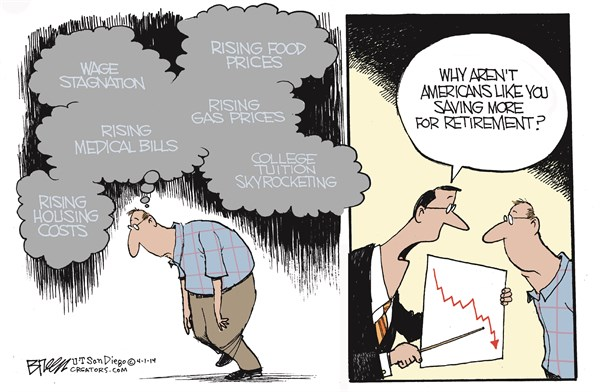

The key idea of a neoliberal regime is redistribution of wealth to the top 0.1%. and first of all

to financial oligarchy. So there is little wonder that ordinary citizens are deprived of hopes for secure

retirement to achieve this noble goal. that means that all gains from rising productivity goes

up the food chain and for lower 80% or so wages remain stagnant while cost of living trends up. And

one adjustment was to contribute less for retirement and use retirement as safety funds in case of unemployment.

This systemic shift of economic risks toward lower 99% of population is an immanent, fundamental feature

of neoliberalism not temporary aberration (so called "Last man standing" strategy"):

The elite 1% are playing a similar game against the 99% which I call “The Last Man Scrambling”.

Paul Rosenberg’s

latest essay

discusses a 2006 book by Yale University political scientist Jacob S. Hacker who explains how the

99% are being financially eaten alive by what is termed the “risk-shift” – the systematic shifting

of risk from large institutions onto the backs of citizens, including the most vulnerable among

us, under the neoliberal rhetoric of “individuals taking personal responsibility”...

So it is far from surprising that after the conversion of the society to

neoliberal model started under Reagan,

chances of "happy retirement" (aka "golden age") for lower 90% of world population (and probably 80%

of US citizens) became pretty slim. The key idea of neoliberalism is "Greed is good", or in other words,

if we increase inequality to max, we speed up growth (albeit mostly in financial sector ;-). And that

presuppose that, after we run out of cheap oil, wealth redistribution became the key "accelerator"

of economic growth. Which can be called "economic growth at any cost" and actually aligned perfectly

well with attempts of some countries to include into their GDP the revenue from prostitution and narcotics

trade.

Such policies hurts middle class and decimates lower class so retirement problem is just a tip of

the iceberg. The neoliberal elite is of strong opinion that 99% should be satisfied to get what trickle

down from the top 1% and should not complain. See

Why

America’s middle class is lost, by Jim Tankersley, Washington Post. And it goes without saying that

the top 1% grabs lion share of nation wealth and almost all gains because it can (as is "Yes we

can"). Corruption of regulators

guarantee that in this rather dirty and criminal redistribution process they never risk jail.

So "insufficient retirement funds" problem for, say, 90% of the population is an immanent feature

of neoliberal regime, not just an accidental result of 2008 financial meltdown. Investment banking has

been ruthless in dumping risk on hapless 401K lemmings. The stock run of 2013-2014 improved situation

for the most reckless part of savers, who adhere to "stocks for a long run" philosophy (akaNaive Siegelism),

but did not fundamentally changed it. The situation is considerably worse for those whom the meltdown

of 2008 frightened away from the stock market.

People in retirement or close to retirement were disproportionally affected: as stocks are inherently

riskier than other investments (and should be trimmed with age, as 100 - your_age rule

suggests), but interest on bonds precipitously dropped during Helicopter Ben actions to save financial

sector from complete meltdown.

Lack of retirement funds means that many seniors will be forced to work well past the traditional

retirement age, if (big if) they can find employment. Living standards for for 90% of seniors will fall,

and poverty rates will rise. It is important to understand that this is not an accident but the natural

situation under neoliberalism as a new social system. And the retirement crisis is the direct result

of conversion of the state into neoliberal model. Such a conversion imply

Dramatic growth of inequality with top 1% getting lion share of the wealth while 99%

face shrinking pie and relentless pressure to "increase productivity" created by global labor arbitrage.

Slashing retirement benefits and first of all elimination of defined benefits pensions

and replacement of them with inferior casino style 401K plans (defined contribution plans). Raising

the age to start collecting them as social spending are cut to allow top 1% to continue to get the

lion share of the nation pie. Companies have eliminated traditional pension plans that cost employees

nothing and guaranteed them a monthly check in retirement offloading all the risk into employees

and cutting or eliminating benefits

Increase in reckless financial behaviour based on greed as neoliberalism makes greed a virtue.

That include speculative "make money fast investments" in which many 401K lemmings wee fleeced.

That also includes "better then Jones" mentality which force many people cars and home they barely

can afford, cutting retirement contributions to a minimum.

