial, nutrition, energy, and health realms have been found wanting when the curtain is pulled back and their behavior examined. Trust, particularly in financial expertise, has been shattered. Early in the 20th century, the so-called Progressive Era was an attempt to bridge the gap between the oligarchs of industry and the populists. Deference to expertise was said to be in the interest of all. Delay gratification and let the experts allocate capital so that in the future we would all be better off was the mantra. It had a religious-like psychic resonance. Experts on economics and social planning were custodians of our future, not unlike the role that priests played in earlier times. Restrain yourself now to achieve the promise of the afterlife. The linchpin was the experts vision and integrity. They were trusted to make sure we all got to economic heaven together.

We just got handed a big bill and the perpetrators that led to the bailouts are back getting large bonuses. If experts cannot be trusted and governments are unwilling to change the rules, then we will once again be heading toward popular reaction. The cooperative game is breaking down. The population showed us a hint of that over the AIG bonuses. A volcano that is still today may yet explode tomorrow.

As I watch the stories of this newest revelation on the wonders of financial innovation, so-called high frequency trading (HFT), I scratch my head and wonder how we got to this place: That most profound mystical deity which we are asked to worship, “the market,” can now be rigged so that a few get to see orders beforehand. As Charles Duhigg wrote last week in the New York Times, “While markets are supposed to ensure transparency by showing orders to everyone simultaneously, a loophole in regulations allows marketplaces like Nasdaq to show traders some orders ahead of everyone else in exchange for a fee.”

This “innovation”–employing monster computing power and the apparent ability to buy your way to the front of the line–looks like old fashioned front-running to me. How can that contribute to the integrity of our marketplace? Bob Kuttner has written an illuminating piece on this subject. For my part, I just hope that our society can demystify (unspin?) this process. It is time to build a financial system that serves the real economy for the next generation. To do so, we may need to sweep aside some of the so-called innovations in financial practice that were born of this foolish era of market fundamentalism and its supervisory and enforcement laxity.

Surely there are techniques that we should adopt. Yet in the aftermath of the crisis the burden of proof is on those who advocate them. Where are the benefits to society? What are the costs? To answer those questions, we must come out from the well spun power cloud of Wall Street and ask real questions. Regarding financial innovation, I am fond of the lyrics of Michael Stipe. It is time we start losing our religion.

- attempter said...

- The facts here are very simple.

There is only one measure of the health of an economy: how many fulfilling, living-wage jobs are created or destroyed. (All other factors can be distilled to this.)

We're now approaching 40 years of financialization and globalization. That's far more than enough time to render judgement.

What has happened to real wages? They've steadily declined since 1973.

What has happened to real jobs? They've been destroyed by outsourcing, offshoring, and technologizing/deskilling.

The financial sector presided over this massacre.

(That's dispositive right there. But we can also add the extreme burgeoning of wealth unequality. And we can add the sickening volatility and moral degradation of a boom-bust binge-purge exponential debt crisis socioeconomy, which is the only kind of socioeconomy globalization can generate. The "Great Moderation" is for the hall of fame of Orwellian totalitarian terminology. The banks facilitated all of this.)

So the verdict is in. The financial sector adds no socioeconomic value, only destroys it.

It should be completely dismantled.

Siggy said...

- Wall Street is a place were 'everything old is (perenially) new again'. Since the time when bankers were relieved of personal liability, there has been no incentive to be legal, moral and ethical. For those who would want to bring morality and ethical conduct to the market, they should first look at who benefits from such dodges as term-auction securities, the grandest fee scam I have noted in 50 years. Similarly, few, if any, sellers of CDS have the balance sheet to support the volume of contracts they have written. What should have occurred is that we should have had the catastrophe. Perhaps then, all that theater in the congressional hearings would reduce to something meaningful.

Today we see a stock market intent on advancing in the face of incredibly poor economic reports which while better than earlier data nonetheless stink. Employment is still shrinking and until we see real job growth and some statistical artifice our economy will not be very comforting.

Bill Dudley says that the ability of the Fed to pay interest on excess reserves will thwart the onset of inflation. We will get to see if that is a lovely set of emperors new clothes in the coming months. Look for interest rates to creep up as well as the costs of staples at the supermarket where the 'real' economy shops. What we are ling thru is the grandest economic experiment ever conducted. For now I do not believe that it has a good outcome.

Selected comments

JD:

well said, kudos to Johnson;

As an economist I give a break to those, especially Greenspan and Summers, who in the 1990s spread the word of the benefits in efficient capital allocation enabled by these new instruments. Without digging into and understanding the details we could glimpse the potential, and after all, the Wall Street geniuses surely new how to hedge and diversify. Not!

But now that they have blown up on all of us, its high time to put the burden of proof on those who resist regulation.

craazyman:

Making "money" through leverage.

If GNP = money supply X money velocity, and counterfeting money supply is a criminal offense (Isaac Newton took glee in hanging counterfeiters when he ran the British Mint), then the counterfeiting of good credit that boosts money velocity is algebraically equivalent to counterfeiting currency.

And the call it "innovation". Ha ha ha ahhahah hahah hgahah ROTFLMAO

And yet the counterfeiters get our tax dollars for their bonuses, even AFTER the counterfeit credit implodes like wooden nickels.

Admittedly, that is pretty innovative.

Hugh

Rob Johnson is basically describing the elements of a con. Play upon the ego, greed, and fears of the mark.

You're a smart guy. You can understand how modern day gimfazzlery works. The returns are amazing but I got to have an answer now because I have 5 other guys wanting in on the deal.

Silas Barta

The simplest test of whether financial innovation has benefited society is this:

Can you name a project that was able to be funded because of Wall Street innovation, that would not otherwise have been funded, and thereby produced something profoundly beneficial?

I can't see a case where that's happened. So, it's most likely been all a crock.

Sukh Hayre

ilas,

"Can you name a project that was able to be funded because of Wall Street innovation, that would not otherwise have been funded"

Therein lies the rub.

You see, it is not America that has been conned by Wall Street. It is the rest of the world (to America's benefit).

America now has a huge supply of housing for all of its citizens, that had it not been for this "innovation", would not have existed. Not to mention all the commercial buildings and the road infrastructure put in place to commute to these new developments.

All the paper wealth that has been created over the last 30 years was just one large Ponzi scheme. The paper wealth will be destroyed, but the real assets constructed will remain.

Had it not been for this innovation, people would still be broke today, but we would not have the housing.

This to me seems like the best wealth redistribution plan that could possibly have been implemented in a capitalistic, dog-eat-dog society that America has become. When the poor pick up debts they can never realistically hope to pay, they will eventually default, and therefore will be no worse off. But a house will have been built that they will eventually be able to reside in, at a rent they can afford to pay, based on their minimal income. This will bring down the value of the home, which will now become an investment property. But the loser in all this is the person who had the savings in the first place to lend the money to have this home built.