Elimination of large number of salaried job and switch to temporary workforce. As a result

many boomerswere unable to save before the recession, and lost the job during it. Now their

wealth is disappear before retirement. As stagnation became permanent chances for old folk to find

employment became more and more difficult. Many need to accept severe cut in monthly salary to get

any employment at all. The Great Recession threw tens of millions of people out of work worldwide.

For many who kept their jobs, pay has stagnated the past five years, even as living costs have risen,

making it tougher to save for retirements cuing their banks and financing unemployment benefits

and other welfare programs.

Stock crashes which became a feature not an exception. Two neoliberalism caused crashes

of stock market (2000 and 2008) make a significant dent in 401K plans. Decimation of bonds returns

under Bernanke added to the injury as older fold should have larger part of their saving in bond.

"The low-interest rate environment has been brutal for retires: $500K in savings would yield $25K

a year at an interest rate of 5 percent, a nice supplement to Social Security, but just $10K at

2% percent.

Government budget deficits swelled both in Europe and the United States. Useless wars

and pressure from military industrial complex in one cause of rising deficits. In many countries

neoliberalism was exported on the tips of bayonets. In other via color revolutions which also cost

money (to bribe sufficient part of local elite). Another is oversized financial sector, which caused

spectacular crashes and due to the fact that it owes the government force on society its own bailout

like in USA in 2009. Moreover due to "Great Recession" tax revenue shrank, and governments pumped

huge amount of money into financial sector increasing the deficits.

Those factors of neoliberal conversion started under Reagan have been well documented individually.

What is less appreciated is their combined ferocity. There are also some negative demographic factors:

Retirees live longer and falling birth rates mean there will be fewer workers to support them.

Baby boomers will retire "en mass" during the decade of 2013-2023 stressing the system.

In other words 401K Donors to Wall Street (which as a cruel joke are called 401K investors)

are currently travelling on the Cruise Ship "Affluent Society" in Stormy Fiat Currency Waters to the

final destination, which might be the Frugality Island:-). Fleecing by financial oligarchy of middle

class retirements plans is the fact of the US life. Recent "crazy" run of S&P500 to 1800 eased the pain,

but structurally the situation essentially remains the same and, what raises fast, falls even faster:

...America’s overall retirement system is in big trouble. ...

Many workers used to have defined-benefit retirement plans, plans in which their employers guaranteed

a steady income after retirement. And a fair number of seniors ... are still collecting benefits

from such plans.

Today, however, workers who have any retirement plan at all generally have defined-contribution

plans — basically, 401(k)’s... The trouble is that at this point it’s clear that theshift

to 401(k)’swas a gigantic failure. Employers took advantage of the switch to surreptitiously

cut benefits; investment returns have been far lower than workers were told to expect; and, to be

fair, many people haven’t managed their money wisely.

As a result, we’re looking at a looming retirement crisis, with tens of millions of Americans facing

a sharp decline in living standards at the end of their working lives. For many, the only thing

protecting them from abject penury will be Social Security. Aren’t you glad we didn’t privatize

the program?

One important side effect of the transformation of the USA society into

neoliberal society since 1970 was offloading

risks on individuals. That's true for retirement too. Now with 401K plan it's individual who assumes

the inflation risk, interest risk (See

Bernanke

stole your pension), market volatility risks and structural unemployment (rampant in the USA) risks.

This neoliberal society now faces several

major crises which lead to the loss of power and prestige and as such deeply affect the US economy:

Consequences of outsourcing of manufacturing and raw materials production. Which led

to overproduction which in turn leads to a decline in profits, and as wages are squeezed to stabilize

profits. As a result demand falls further and further. Moreover the US, which plays the role the

consumer of last resort, cannot continue to borrow indefinitely. The IOUs that the rest of the world

accumulated will eventually have to be repaid.

Military overextension is a second important problem as the wars in Afghanistan and Iraq

demonstrated. Guerillas forces proved to be difficult to fight opponent. The US military is so strained

that it has to hire mercenaries from companies like Blackwater

The decline of legitimacy of the neoliberal ideology. Now neoliberal expansion on which

transnationals (which owns the US government) depends is more costly then in 90th.With neoliberalism

("Greed is good") under attack (including recent attack from

Pope

Francis), the US has lost its ideological supremacy it enjoyed in 90th. Because the US dominates

international financial institutions like the IMF, World Bank and most of the regional development

banks, their imposition of neo-liberal structural adjustments programs has led to a revolt against

their destructive policies as witnessed by the revitalization of the left political forces especially

in Latin America but also in the rest of the global South. Furthermore, the US bullying and

sometimes insulting treatment of the UN has further sullied the US's reputation.

The quagmire of domestic politics.Neocons

spend money left and right for color revolutions trying to preserve the USA as the sole superpower

on the planet, the position it acquired after the dissolution of the USSR. As Ukraine EuroMaidan

had shown recently, now it's a costly business. Added to this international de-legitimization is

the quagmire of domestic politics from

the surrender of civil liberties to Uncle Sam to the

patently obvious corporate

control of both major parties.

When a large number of old people expect to receive certain amounts from their retirement portfolios,

reductions in running yields end up reducing their monthly income. People were forcefully pushed into

stock market casino, in which of course Wall Street is the winner and ordinary investors are the losers.

Casino Capitalism, the internal version of neoliberalism the USA

and Great Britain has been nurtured and encouraged by a series of government decisions.

Of which creation of 401K plans was only one among many. There were also important decisions to deregulated

financial m and allow derivatives with the hope to replace income from manufacturing by income

from financial sector. In other words its was a counter-revolution of the part of ruling elite

that lost its influence in 30th (dismantling New Deal from above in the USA (Reaganomics)

or Thatcherism in the GB). As

Nancy

Folbre is an economics professor at the

University of Massachusetts wrote in her article Rowboats for Retirement (NYT,

Jun 24, 2013)

It feels so good to row your own boat. You’re the captain. You can set your own course and speed.

According to the boat advertisements, you are almost sure to reach your destination as long as you

pay for good advice, rebalance and row hard. Sure, there may be big waves, but you can ride them

out, and storms always subside.

A lot of people used to think of 401(k) retirement accounts this way. But in the last six years,

most Americans have gained a new appreciation of financial bad weather and the threat of a perfect

storm. Stock market volatility, low interest rates and a sagging bond market have discouraged retirement

savings.

Persistent unemployment and stagnant wages have left many workers treading water, struggling

so hard to stay afloat that they couldn’t open a retirement account even if they wanted to.

A

new report from the National Institute on Retirement Security, based on analysis of the 2010

Survey of Consumer Finances, shows that about 45 percent of all working-age households don’t hold

any retirement account assets, whether in an employer-sponsored 401(k) type plan or an individual

retirement account.

Among those 55 to 64 years old, two-thirds of working households with at least one earner have

retirement savings less than one year’s income, far below what they will need to maintain their

standard of living in retirement. By a variety of measures, most households, even those with defined

benefit pensions, are falling far short of the savings they will need.

It's very probable that without new technological breakthrough the USA economy as well as all major

Western economies are in "permanent stagnation" period. Stagnation of median wages may have been evident

for longer in the US, but the Great Recession has led to declining real wages in many other first world

countries. And semi-permanent rate lowering by FED and derivatives frenzy of major banks should probably

be viewed as the last, desperate attempt, if not to provide growth, then to provide an illusion of growth.

At any cost.

Generally, as return on investment in manufacturing diminishes more and more, money are chasing financial

assets, creating one speculative boom after another. And each of them sooner or later ends in spectacular

bust. Herbert Stein quote

"If something can't go on forever, it will stop" (which sound more like Baby Ruth quote ;-) is fully

applicable here. What is important to understand that "boom-bust" cycle now is the way neoliberal economy

functions. They are not aberration, they are the immanent feature of the system. The side effect

of fleecing 401K lemmings is in full accordance with the main idea of neoliberalism: redistribution

of wealth between top 1% and the rest of population. And any attempt of more equitable sharing of wealth

face huge, emotional resistance of "Masters of the Universe" one of which recently compared such attempts

with Hitler's Kristallnacht (Progressive

Kristallnacht Coming — Letters to the Editor - WSJ.com)

For an individual investor it is impossible to predict when such a bust happens. But it is reckless

not to take into account this possibility, when financial assets appreciate like there is no tomorrow.

Again for a regular investor the game now is not about the return on capital, but the return of capital.

This neoliberal invention called 401K is, in essence, a privatization of retirement plans. And

instead of growing the funds, many people discovered that it actually impose a tax of savers because

it offloads all kind of investment risks on the individual. It also created a huge and semi-parasitic

industry of mutual funds, which try to lure 401K investors in stocks. Those who were saving in bonds,

especially in bond mutual funds and ETFs now face dramatically lower returns due Bernanke helicopter

money and bringing short term rates below inflation, In no way they are safe. See Coming Bond Squeeze.

Read Saving your 401K (or may be not now and

access to this page strongly depends on the value of S&P500; when S&P500 is above 1700 few people read

it, but it was an avalage in 2008 and 2009 when S&P was below 1000 ;-).

Even the current, high value of S&P 500 that does not change general situation: what is proposed

for lemmings in 401K plans is not investing, but gambling with Wall Street as the casino owner (aka

Casino Capitalism). As such there is a distinct possibility to

be a victim of computerized financial warfare of Wall Street with middle class. The financial elite

also lusts after Social Security money, and would love to have it transferred over to them for 'safekeeping'.

The news isn’t good about the shift from defined-benefit to defined-contribution pension plans for individual

investors. Wall Street behavior is sticky. As John Kenneth Galbraith noted:

"People of privilege will always risk their complete destruction rather than surrender any

material part of their advantage."

In selecting you allocation try to fight greed and opt for security. The working hypothesis should

be that you probably can beat inflation in 401K, but that's about it. Don't expect anything larger then

that -- all profits belong to Wall Street not you.