Therefore, by greed, wealth is eventually redistributed. When the poor can borrow no more, the economy collapses and debt destruction through bankruptcy takes hold. But one man's debt is another man's wealth, so this is destruction of debt is also a destruction of wealth. This is capitalism's reset button.

Sukh Hayre

In regards to how the US benefited on the backs of other nations:

I forgot to mention all the oil and manufactured goods that have been sent our way in exchange for worthless IOU's.

How's this for innovation:

Import manufactured goods and oil in exchange for US dollars. Then, borrow those dollars back to build houses you cannot afford. Then, default on your housing debts.

In the end, you have consumed oil and manufactured goods provided by others, and have built homes for your citizens that they could not afford.

In the end, Americans get oil, manufactured goods, and homes, and those that sent you the oil and the manufactured goods get stiffed.

Also getting stiffed in this process will be anyone who thought they accumulated wealth by being a middle man in the process, as they will see their wealth destroyed as their investments drop in value (as companies will eventually go broke and shareholders will be wiped out - once a large enough company in any industry (ie GM) reorganizes itself by going through the bankruptcy process, do all its competitors not have to evenually follow suit, as the company has a competitive advantage once it comes out of bankruptcy?. This also means that the life savings and pensions of the middle-class are also going to be wiped out.

Only those with so much wealth that they can afford to not chase returns by buying equities (are content with the meager return they get on US Treasuries) will be able to save any semblance (sp??) of their wealth.

You cannot create inflation when debt is being destroyed. Unless you are willing to go Zimbabwe's route and just print money and hand it out. This can only happen if the government decides to do away with double-sided accounting and decides that Plan B is to just actually print US dollars and give its citizens enough of them to wipe out their debts.

Anonymous

One more loophole masquerading as Fin innovation in the news lately is flash trading.

David Shillman, an associate director at the Commission's Division of Trading and Markets, said at the SIFMA conference that flash orders lasting less than 500 milliseconds fall within an exception to the Quote Rule, or Rule 602, in Regulation NMS. The Quote Rule requires all market centers to publicly disseminate their best bids and offers through the securities information processors. The exception is for orders that are immediately executed or canceled.

All the exchanges (even those that protest flash trading) are ready to jump in if the loophole stays. If it's banned the playing field would be leveled for all players, if its not closed the playing field will be leveled when the remaining holdouts jump in.

DRX, to answer your question see Nina Mehta at Trader magazine here

http://www.tradersmagazine.com/news/pipeline-blocks-high-frequency-trading-al-berkeley-104059-1.html?pg=5.Actually, all her stuff is terrific.

The Big Picture

Above I took C, FNM, and FRE and expressed their *composite* volumes (e.g., the volumes transacted across all exchanges) as a fraction of NYSE volume. What we see is that, early in 2007, those three stocks accounted for only 1-3% of NYSE volume. During the financial crisis of late 2008 and again as the market was bottoming in early 2009, that ratio skyrocked to well over 50%.

Recently, however, the volume in these three stocks has hit astronomical levels relative to total NYSE trading, as all three have made phenomenal percentage gains during August. Indeed, the composite volume of these three stocks alone has recently doubled total NYSE volume. If we look at just the NYSE trading of these firms, they are accounting for about 40% of NYSE volume. It is not surprising that Brian would notice TRIN flipping up and down as these stocks change direction.

Again, the question is what all this means. There is no way that mom and pop trader and investor are involved in any meaningful way in generating these kind of daily trading volumes. Nor are proprietary trading shops capable of generating volumes that exceed those of the entire New York Stock Exchange. While I have no doubt that the algorithmic trade close to the market is participating in this movement, the directionality of the involvement suggests that large financial institutions are systematically buying the beaten-up shares of the poster children for TARP: C, FNM, FRE, AIG, and the like.

It is worth noting in this regard that other major (healthy) financial firms, such as GS and JPM, have seen no such surge in their volume or their trading prices.

My best guess? We’re seeing a massive infusion of capital into very troubled financial institutions, no doubt aided by short covering and the participation of program traders and proprietary daytrading firms. Where is the capital coming from? Why has it poured in so suddenly (the really large infusions began in early August)? Why is it coming in at such a pace that it is dominating NYSE volume?

Zero Hedge rightly wonders why this hasn’t triggered alarms at the exchange. And why is it happening with only the weakest financial institutions?

- skysurfer Says:

August 31st, 2009 at 3:06 pmIt may also be interesting to note that C has the largest exposure to off balance sheet entities that may need to come back on the balance sheet due to FAS 140. I am not sure about FRE and FNM, but I believe that C has almost $1,000 billion. Somebody correct me if I am wrong on this as it has been a couple of months since I looked into it. I thought it would matter about 30% ago on the S&P. Silly me.

As for helping the companies, it helps their capital structure look better, especially if all of these entities go back to the balance sheet.

- constantnormal Says:

August 31st, 2009 at 3:06 pm@JohnnyVee 2:53 pm

It works like this: corporations use shelf-registered stock sales to the Fed/Treasury/designated agent of the Fedreasury to bring money in-house. The use of shelf-registered stock sales means it can occur somewhat quietly. Also, they can sell shares held by the companies involved. Either way, it amounts to shares of worthless stock being exchanged for cash.

Another way is for the Fedreasury to buy shares on the open market, pumping up the prices of the shares and boosting the balance sheet valuations of any shares held by the companies in question. But that way is a bit indirect and not nearly as efficient as buying the shares directly from the companies.

- constantnormal Says:

August 31st, 2009 at 3:12 pmHot Dog! It’s the Conspiracy Theory World Series! And I’m at bat …

Ok, let’s try this one … the Fed is printing money and buying shares in the Fantastic Four (nod to Marvel Entertainment, Disney’s newest crown jewel). But but but … you say, why is the government (and regardless of any theoretical nonsense, the Fed IS a part of the government) buying shares in AIG, FRE, FNM, they are already in “government conservatorship”? My answer to that involves how much of their stock and bonds (especially bonds) are held by large parties (China?) that do NOT want to see the companies blown out like candles in a hurricane if the truth about their financial state should become known.

- Steenbarger Says:

August 31st, 2009 at 3:41 pm@JohnnyVee 2:53 PM

Legit question; thanks. As I tried to clarify in my follow up to this piece, lifting the shares of these companies would provide capital infusion to the extent that the rally (and story regarding the companies’ viability) enabled the firms to raise additional capital. It’s tough to raise capital as a zombie languishing at two bucks a share, and the political will for additional bailout is nil.

Brett

nakedcapitalism.com

Economists Thomas Piketty and Emmanuel Saez have made careers of studying US income inequality using IRS data, which goes back to 1913. The most recent data available (for 2007) showed that the top 14,988 households (0.01% of the population) received 6.04% of income, the highest figure for any year since the data became available. The top 1% of households received 23.5% of income (the second highest on record, after 1928), while the top 10% received 49.7% of income (the highest on record).

The fortunate 14,988 had an average income in 2007 of $35,042,705. They had an average federal tax burden, according to Piketty and Saez, of 34.7%, leaving them after tax income of $22.9 million. If you assume a 50% savings rate among this group, you get total savings of $171.5 billion. This is nearly ONE HALF of the total savings for the entire country implied by a savings rate of 4.2% ($365 bn) reported in this month’s Bureau of Economic Analysis data.

I’ve never actually had an after tax income of $22.9 million, so I couldn’t say for sure whether a 50% savings rate is a reasonable assumption, but I’m going to go out on a limb and say that it is, just based on the pure physics of spending money. Buying cars, clothes, and fancy dinners, even at Masa, won’t get you there…the math doesn’t work. Buying a private jet could get you there, but most people, even rich people, don’t buy one of those every year. The only EASY way to spend more than 50% of $22.9 million on an annual basis is to buy lots of houses…but the definition of “personal consumption expenditure” used by the BEA specifically excludes purchases of real estate. They use an imputed rent calculation instead. So I’m going to stick with my 50% number.

If we expand our survey to the top 1% of all households, we find an average income of $1.36 million for 2007. These folks had an average federal tax burden of just under 33%, so their after tax income averaged $916 thousand. If you assume this group had a savings rate of 33%, you get total savings of $452 billion (remember, $171.5 bn of this comes from the top 0.01%, we’re assuming a savings rate of around 25% of after tax income for the “poorer” 99% of the top 1%) This is more than 100% of the personal savings of the entire population, according to the BEA data. It implies that 99% of the US population still has, on average, a negative savings rate of around 1.3%. If you subtract the next nine percent, which likely still has a positive savings rate, the data for the bottom 90% becomes even more depressing, implying a negative savings rate of close to 5%.

08/15/2009 | http://www.zerohedge.com/

The stratified US consumer

One reason why delevering trends in the US consumer base are not equal, and have to be analyzed separately, is due to the dramatic schism within the consumer population, specifically the purchasing capacities, limitations and motivations of various income classes in US society. This is an approach that is all too often missing from traditional analyses of the US consumer. In order to properly analyze some of the major undercurrents within the consumer population, Zero Hedge relied on the most recent Survey of Consumer Finances, as well as an August 6 report by Bank Of America, "The Myth Of The Overlevered Consumer."

Three primary drivers determine one's willingness to spend - credit quality, disposable income, and wealth. Yet as the table below demonstrates, there is a substantial disparity in how these three factors impact the two critical classes of US society - the Middle and the Upper class.

What is immediately obvious is that based on estimates by Bank of America, the 50% of US population which makes up the middle class, is responsible for the same amount of total consumption as the 10% of the upper class. Another observation is that the balance, 40% of population considered Low-Income consumers, is responsible only for 12% of total consumption.

Mr Blanchard said an IMF study of post-War banking crises led to an unpleasant finding. "Output does not go back to its old trend path, but remains permanently below it."

Then the sting: we are exhausting the limits of fiscal stimulus. "The average ratio of debt to GDP in the G-20 economies was high before the crisis, and is forecast to exceed 100pc in the next few years".

We cannot add debt, so the IMF says we must draw down our future pensions and future health spending to keep today's economy afloat. "A modest cut in the growth rates of entitlements can buy substantial fiscal space for continuing stimulus."

Bill

There will be no sustained recovery, since modern economies are based entirely upon an ever-growing, cheap supply of oil and, according to the folks who track oil production, including 50% of top oil executives, who have decent access to research within their field, the world is pumping the maximum that ever will be pumped right now. Post-peak, actual availability of oil will decline at 3% to 10% a year, for up to a 50% decline in annual supply in 7 years.graeme daveyThis will not support a recovery to pre-peak euphoria, no matter who prints or spends money.

Quantative easing is unfortunately giving the hedge funds more money to burn and creating a commodity price bubble that the the consumer will have to pay for twice.ObamanomicsOnce up front to buy their fuel/food and secondly in increased tax to pay for the obscene level of debt. After all the oil price is set in London not Saudi.......

Meanwhile the parasites continue their feast. The only answer is a levy on hedge fund profit I'm afraid -- and exchange controls to stop the fleeing abroad of that profit. When is our money going to stop being poured naively into the mouths of those who don't need it?

"I think this time Europe will have the soup kitchens and America will have the fascism."Psst: America is a fascist empire which is collapsing under a mountain of debt, much like Rome, The bought and paid for political whores may be able to kick the can down the road a few more years but the will not be able to stop the collapse of the unsustainable.

mark weekes

Another superb article Ambrose!

We already have soup kitchens in the shape of mass welfare which wasnt there in the thirties. couple that with all the loans quangoes and grants and charities and its much worse than the thirties.

Stevie b.

But Ambrose - isn't it all just too late? Isn't postponing the day of reckoning and hoping for something to turn up, isn't that better than anything else because it's just too late to do anything else?

Next week we move into September, the riskiest month of the year for financial markets, with the federals escalating preparations for a flu pandemic, while Congress considers legislation providing a 'kill switch' on the Internet for President Obama to use in the event of 'an emergency.' There are widespread rumours of a bank holiday lasting one week after a market meltdown begins in the US, during which the banks would be restructured.

Risky times indeed, and those in the best position to know what is happening behind the scenes are hitting the exits in record numbers right now, running to cash, and hard assets and currencies.

... The Obama Economics and Regulatory Team, in conjunction with the Federal Reserve, have accomplished no serious reform of the financial system. They have enabled the type of market inefficiency, soft fraud and price manipulation that is undermining global confidence in the integrity of US markets and financial products. And they have advanced a proposal to consolidate a huge amount of regulatory power under the Federal Reserve, a private banking agency that was at the root of our unfolding financial crisis.

The time has passed when Obama could have pointed to the past mistakes of his predecessors as the fault for our problems. Thanks to Tim Geithner, Barney Frank, and Larry Summers he now owns the financial crisis, and the coverups, policy errors, scandals, conflicts of interest and bailouts that have occurred since he has taken office.

His reappointment of Ben Bernanke as Federal Reserve chairman most surely tied a bow on his ownership package for the crisis, which is in danger of becoming his 'financial New Orleans.'

BusinessWeek

The U.S. scientific innovation infrastructure has historically consisted of a loose public-private partnership that included legendary institutions such as Bell Labs, RCA Labs, Xerox PARC XRX, the research operations of IBM IBM, DARPA, NASA, and others. In each of these organizations, programs with clear commercial potential were supported alongside efforts at "pure" research, with the two streams often feeding one another. With abundant corporate and venture-capital funding for eventual commercialization, these research labs have made enormous contributions to science, technology, and the economy, including the creation of millions of high-paying jobs. Consider a few of the crown jewels from Bell Labs alone:

- The first public demonstration of fax transmission (1925)

- First long-distance TV transmission (1927)

- Invention of the transistor (1947)

- Invention of photovoltaic cell (1954)

- Creation of the UNIX operating system (1969)

- Technology for cellular telephony (1978)

... We should not underestimate the magnitude of the job creation challenge. Outsourcing and extended recessions are not the only job destroyers in our system. There is also the constant pressure of value migration (the flow of value from old business models to new), which continues to be the major force reshaping our economy and will eliminate a large number of jobs in the next decade. (Think of all the old business models you know, from newspapers, to printing, to landline telephony, to the mighty, but now vulnerable, PC).