This, more cautious strategy, includes avoidance of anything that has a slightest shadow of

possible scams involves. Stakes are just too high.

Warning -- Warning !Warning !

Please read section about

retirement

scams first !!! This is real danger for those close to retirement and all people already

in retirement. Targeting is very sophisticated and the fact that you have a university diploma

might not save you, unless you understand the risks.

Often scamsters are seniors themselves and live in the same community and/or attend the

same church. Remember, if the investment it too good to be true it usually is.

Now in order to survive, many financial advisers are faced with tough choices. And this

type of behaviors is no longer limited to sleazy "cold-call" financial advisors.

Moreover, there are three important factors that IMHO dictate extreme caution as for stocks holdings

for people who are close to retirement (see discussion at

Economist's View for more details)

Stock market like Ponzi scheme depends in entering of new and new players for growth.

That condition held true when baby boomers aged and stock market dramatically risen as self-fulfilling

prophecy, but now is it less true and may even became false.

Quality of corporate earnings is now extremely low. Most of this often sited "increased

profitability" is just result of draconian cost cuts across the board. Large corporation are

still shrinking their workforce in order to maintain the level of EBITRA earnings. This scorch land

policies can't last indefinitely. I think without some kind of technological breakthrough, the situation

can spin out of control in less then a decade. So far corporations did not shred "all the fat" but

in some areas (for example IT) they are close.

The current unemployment is structural. Computers and

outsourcing really eat people jobs. They will never return, at least good paying portion of it which

sustained the middle class. So there is big difference between "Clinton years" and "Obama years."

During Clinton years many created jobs were relatively well-paid IT and financial sector jobs. Even

later, during Bush II years, a lot of them were construction jobs. Right now most of newly created

jobs are service-sector McJobs. That pay less then $15 per hour. This sad development impoverishes

population and dampen consumption from the lower 60% of population considerably (although in the

USA consumption is mainly top 10% game in any case; lower 60% simply does not matter; that why consumption

is so resilient to economic slumps).

Neoliberalism is now entered

zombie phase and that creates some difficulties for the US government and US global corporations

in pushing their agenda through the other countries throat. Those difficulties might increase

in he future. Just count the number of left governments in Latin America now and in 1991. It can

still attempt to expand, but in any case the gold years of neoliberalism after disintegration of

the USSR with subsequent colonizing the new half-billion people economic space (the key source of

Clinton's years prosperity) are over.

At the same time, the amount of funds you need for retirement now it difficult to estimate as you

now carry both inflation risk and market crash risks. That means that you need to put efforts in creating

a model (using Excel) suitable for your situation to have a realistic

assessment of what you need and can be adapted to the changing situation (for example ZIRP regime installed

by Bernanke and Co.). More or less comfortable monthly income now approaches $4.5K a month for a

couple of two, renting a modest two bedroom apartment, who wants and is able to travel (let's say one

trip to children, one vacation and one other trip, $2000 each, of $6K total per year):

Item

Monthly

Annual

Total expenses

4505

50760

Rent

1200

14400

Food

800

9600

Travel/Vacation

500

6000

Suppl Medical Insurance

400

4800

Car amortization (two cars)

400

4800

Car insurance (two cars)

150

1800

TV

120

1440

Gas/transportation

120

1440

Heating/air conditioning

100

1200

Extra expenses

100

1200

Drugs and out-of-pocket med

100

1200

Electricity

60

720

Presents to relatives

50

600

Cloth, computer, furniture, etc

50

600

Internet

40

480

Cell phone

40

480

But to get those funds by growing your 401K investments is a difficult task. At minimum, if one of

spouses gets SS $3K at age of 70 (so the other is eligible for half) you need approximately $300K of your own funds

to get from age 65 (or the time you lose your full time employment) to age 70.

You need to double that if you lose job at the age of 55.

As many IT specialists who reached senior age lose full time employment much earlier and are underemployed

since, you may need to dip at your 401K at some point of your life, so doubling this amount by shooting

for $300K in 401K for each of spouses is prudent. That's not that much but few people have that at,

say, 55. Generally it is realistic to assume that since 60 you will be underemployed and can't get more

then 50% of previous salary. So you can't contribute to 401K any longer. Most of available jobs now

are McJobs in service sector.

Yes, once in a while stock market performs a spectacular run and that can help. But the question

is whether it last. Who would expect that when the USA economy is still in zombie state with high unemployment

S&P 500 would reach 1667 as it did on May 17, 2013.

But for each 100 days then stocks are at their five year peak level, there are ten different years.

And the key problem is that to one can predict when the fortune changes and at what level stock market

will be when you desperately need to withdraw money. In any case, the events of 2000 and 2008 for many

people were like losing half of money at a casino, then having the dealer smile at you and say "How

about one more try. Trust us. This time it will be different..." At this point, relations of Wall

Street and 401K investors look like in a classic scorpion and frog fable.