As a consequence of exporting good jobs that are not fully replaced, the U.S. demand engine is broken. Of the roughly 130 million jobs in the U.S., only 20% (26 million) pay more than $60,000 a year. The other 80% pay an average of $33,000. That ratio is not a good foundation for a strong middle class and a prosperous society. Rather than a demand engine, it's a decay curve. As a nation, we have papered over our declining incomes by accepting the need for two incomes per household and by borrowing heavily, often against paper assets inflated by financial bubbles (dot-com and housing). In recent years, personal debt has grown much faster than personal income. In 1985 the ratio of household debt to household income was 0.7 to 1; in 2000 it was 1 to 1; in 2008, it was 1.7 to 1. We earned less, so we borrowed more. In 2007 we reached our limit.

Selected Comments

max

- Soothsayer

Aug 30, 2009 11:43 PM GMT R & D is only the tip of the iceberg. Even if new products are developed, they are manufactured in Asia. Most R & D has already been outsourced to India. No, the real problem is 35 years of neoliberal economic policy exactly the same as that which brought us the Great Depression. The real problem is 35 years of supply-side emphasis. Only now are we discovering the paradox of supply-side economics. There is no demand no matter how low the cost of the product. Corporations run this country. Congress, the President, and all the rest in government are just sock-puppets of corporations. Unless and until you are willing to work for $0.57 an hour GET USED TO IT! It took 35 years to design the ship our country is in. Unfortunately the "engine" has broken down.

- logic Aug 30, 2009 11:35 PM GMT No no no, science and engineering is for lower caste people, losers. America's future is in outproducing the rest of the world in MBAs. We'll be able ignite a new economy based on financial engineering, and laugh as other societies get their hands dirty with "stuff."

I applaud this article and its desire to stop the downward decent of American technological and economic leadership. But it is too late for us. The question is longer if but when will China eclipse the U.S. as the new leader of economic growth and prosperity. PJL and Eric have correctly identified the problem causes. What is ironic is that one the loudest proponents of outsourcing and H-1Bs has always been BusinessWeek. Many people are now questioning if BusinessWeek is a viable ongoing enterprise. BusinessWeek should following the plays from their playbook. First, outsource all non-core functionally. Second, replace all journalists with H-1Bs who will work twice as hard and for half the pay. That should keep you going for one or two more years...maybe...talk about deserved karma.

crispin

Well they printed too much money and, now that real estate collapsed, judging by this article it seems they want us to be more productive so that they can have another place to store this $ thus preserving at least a little bit of its worth. That will not happen. You can't just print money and expect the rest of us to innovate, build, and do all of the things you can't do just so that you can preserve your position. All you can do now is increase the minimum wage and encourage population growth (birthrates/immigration). Oh yes, and see if you can resist the compulsion to print money. But the innovation is gone, long gone, and all that's left are the copycats and middlemen, and creating national labs and an industrial policy will not work because talented people will very soon no longer be willing to work for dollars.

Cold War fallout

As a previous post noted, the Cold War drove much of this country's innovation -- providing stable, high-paying engineering careers that in turn supported manufacturing jobs that helped build the middle class. I'm surprised the author didn't acknowledge this. My EE degree straddled the formal end of the Cold War, and the contrast in demand for engineers was stark.

Aerospace engineers especially had their careers end before they even started.

Noelle

If Americans want scientific innovation, then they are going to have to start treating their scientists better. A science PhD is expected, after all that education, to work for 30k a year in a job with no security called a post doc, often even when he plans to go into industy. Meanwhile some liberal arts kids straight out of undergrad can go to wall street and become traders for 100s of thousands. Hello? No wonder all of these scientists go into the derivatives field.

Doc

Let's see, Wall Street analysts said my profitable Fortune 500 employer was spending too much on R&D - about 1% of revenue. So we cut 60% of the R&D staff and eliminated outside research support to universities. The institutional investors were pleased and analysts praised management for cutting fixed cost overhead. Let's just say the US has a bit of a culture change in the investment community if we are to survive as an economy that actually produces anything.

Gimme a BREAK!

EVERY religion warns us about the 'Money Lenders Outside the Temple.' NYC, Boston and Greenwich are the money lenders, and the dollar is our god....and Congress appears to be the 'broker.' JC: WHAT (dubious) value would a moon colony contribute? You know that pig of an international space station? It was supposed to cost a $100 Billion - it's WAY OVER that price, we picked up 75-90% of the cost over-runs, and it doesn't DO even 1/2 the things it was supposed to do. So you plan is to blow another 3 trillion dollars while our Nation ROTS FROM WITHIN???? There would be more WASTE and FRAUD than Bush's Wars for Discovering his Manhood.

Jackov

I became an aerospace engineer during the Cold War, when science drove industry. Now, I am a Senior in Finance, and planning to ride out the Great Recession with an online Fraud Risk Mgmt MBA. America has been financialized. Only short-term investments that attract private investment is feasible.

Robert Laughing

Interesting piece, but Mike and Pete are right on! When I do my reading, and shopping, I see thousands of garbage products, of NO REAL value. Look at Detroit and the unrivaled garbage it produced for 30 years! Look at furnaces, a/c, household appliances and you see really more garbage, that has changed very little in 50 years. Then, look at how much Govt spends PAYING BIG business, Colleges/Ivy League Unis, etc, to DO work/research that these BUSINESSES should be doing themselves. All I see is a huge Govt carrot, and NO STICK....our Congress is grossly corrupted by geriatric clowns, serving themselves, to the detriment of our Nation.

Look at the C17; it's been produced, the Pentagon has MORE than enough, but war mongers and two-faced Democrats want MORE, MORE MORE! And when the C17 continues to roll off the assembly line, a couple hundred WORTHWHILE projects go starving into oblivion.

Commie Stooge

Why has America's lead in Science evaporated? It's no accident that this has occured during the lat 30 years of Conservative ascendency. Just read "The Republican War on Science"; and "Anti-Rationalism in American Life" by Susan Jacoby. A majority of those voting for John McCain believe that the Earth is just 6 thousand years old! Schools in many parts of the US are reluctant to teach science, since school boards are often packed with conservatives & fundamentalists. Better to avoid evolution & the Big Bang entirely, rather than cause a controversy. Dover PA was just the latest battle: there will be many more.

Shantanu

I can't agree more with the author. The "perceived value" placed on fundamental research has declined sharply in the last decade because of misplaced understanding that free economy and private sector is best placed to fill that void. While it is not a USA specific phenomenon, it is most relevant in USA because it was such a power house and thrived on its intelligensia and ability to attract best scientific talent from anywhere in the world. Today's USA is very different. Success is financial, R&D is tactical, leadership is socialist, Innovation is synonymous with likes of Apple (when at best such things are polished incremental innovation). To be really innovative as a country, USA or others like China, need to invest in Fundamental R&D that can lead to new industries. Only way to kick start this sector is via pumping Government money. Both China and USA, have the government to do it. Can the "socialist" administration in USA think big and invest where it needs to, or will the "capitalist" government of modern China take the lead here? We are at a precipice, and this answer will determine the economic superpower of the coming century.

Snoz

Contrary to what Adrian asserts, there is no shortage of science/technology brain power in America. America can and will make more science/technology break-through if capital flow from Wall St speculators and financial sector gamblers to R&D and manufacturing. With the help of government regulators, both speculator and gambler have siphoned capital from R&D and factory formation. America's politicians do not have the courage to abolish wage control so that American manufacturing power can re-emerge. While basic R&D is wonderful, it is the application of the R&D results to the manufacturing of goods that generate jobs and revenue. For too long, Wall St propaganda have persuaded investors that pushing paper investment is sufficient to sustain a modern economy. Recent financial meltdown proved otherwise. It is the "easy money" policy of the Federal Reserve that has encouraged rampant speculation on Wall St instead of channeling investment in business that pursue science/technology break through

Luigi

While the argument presented is reasonable, it fails to consider a significant change in the environment today compared to the grand era of basic science. The era was a direct result of an integrated partnership between government, industry, and academia resulting from Vandevar Bush strategic R&D vision. Many industries, like AT&T and Xerox had monopoly power and thus could spend lavishly on basic research. The government well funded R&D efforts were driven primarily by the Cold War. All 3 major institutions were supplied by well educated resources that came from a first class and stable educational system. That world was well ordered and relatively stable. Today's environment shares none of the above stable characteristics. Our school systems are chartered to educate a broad and unstable demographic of students. It is difficult to imagine the next generation of US students to be competitive with world class students from Asia in math and science. Education of the next generation is one of the most important tasks of government. Without a well educated (especially in math and science) population, a viable future is not assured.

JamesH

This country had a great thing going in Silicon Valley until all of the middlemen moved in and destroyed everything. There's no point in starting up something new because the hustlers will just follow the scent and destroy the innovation.

Printing money at the federal level in the hopes of creating a tech boom failed utterly, as all of the money was funneled directly into worthless garbage such as Google (hilariously listed as a legitimate research company alongside the likes of DuPont, 3M, and IBM) and other such media creations for example the social networking trend.

Innovation can rise again but only if the gatekeepers are forcibly evicted and/or permanently banned.

Otherwise, the US's competitive advantage will deteriorate significantly and irreparably -- to the delight of the glory-hunters, no doubt, who if truly honest with themselves will simply admit that they never actually cared about this place anyway.

"There's been a significant consolidation among the big banks, and it's kind of hollowing out the banking system," said Mark Zandi, chief economist of Moody's Economy.com. "You'll be left with very large institutions and small ones that fill in the cracks. But it'll be difficult for the mid-tier institutions to thrive."

"The oligopoly has tightened," he added.

The Baseline Scenario

...now it’s all about whether you are a preferred client of Goldman Sachs or another big finance house.

If you’re on the inside track, this is a great time to buy US assets that are being dumped by people without access to cheap credit, or assets overseas (e.g., Asia, where the “carry” or interest rate differential relative to the Federal Reserve is already positive and the exchange rate risk is all upside).

If you’re on the outside track, you are experiencing a version of Naomi Klein’s “Shock Doctrine”. Some (former) members of the elite are in this category – this is another standard feature of emerging market crises and “recoveries”. But mostly, of course, it’s nonelite on the outside track and a more concentrated, reconfigured version of the elite on the inside.

This can lead to short-term growth – the speed of recovery in many emerging markets surprises many, from about 12 months after the crisis breaks. But it also leads to repeated crisis, to derailed growth, and to a loss of income, status, and prospects for most of society.

Selected Comments

How bleak and horrible the prospect is. It sure is the shock treatment. Everything Simon has written on this is correct. The term banana republic, heard more and more especially since Katrina, is no joke. It’s precise.

But Americans are going to insist on their zombie first-world middle-class delusion. They’d rather sink into poverty with only that delusion to keep them warm, than brave the bracing wind of cold reality in order to try to take action to actually recover what’s supposed to be their country.

As for the small banks, the last time that was written here I argued they’re probably worried that any ostensible new regulation would probably end up being hijacked for the benefit of the big banks.

While I still think that’s a plausible outcome with the Congress and “regulators”, it’s also true that they could try to go over the head of the political structure and right to the people. Simon refers to the media, who I suppose might be in play to some extent, though so far they too have mostly shilled for the TBTF ideology.

I guess by now I’m frustrated at how the only sane and angry expression on this subject is limited almost completely to the blogosphere.

Why were there never any of these protests against the bailouts? It seems like, as hostile as so many people are to this (and to so many other things), no one has any will to try to do anything about it. The only action has been from the astroturfs (if I recall correctly, the “teabaggers” first arose not in response to bank bailouts but to proposed mortgage mods). It’s all calibrated to show the masses the semblance of protest and give them plausible-sounding slogans even as the focus in every case is against the public and in favor of the very corporations already plundering the public.

I don’t know what’s more sickening, the evil of the manipulators or the gullibility of the public.

Oh well, they’re being shocked.

CertifiedRez

“I don’t know what’s more sickening, the evil of the manipulators or the gullibility of the public.”

Both equally nauseate, though gullibility troubles more given it’s sound-bite origins that have become more than ever a defining quality of American society. As tea-baggers and town-hallers have evidenced, big media can (and often will) turn logic on its head and supplant reasonable discourse with unbridled passion and fear.

“guess by now I’m frustrated at how the only sane and angry expression on this subject is limited almost completely to the blogosphere”

So am I. But it really doesn’t surprise that the topic being discussed here today exists only (at least for now) in the blogosphere, where matters as important as these are so diffused. But I’m not discouraged. Would HFT have become a headline event had ZeroHedge not been on the issue months before it became Bloomberg, FoxNews, CNBC fodder? Would the alphabet soup of financial instruments and shell corporations having caused the crisis reached the public consciousness had so many experts in the craft not been at the keys with analysis? Probably not.