Boomers were brainwashed about "stocks

for the long run" and now they see that returns are below expectations (as of Feb 25, 2013

S&P500 grew 15% less in comparison to the same investment to

Pimco Total Return fund, if we invested from

01/01/1996 biweekly to Feb 2013). Of course, God knows what will happen with Total return fund after

Bill Gross left, but still...

As most 401K investors feel that they do not have enough money for retirement they tend to take outsized

risks and recently jumped back to stocks and junk bonds (aka reaching for yield), because

interest in regular bond funds and Treasuries disappeared (thanks to Bernanke Fed). Wall Street

is famous for royally fleecing such people.

As most 401K investors feel that they do not have enough money for retirement they tend

to take outsized risks and recently jumped back to stocks and junk bonds (aka reaching

for yield), because interest in regular bond funds and Treasuries disappeared (thanks

to Bernanke Fed). Wall Street is famous for royally fleecing such people.

Even the recent fuelled by Fed money printing boom in stock prices is no escape: in the current

oil-constrained US economy stock prices have been sliding in real terms (inflation adjusted) since the

2000 peak, and every time after peak they suffer a collapse. Two most recent were in 2001 when

S&P500 fall to 720 or so from 1460 and in 2009 when S&P fall to 670 or so.

You can't predict the time of the next collapse, but you can be sure that it will happen in the most

inopportune moment then you vigilance is at low after a relatively long and steady period of growth

of stock values. It can happen in 2015 it can happen in 2020 but generally each ten years there is a

risk of such calamity.

When Wall-street pump-and-dump insiders start a dump phase, the Fed opens the credit tap to push

them back up, thus the oscillating pattern around a downwards trend in 2000-2012 But at the end a stock

crash occures that those who paniced give a lot of money to Wall street speculators. Can it modern method

of redistirbution of wealth from lemming to Wall-street sharks, if you wish.

One positive for 401K investors trend is that S&P500 became like another government statistics. That

means that it is the US government who now desperately wants to stop or slow the decline of the S&P500,

because the S&P500 goes down, most pension funds and other insurers blow up... As Greenspan argued recently

the main goal of FED policy is to boost stock prices (and house prices).

But at the same time ZIRP — the near zero percent rates sinking already retired Boomers retirement

dreams and undermining prospects of happy retirement for those boomers who still work. Some can't bear

the pressure and do move assets back into stocks reaching to yield. They can be lucky, but if they are

not then the next crisis will wipe out that paper gains in no time like has happened in 2008. And there

is no guarantee that the third great robbery of the century is far away: halfway across that stream,

scorpion again will show the frog its true nature…

That's why the first thing in retirement planning is to learn

Excel. Even with crappy rates your Social Security will kick in at 66. Your financial situation

will be better if you can wait till 70 to start getting SS. In most cases this "66-70" increase

in SS constitute tremendous help. In other words minimal size of 401K should give you the ability to

postpone Social Security till 70.

Also with crappy interest rates you need to understand that your health is becoming your most valuable

asset.

Minimal size of 401K should give you the ability to postpone Social Security till 70.

Generally IT staff can't assume that they will be employed till 66, so it is better to reach

this amount around 60. That means that you should strive to contribute the amount which at 60

"theoretically" makes you 401K sufficient to support "self-financed" retirement for 10 years.

Assuming $60K a year and 3% return after inflation a year that comes approximately to $500K.

With $12 a year ($6 an hour) supplementary income you need only $400K and with $24K ($12 an

hour) supplementary income this amount drops to $300K.

It's not a rocket science to calculate approximate year-by-year expenses from the day of your

retirement/unemployment to your longevity expectation date +7 (very few people exceed their longevity

estimate obtained usingRetirement &

Survivors Benefits Life Expectancy Calculatorby more then five years) .

This way you can see that you do you not really need to play in the stock market casino that much.

And get an approximate calculated amount of safe funds (and your monthly contributions) that will allow

you to live frugally, but securely without taking outsize investment risks. Here is an example of such

a basic estimate:

Life Expectancy Calculator

The following table lists the average number of additional years

a male born in 1950, can expect to live when he reaches a specific age.

If you are at Age

Additional Life Expectancy

(in years)

Estimated Total Years

63

20.5

83.5

66

18.3

84.3

70

15.5

85.5

The means that as you (and your wife) age, you better decrease your equity exposure to the level

where your minimum life expenses are covered without your stock part of the portfolio.

For the examples table below shows minimum monthly expenses obtained by drastically downsizing retirement

life style shown above:

Item

Monthly

Annual

Total expenses

2470

29640

Rent

800

9600

Food

800

9600

Travel

100

1200

Suppl Medical Insurance

0

0

Extra expenses

150

1800

Car amortization (one car)

100

1200

Car insurance (one car)

100

1200

Gas/transportation

60

720

TV

80

960

Drugs and out-of-pocket

100

1200

Cloth, computer, furniture, etc

50

600

Presents to relatives

50

600

Internet

40

480

Cell phone

40

480

This calculation means that you probably can survive on around 60% of your "desired" retirement income.