I believe as difficult an adjustment it will be for all who prefers trust over analysis, or faith over evidence (who, again, usually are the gullible un-empowered by misinformation, left prey for those that benefit from the informational asymmetry), the work Simon and James do here, and others elsewhere, reverberates. And the tenor of our comments do as well. Keep the faith.

anne

We have invested huge amounts of capital to prop up “too big to fail” companies that led us to the brink of catastrophe. ALL of us outside of Wall Street have seen an exceptionally poor return on that investment – but those at the TBTF firms are on track for record bonuses. And the firms have grown even bigger, making government support and federal financing a permanent fixture in our economy.At my end-of-summer block party last week, in two of ten homes, the primary wage earners have become unemployed this summer (both middle managers dropped from Fortune 500 firms hard hit by the recession.) A family around the corner (not included in this particular small block party) is also experiencing the woes of unemployment.

These are hardworking, college educated people. But not Goldman Sachs clients. So they’re irrelevant to the policy makers. We all know that too. And wonder how our nation will survive the “jobless recovery.”

At some point, policy makers will have to realize that the financial sector is not the economy, and that the money it is sucking up is not a productive use of our national funds.

Teotac

The policy makers will not realize it while the rest of the Treasury-buying world (ie China) continues to loan money to finance our debt-addicted, crack habit spending ways. When the world wakes up to that fact (and here I proscribe to the tipping-point theory), the gig will be up, interest rate control, inflation and dollar collapse will hit us accross the board…. at that point finger pointing will be useless, and The End of The American Century will come to a most startling finish.

Other than that, I think we have things pretty well under control…yay for the greenshoots!!

Paul

Another way of looking at the two track economy- those who are tied to government or have great influence of government have severely tilted the playing field to benefit themselves and have left the rest of us to survive on the leftovers of their feasting. It is just not the financial oligarchs, but the lawyers, the politicians and their staffs, the government employees, particularly the public employee unions, the farmers, the Seniors, the lobbyists, the quasi-public foundations, the Universities, the insurance industry, the defense and other public works contractors and all those who regularly feed at the public trough.

Not only are individuals in these favored sectors substantially overpaid, but many of these industries, particularly the lawyers and the financial services industry have rigged our regulatory system to make their roles almost indispensable in the workings of everyday commercial life.

The problem with a highly regulated economy like ours with our all too often opaque, decision making process, is that those who have undue influence on the regulatory process will over time garner substantially more than their share of our economies’ rewards. That is just how system is working now. Plus, this undue influence is essentially an enormous tax on productive work, which makes the cost to the public of ordinary commercial services and products much more expensive than they ought to be. Real Growth and the true cost of living has declined dramatically as a result. This is what has happened to our economy.

The political influence of the favored interest groups have warped our social welfare state and regulatory structure to produce this two track economy. Until the excesses of the favored interest groups are addressed, the phenomenon of the two track economy will only become more pronounced.

Bond Girl

The increased consolidation within the financial industry makes financial “reform” one big catch-22; this is what your arguments for consumer protection overlook.

What are regulators going to do when these institutions misbehave? Fine them? They can’t fine these insitutions a meaningful amount (read: an amount that makes misbehaving something more than a mere cost of doing business) because that will cut into their profitability. And what is good for the profitability of the institutions that issue 2/3 of the credit cards in the country and 1/2 of the mortgages is good for the country, right?

On the other hand, if they do not find a way to discipline the big players in the system, they are just going to act to increase their share of whatever is left of value in this country.

We’ve basically institutionalized the process of capture.

On the other hand, I’m not sure breaking up the banks will achieve what you think, either. Smaller banks have been very effective at organizing themselves to promote their political interests. And I’m not sure how one would go about breaking up the large banks when government agencies do not even really understand what the banks are doing, mechanically-speaking, not to mention the instability that would create in the meantime. I think we need another alternative here.

Talkingcat

Interesting and good posts, Bond Girl.

I am minded of the Oil Industry, where in the past the small independents were very successful at pressuring the government to beat up on the Majors on many occasions.

Still, perhaps with lots of small and politically effective banks, we would have just regular regulatory capture, not super-regulatory capture like we have now.

The point about the difficulty of un-winding a too-big-to-fail bank emphasizes the importance of these ‘funeral plans’, no?

Bond Girl

Well, it is one thing to say it is a good thing and another thing to actually accomplish it. Is there going to be a grand architect of the financial industry that is going to sort out all the inter-relationships these companies have and decide their smaller form? Who could possibly fill that role?

Another thing people do not seem to grasp is that we do not actually have large and small financial institutions in this country. We have large financial institutions with large financial institution products and we have small financial institutions with large financial institution products. People who think small institutions are grand are really just being manipulated by some genius marketing.

The size of institutions matters and it doesn’t. I think financial crises occur when the preponderance of market activity is subject to lower standards; it has little to do with the actual players. You can have a financial crisis with a lot of small players that made a lot bad loans and you can have a financial crisis where a few major players made a lot of bad loans. Both tend to end in the government taking responsibility for the system itself. We probably do not see this right now because our small bank failures are really only getting going, and we are only now confronting the problem that we are running out of qualified participants to absorb the bad apples. (Which leads to what? More consolidation?) I don’t know, I might be surprised, but I think being a large institution merely makes it easier to take down the system, but it is not a necessary condition for doing so.

One more idea on how to change behaviors of the bankers – pass a regulation that caps wages at $400,000 for anyone (not just those in the C-Suite) who works in a financial institution that accepts federal aid, bailout money, etc.

So no bonuses or multi-million dollar salaries if you work at a place that profits by relying on federal welfare programs.

I think you’d see a remarkable behavioral transformation almost immediately if bankers realized their high-risk behaviors could hurt their pocketbook. They obviously don’t care about the bank’s bottom line, but I’m sure they care a great deal for their own bank accounts….

CertifiedRez

We can begin with ending the conflict of interest between regulators and those they regulate by discontinuing the way these regulating entities are funded. For instance. I’m an appraiser. I hold a state license and am regulated by the issuing state entity. The state entity is largely funded by licensing fees. What incentive is there for this body to pro-actively regulate its members when uncovering widespread fraud would diminish its funding source. It bears stating these bodies are generally under-funded to begin with and cannot monitor its members effectively. While appraisers are low-hanging fruit in the finance matrix, their impact on the system is undeniable when similar disincentives across the whole credit-creation process places untenable pressure on those charged to maintain good character. This post at ZeroHedge yesterday on the SEC’s conflict of interest brilliantly illustrates my point.

http://www.zerohedge.com/article/why-sec-irreperably-conflicted-issue-high-frequency-trading

Up to 1,000 banks could fail in the next two years, private equity chief John Kanas told CNBC in a recent appearance. Kanas' high-powered private equity conglomerate -- which included the buyout titans like the Carlye Group, the Blackstone Group and W.L. Ross -- bought Florida's failed BankUnited in May.

According to Kanas, the second wave of failed institutions will include hundreds of smaller banks. "Many of these [failed] institutions no body has ever heard of," Kanas said. "It augurs poorly for smaller business mangers," he added. "Very small banks tend to lend money to small businesses -- this exacerbates the problem for small companies."