Unfortunately this involves pretty big sacrifices in life quality. So in no way you can allow you next

egg to drop 50% due to stock market calamities, as happened in 2008. So please remember that the game

is rigged and it's you who might pay the price of all this gambling...

But here with almost no cushion you need to be aware about growing medical expenses. Like with older

cars, maintenance became more frequent and more expensive with age probably doubling each ten years

after 60.

In order to model your personal situation in Excel more realistically

on year-by-year basis you need just a few inputs such as:

Life expectancy (there are good calculators available on the Web such as

MSN Money

calculator). As a rule of thumb, a person without serious diseases (asthma, diabetes, etc) who reached

age 60 are expected to live another 22 years, if he is a male and 26 years, if she is a female (see

Wisconsin Life Expectancy

2006-2008)

Medical expenses estimate (including "out of the pocket", which can be channeled via

Flexible saving account to avoid taxes on such spending).

Before tax savings, including 401K and Roth account savings (they should be treated differently

as separate items as tax consequences for them are different -- Roth distributions and income are

not taxable. )

After tax savings. Everything else you have.

Social security. Use the estimate provided by government.

Value of your house, if any and/or your gold/precious metals, if any. This class of assets

generally can be viewed as protected from inflation.

Comfortable minimal level of monthly income (depends on the area where you plan to spend

your retirement, there are expensive places to live and less expensive places to live; also modest

changes in life-style typically can cut expenses 10% or so)

After that you need to create you first simple spreadsheet, with the columns such as Total assets,

Interests income, SS income, Pension (if nay), Other sources and Expenses columns like listed above.

Each row of the spreadsheet should correspond to one year. Some cells can be initially calculated manually.

You will be surprised how much information you can get from this simple exercise.

Boomers not only can get clobbered by the impact of market volatility, they also can lose purchasing

power due to inflation. In other word the UIS elite offloaded the long term economic risks from

states to individual. That offloading is the hallmark of neoliberalism as a "secular religion", the

ideology that still is dominant in the USA.

This another reason why increasing the share of equities is a questionable solution to the problem

of unsufficient retirement funds. A better solution is to think of retiring with a part-time job until

age 70. Even McJob: one realistic plan to enhance your retirement financial security is to continue

part time working till 70. That not only allows to maximize

the Social Security pension but also allow you to dispose your unprotected from inflation assets

in a shorter time frame, lessening the impact of inflation.

Getting part time job not only allows you to get supplementary income easing the requirements to

the size of your private retirements assets, but it permits some of us (especially for former

office slaves, may be the first time in life) to realize untapped in regular work potential. The first

$12K of income are generally tax free.

People do miss their jobs - even jobs they hated. I have never seen statistics, but my experience

suggests at least 50% of those who quit without another job regretted the decision. One discussion

list posted a note from a 40-something woman who had chosen enjoyable, low-paying jobs to "get most

of her life". Now she is against the wall, with no nest egg to fund a career transition and no options.

In any case don't be suicidal and try to compensate insufficient funds by buying some complex financial

product from Wall Street. As one trader put it (naked

capitalism, Aug 02, 2013):

“My advice to people dealing with the financial sector is: never buy anything that’s complex.

Because the more complexity the more opportunities there are to screw you over. I just

can’t get my mind around how banks can still call clients in the corporate world and say, look we’ve

got this great idea that’s going to make you a lot of money.

I mean, what are they thinking? Nobody in the City can be trusted because they don’t work

for you, they work for themselves.”/

In 2005, nearly 5.5 million households were subject to mandatory withdrawal requirements for individual

retirement accounts and 401(k) plans. In 2008 they faced an problem. If you, for example need

to withdraw $50K and all you holding are in S&P500, which is 50% down you instantly lose $25K.

This week, the Internal Revenue Service

announced that people under age 50 in

401(k) and similar workplace

retirement

plans will be able to deposit up to $18,000 in 2015, an increase of $500 from this year. Those 50

and over can toss in as much as $24,000, a $1,000 increase.

Which is all fine and dandy for the

well-heeled and the frugal. But one of the biggest problems with these accounts has nothing to do

with how much we can put in. Instead, it’s the amount that so many people take out long before they

retire.

Over a quarter of households that use one of these plans take out money for purposes other than

retirement

expenses at some point. In 2010, 9.3 percent of households who save in this way paid a penalty to

take money out. They pulled out $60 billion in the process; a significant chunk of the $294 billion

in employee contributions and employer matches that went into the accounts.

These staggering numbers come from an examination of federal and other data by

Matt Fellowes, a former Georgetown

public policy professor who now runs a software company called HelloWallet, which aims to help employers

help their workers manage their money better.

In a paper he wrote with a colleague, he noted that industry

veterans tend to refer to these retirement withdrawals as “leakage.” But as the two of them wrote,

it’s really more like a breach. And while that term has grown more loaded since their treatise appeared

last year and people’s debit card information started showing up on hacker websites, it’s still

appropriate. Millions of people are clearly not using

401(k) plans as retirement accounts at all, and it’s a threat to their financial health.

“It’s not a system of retirement accounts,” said Stephen P. Utkus, the director of retirement

research at Vanguard. “In effect, they have become dual-purpose systems for retirement and short-term

consumption needs.”

How did this happen? Early on in the history of these accounts, there was concern that if there

wasn’t some way for people to get the money out, they wouldn’t deposit any in the first place. Now,

account holders may be able to take what are known as

hardship withdrawals if they’re in financial trouble. Moreover, job changers often choose

to pull out some or all of the money and pay income tax on it plus a 10 percent penalty.

The breach tends to be especially big when people are between jobs. Earlier this year, Fidelity

revealed that 35 percent of its participants took out part or all of the money in their workplace

retirement plans when leaving a job in 2013. Among those from ages 20 to 39, 41 percent took

the money.

The big question is why, and the answer is that leading plan administrators like Fidelity

and Vanguard don’t know for sure. They don’t do formal polls when people withdraw the money.

In fact, it was obvious talking to people in the industry this week and reading the complaints

from academics in the field that the lack of good data on these breaches is a real problem.

Fidelity does pick up some intelligence via its phone representatives and their conversations

with customers. “Some people see a withdrawal as an opportunity to pay off debt,” said Jeanne Thompson,

a Fidelity vice president. “They don’t see the balance as being big enough to matter.”

Or their long-term retirement savings matter less when the 401(k) balance is dwarfed by their

current loans. Andrea Sease, who lives in Somerville, Mass., is about to start a new job as an analytical

scientist for a pharmaceutical company. She was tempted to pull money from her old 401(k) to pay

down her

student loan debt, which is more than twice the size of her balance in the retirement account.

“It almost seems like they encourage you,” she said, noting that the materials she received from

her last retirement account administrator made it plain that pulling out the money was an option.

“It’s an emotional thing when you look at your loan balance and ask yourself whether you really

want to commit to 15 more years of paying it, and a large sum of 401(k) cash is just sitting there.”

So far, she’s keeping her savings intact.

Another big reason that people pull their money: Their former employer makes them. The employers

have the right to kick out former employees with small 401(k) balances, given the hassle of tracking

small balances and the whereabouts of the people who leave them behind. According to Fidelity,

among the plans that don’t have the kick-them-out rule, 35 percent of the people with less than

$1,000 cashed out when they left a job. But at employers that do eject the low-balance account holders,

72 percent took the cash instead of rolling the money over into an individual retirement account.

This is unconscionable. Employers may meekly complain about the difficulty of finding the owners

of orphan accounts, but it just isn’t that hard to track people down these days. Whatever the expense,

they should bear it, given its contribution to the greater good. Let people leave their retirement

money in their retirement accounts, for crying out loud.

Account holder ignorance may also contribute to the decision to withdraw money. “There is a complete

lack of understanding of the tax implications,” said Shlomo Benartzi, a professor at the University

of California, Los Angeles, and chief behavioral economist at Allianz Global Investors, who has

done pioneering research

on getting people to save more. “And given that we’re generally myopic, I don’t think people

understand the long-term implications in terms of what it would cost in terms of retirement.”

In fact, young adults who spend their balance today will lose part of it to taxes and penalties

and would have seen that balance increase many times over, as the chart accompanying this column

shows.

But Mr. Fellowes of HelloWallet, interpreting the limited federal survey data that exists, says

he believes that people raid their workplace retirement accounts most often because they have to.

They are facing piles of unpaid bills or basic failures of day-to-day money management. Only

8 percent grab the money because of job loss and less than 6 percent do so for frivolous pursuits

What can be done to change all of this? Mr. Benartzi thinks a personalized video might be even

more effective than a boldly worded infographic showing people the money they stand to lose. He

advises a company called Idomoo that has

a clever one on its website aimed

at people with pensions. If you want to see the damage that an early withdrawal could do, Wells

Fargo has a

tool on its site.

"Over the past five years, the S&P 500 stock index has more than doubled. For the past

10 years, it has nearly quadrupled," says Orman. "If you have left your portfolios on

autopilot, that could likely mean that you now own more stock than you intend to, or

should."

Left to their own devices, your increasingly valuable stocks may have started to account for

an even larger portion of your account

... ... ...

Orman cites a recent analysis from Fidelity Investments on the retirement plans the company

handles. Fidelity estimates about 20% of savers own more stock than they'd recommend for

someone of their age.

Retirees who have the most money pay the most in taxes, according to a

recent

working paper

, but they're not necessarily rich.

"Most of the tax burden is carried by the top quintile of households,"

Anqi

Chen

, co-author and assistant director of savings research at the Center for Retirement Research at Boston College, told

Yahoo Money. But "it's important to keep in mind that when we think about the top quintile of households -- the top 20% -- they're

not the super wealthy."