More from Kanas:

"Government money has propped up the very large institutions as a result of the stimulus package," he said. "There's really very little lifeline available for the small institutions that are suffering."

lavy:

Ben Brenanke is a small town schmuch who has agreed to be the boy. That is the only way that an American youth rises. It surely has not been on the strength of his ideas. Come on, " savings glut". I know that Brad De Long and our host support this idea (at least they used too).

At the end of the day, this man is a tool of the Plantation Capitilst movement that has little or nothing to do with the crap they are teaching at the University.

2009-08-27 | CalculatedRisk

From Reuters: U.S. mortgage delinquencies up in July: Equifax

Among U.S. homeowners with mortgages, a record 7.32 percent were at least 30 days late on payments in July, up from about 4.5 percent a year earlier and 7.23 percent in June, according to monthly data from the Equifax credit bureau.There numbers aren't directly comparable to the MBA quarterly numbers, but this shows that delinquencies are still rising.Doc Holiday :

Whose Rally Is It? - WSJ.com

"It's this recent rally that's troubling many on Wall Street. It's not just a lack of corporate profits and decisive economic data to support such a move; there hasn't been any volume. Since May 7, when the S&P 500 traded 9.132 billion shares, trading volume has been on a long, slow decline. Last week trading barely topped four billion shares on several consecutive days, some of lightest days since the markets all but froze in the days leading up to the Christmas holiday last year.

Meanwhile, on Monday, trading volume in American International Group Inc. was nearly seven-times higher than three months earlier, Citigroup Inc. trading had risen 181%, and volume of another component of the S&P 500, E*Trade Financial Corp., was up 145%, according to Thomson Reuters Datastream."

Doc Holiday:

That is a great quote: "On Monday, 34% of all trading volume on the New York Stock Exchange was concentrated in three stocks: Citigroup, Fannie Mae and Freddie Mac, according to Thomson, and Citigroup alone accounted for 17.8% of all volume. On Tuesday, five stocks: Citi, Bank of America, AIG, Fannie and Freddie accounted for 36% of all volume, according to calculations by The Wall Street Journal's Market Data Group."

ShortCourage:

Yeah Doc, mine was a snark comment. But I am not so sure about when the newest flipper game will blow up.

I'm afraid it might go on longer than we all expect. It all depends on how long the ROTW plays along with this ponzi Treasury game.

Doc Holiday:

I swear the banks are just playing games with their TARP cash and engaging in collusion with HFT, as the SEC cheers them on. I guess it helps some 401K's, but the obvious nature of this bubble will result in a crash, and then what, we reward these assholes for conspiracy? It does seem this is all related to pumping up market prices for mark-to market swaps, and thus with all the new accounting (fraud) rules, maybe this is the next leg-up of the PPT,

I mean the other side of the coin, i.e, now that PPT has saved the crash through synthetic means, now it's time to pump things up into a bubble, where fundamental valuation has no relationship to earnings realities.......

I don't know what's going on, but, it doesn't look or smell right!

the rat catcher:

According to Mike Shedlock in this recent partial post of his shown below and from oh so many others in the financial community, frugality is in vogue with the savings rate up 5% for the peoples. Which peoples? The upper 20% or is it the upper 2%? Thank goodness the gooberment is borrowing and printing to make it all happen, but I do believe they really want us to spend this money as witnessed by their C4C programs popping up for mortgages, houses, cars, appliances, and oh so many things to come.

Advance your borrowing and consume so far into the future that you devour your great grandchildren's savings right now!

"Many people are living paycheck to paycheck, on the edge of disaster as highlighted in a new Monster Poll that reveals 34 Percent of Workers Have One Week or Less of Savings.

Over a one week period beginning July 6 and running through July 13, more than 16,000 visitors to Monster.com participated in the Monster Meter Poll question “If you were laid off without severance, how long would your savings cover your living expenses?”

- One Week or Less: 34%

- 2-4 Weeks: 16%

- 1-2 Months: 16%

- 3-5 Months: 14%

- 6 Months or Longer: 20%"

2009-08-27 | CalculatedRisk

From the WSJ: Recession Finally Hits Down on the Farm (ht Bob_in_MA)

The Agriculture Department forecast Thursday that U.S. farm profits will fall 38% this year, indicating that the slump is taking hold in rural America. ... The Agriculture Department said it expects net farm income -- a widely followed measure of profitability -- to drop to $54 billion in 2009, down $33.2 billion from last year's estimated net farm income of $87.2 billion, which was nearly a record high....This will probably mean lower food prices, from the WSJ:For most Americans, the chill in the farm belt is related to one of the few positives they see in this economy: slowing inflation. Prices farmers are receiving for everything from corn and wheat to hogs are down sharply from last year.

Mish's Global Economic Trend Analysis

Although the Fed's "Dual Mandate" is complete nonsense, I do agree with Lockhart on one key point: The US economy will suffer with Structurally High Unemployment For A Decade.

Selected comments

fedwatcher:

“You can lead a conservative corporate treasurer to a low interest loan to buy back shares, but you need a board approved bonus to make him do the deed."

civil-disobedience:

“Of course you can make the horsey drink. You just select the LONG WAY to the water. Horsey will be thirsty. And horsey will drink."

CENTURION:

“Civil Disobedience: From an earlier post, you wondered why BB was allowed to stay. Here is some conspiricy. Maybe HE made Obama president and this is the pay back. OR, BB and Obama both work for the same boses and THEY made them who they are.

Do you really think BB and Obama have any power or control? They are tokens, as in TOKEN, if you get my drift. They are both Affirmative Action babies who got what they have only through others. TOKENS. They are just the high class whores in the whore house and will be replaced when f'ng them gets too boring.

tenbeers:

“This comment copied below from a guest post's commenter at naked capitalism (a post which has a decidedly different viewpoint than many here would probably take) caught my interest. The crux of the article is that Obama is basically throwing away his opportunity for reforming our corrupt system by pandering to the middle and the status quo business elite, while the right will continue to oppose him because it never wanted him, and the left will abandon him because he's been a corporatist compromiser. I'm getting to where I agree with that, and without a course change, his opportunity is fading fast.

Quote:

It's clear that the current economic model is morally and ethically bankrupt. And not because fiat money is inherently unstable, although it is to some extent, but because the sense of civic duty on the part of the power structure became so feeble and the influence of nonsensical ideology so strong that it overwhelmed common sense and prudence, like a virus of thought.

The economy has been looted from the inside out in a giant ponzi finance scheme.

How to make it work across the board for everyone is a fantastically complex question.

One notion that seems clear is that free trade that saves a a dollar on a shirt but sends a million dollars in wages to a third world country has a limit, beyond which it contributes negative economic value. There's an equilibrium in there somewhere. Some free trade is good and some credit is good. But too much, like too much of a drug for a sick person, is destructive. This notion of equilibrium is missing in most economic thought that I'm aware of.

http://www.nakedcapitalism.com/2009/08/guest-post-obamas-teflon-melting-as.html

fedwatcher:

“BULL! Obama knows that he cannot rock the boat after the annual Jackson Hole Love Fest.

"Perception is reality", and the perseption that is being sold to us is today is "Happy Times Are Here Again".

We are Japan. {So far it has worked for them in the last 20 years, so why should we not give it a try?}

Banks are increasing lending to buyers of high-yield company loans and mortgage bonds at what may be the fastest pace since the credit-market debacle began in 2007.

... Lending to purchase loans rated below investment grade and mortgage bonds is part of this year’s recovery in credit markets. Companies sold $889 billion of corporate bonds in the U.S. this year, a record pace, Bloomberg data show. The Standard & Poor’s 500 Index rose 52 percent since March 9, the best rally since the Great Depression.

... The risk now is that new credit leads to more losses at a time when consumer and corporate default rates are rising. Company defaults may increase to 12.2 percent worldwide in the fourth quarter, from 10.7 percent in July, according to new York-based Moody’s.

Selected Comments from Naked Capitalism

zeropointfield

The model offers no new insight in my view. The threshold is the moment at which there is more debt in the system than there is an ability to pay it down. That's the point of no return.However, we already know enough about Ponzi schemes to know that they collapse at some point they all do.

The best way to avoid this is not to participate in one. Also the ability to predict the exact moment of collapse won't help you because everyone else will have the same knowledge. The best move here is not to play.

T.

This confirms the slow train wreck is headed for another disaster, rinse and repeat, with the end game destruction of the currency as Mises predicts.ndk"The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved."

Voluntary abandonment is out without a violent counter-revolution, not something to wish for. When this corrupt Fed and Wall Street cabal will get us to the end game is unclear, but hard to find a surer bet. But the dollar carry trade is getting crowded, and I'm scared to place big bets since one could get burned with the blowups along the way.

We clearly have not learned the lessons of the crisis, that leverage increases risk and fragility, period.We can't afford to learn that lesson in this environment. We can again invoke St. Augustine: "Lord, grant me chastity and continence, but not just yet."

But the American consumer's redeveloping that Puritan spirit. Without endogenous growth in wages and revenues, or any desire to borrow by credit-worthy corporations and consumers who see little opportunity of wage and revenue growth in the future, there is really no way to boost money supply other than to increase leverage and government debt. If we want money supply to increase and inflation to happen, fiscal deficits and the financial markets are about the only hammers we've got. Unsurprisingly, they're happy enough to cooperate.

All of this is exactly what I would expect from an economy with negative equilibrium real interest rates. We're settling very comfortably into Japan's world. Krugman demonstrated in his better days that government spending in that situation is at best just a palliative.

As a result, I still expect to see nominal interest rates and economic activity continue to drift lower as releveraging lowers real interest rates as well. Asset prices, squished between those two forces, will do their thing.

And if it proves valid, relevering will proceed until we hit a trigger point again.

Yep. A guest on some show made the interesting point that poorly stored commodities, like natural gas, are plunging, while those easily stored like gold and oil are surging. Again, exactly what would be expected from an economy with lowering real interest rates and depressed economic activity.

The good news is that releveraging and the associated drop in nominal yields will boost the value of boring securities like Treasury bonds as well, and those are likely to again be the assets of choice when that trigger point is hit. This gives me a very comfortable place to hurry up and wait for awhile.

ndk

Unsurprisingly, they're happy enough to cooperate.I should elaborate on why I find this unsurprising.

It's not just the moral hazard and implicit backing of the Government, although those are back and bigger than ever.

It's also the selective pressures that have been at work in our financial system since 1982. Time and time again, under the gentle guidance of Greenspan and Bernanke, and Treasuries such as Summers', aggressive risk-seeking has been actively rewarded.

Closing your eyes, pinching your nose, and just buying has been the key to success for years. This has two complimentary effects.

1) Excessively cautious money managers leave the business, as they are unable to match marks with their exuberant competition.

2) Systemwide, capital is gradually allocated towards risk-takers. Their vote becomes more and more important with time.

A full generation is plenty of time to firmly entrench risk-taking in both the institutions and individuals who have the power and influence. We have just extinguished another nascent wildfire.

Until the next, may these brave redwoods grow to the sky: we got the capital where we got it, and we got the managers we got, so I anticipate courage will be the order of the day for a long while yet to come.

PascalMtl

Unreal. We are headed for a brick wall with probability approcaching 1. As I expected, there was still ammunitions left for one last "shot in the arm" and we are all Bonzai on it... and the next downturn will present an impossible wall to pass, because the runner will drop dead.Change We Can???? RIIIGHT. What FUNDAMENTAL and BINDING change has been made to US or international financial markets and banking? Nill. Way to go, Barack the Saviour! You sure drove the last nail of cynicism into the coffin of hope! Not that the GOP would have done any better, by the way...

Zero, you say "The best move here is not to play"... but we ALL play indirectly via bailouts (future taxes) or pension funds! This Ponzi scheme is strictly impossible to avert for most people.

ronald

The weekly unemployment claims are a reminder that something terrible is wrong with the economy and backstopping the financial sector to increase risk taking does nothing to cure the problem.kackermann

The model sounds intuitive.The ideal market has a buyer for every seller instantly - total liquidity. When too many look to trade in the same direction, price either soars, or collapses..

Aggregating and packaging up boxes of debt to sell, I think, has some not-so-obvious negative side effects.

As a commodity, it is decoupled from the normal price signals of whatever the debt is funding. Inwestors just see the coupon and want more and more. They want 3 box of high yield, 10 boxes of AAA (cough) and whatever. The stuff becomes so popular, that in order to manufacture more boxes of debt, they have to actively go out and set traps to snare loans. Free House (assuming prices rise) - no questions asked, no signature required, don't delay, act now.

House prices were rising like crazy, but the price on a box of debt looks like it might even be going down. The more demand, the cheaper it gets.

What's in that box of debt? Don't know, don't care. It's what's on the outside of the boxes that inwestors like. It's covered in coupons. Coupons from Pyramid Investment Corp, and signed by a Mr. Ponzi Scheme. If not completely satisfied, return unused portion to US Government for full redemption. No questions asked.

The debt is impervious to market signals.

Who Is This Man’s Boss?

In light of the Bernanke reappointment, now seems a good time to ask a curious question. Who does the Fed Chairman actually work for?

The obvious answers don’t quite jibe. The POTUS and Congress, for example, supposedly work for you and me. In theory, at least, they are held to account by the voting process and beholden to “the American people.”

But the Chairman of the Fed is not exactly elected. He is more or less anointed by way of smoky backroom horse trading, in which there is a lot of whispering and assurance-seeking before the Chief Executive reluctantly agrees to endorse.