Those in the highest quintile are mostly married couples with average combined Social Security benefits of $50,900, 401(k)/IRA

balances of $325,400, and financial wealth of $441,400. When annuitized, those assets and retirement accounts earn account

holders roughly $3,000 per month -- or $36,000 per year -- ostensibly making them middle-income earners, Chen said.

"That's some money but not a ton of money," Chen said, "and these households will have to pay about 11% [in taxes]."

(Photo: Getty)

The highest quintile pays 11.3% on their retirement income, while the top 5% is taxed at 16.4%, and the top 1% is taxed at 22.7%,

according to the analysis. Overall, retired households pay 6% in federal and state taxes on their income.

Researchers used income data from 3,419 individuals and 1,907 households included in the Health and Retirement Study, a

nationally representative longitudinal survey of older Americans. The analysis assumes the retirees follow the required minimum

distributions for their retirement accounts and consume only interest and dividends from their assets.

The heavy tax burden carried by well-off retirees demonstrates that even those who enter their golden years with the most money

are still short on savings, an ongoing problem for many Americans. Roughly 40% of the top quintile of savers are at risk of

maintaining their standard of living, meaning "taxes will make the goal even more difficult to attain," the study said.

For the majority of retired households, "taxes are negligible," Chen said, paying 0% to 1.9%. But they are far from lucky.

Those in the "bottom two-thirds of the income distribution don't have a lot in financial assets" that yield material income in

retirement, she added.

Yahoo Money sister site Cashay has a weekly newsletter.

Stephanie is a reporter for Yahoo Money and

Cashay

,

a new personal finance website. Follow her on Twitter

@SJAsymkos

.

"... If you're married and your spouse is covered by a workplace-based retirement plan but you're not, you can deduct your full IRA contribution as long as your joint AGI doesn't top $196,000 for 2020. You can take a partial tax deduction if your combined income is between $196,000 and $206,000. ..."

"... Spouses with little or no earned income for 2020 can also make an IRA contribution of up to $6,000 ($7,000 if 50 or older) as long as their spouse has sufficient earned income to cover both contributions. The contribution is tax-deductible as long as your household income doesn't exceed the limits for married couples filing jointly. ..."

There's still time to make a 2020 IRA contribution and lower your tax bill.

by:

Sandra

Block

January 13, 2021

As you get ready to tackle your 2020 tax return, make sure you haven't overlooked one of the best ways to cut your tax bill

and secure your future -- funding a traditional IRA. (There is no upfront tax break for funding a Roth IRA.)

You can actually make an IRA contribution for the 2020 tax year up until the time you file your tax return, which is due April

15, 2021. But why wait? If you have some extra income – say, from a

stimulus

check

– go ahead and deposit it into an IRA account now before you forget. You'll also give the money a little more time

to grow, which you'll appreciate when you retire.

And what about those tax savings? Well, depending on your income, you may be able to deduct your IRA contribution on your 2020

return. To contribute to a traditional IRA, you or your spouse must have earned income from a job. But, otherwise,

you

may be able to deduct contributions

to an IRA even if you or your spouse are covered by another retirement plan at

work. Plus, starting last year, seniors age 70½ and older with earned income can contribute to a traditional IRA, too.

Here's some more good news: The IRA deduction is an "above the line" adjustment to income, meaning you don't have to itemize

your deductions to claim it. It will reduce your adjusted gross income (AGI) dollar-for-dollar, lowering your tax bill. And

your lower AGI could make you eligible for other tax breaks, which are tied to income limits.

Who Qualifies

If you're single and don't participate in a retirement plan at work, you can make a tax-deductible IRA contribution for 2020

of up to $6,000 ($7,000 if you're 50 or older) regardless of your income. If you're married and your spouse is covered by a

workplace-based retirement plan but you're not, you can deduct your full IRA contribution as long as your joint AGI doesn't

top $196,000 for 2020. You can take a partial tax deduction if your combined income is between $196,000 and $206,000.

But even if you do participate in a retirement plan at work, you can still deduct up to the maximum $6,000 IRA contribution

($7,000 if you're 50 or older) if you're single and your income is $65,000 or less ($104,000 if married filing jointly). And

you can deduct some of your IRA contribution if you're single and your income is between $65,000 and $75,000, or if you're

married and your income is between $104,000 and $124,000.

Spouses with little or no earned income for 2020 can also make an IRA contribution of up to $6,000 ($7,000 if 50 or older) as

long as their spouse has sufficient earned income to cover both contributions. The contribution is tax-deductible as long as

your household income doesn't exceed the limits for married couples filing jointly.

Double Tax Break

Some low- and moderate-income taxpayers get an extra break for contributing to an IRA or other retirement account.

In addition to the usual IRA deduction, you may qualify for a Retirement Savers tax credit of up to $1,000 for contributions

to an IRA or other retirement tax plan. (A tax credit, which reduces your tax bill dollar-for-dollar, is more valuable than a

deduction, which merely reduces the amount of income that is taxed.)

The actual amount of the credit depends on your income. It ranges from 10% to 50% of the first $2,000 contributed to an IRA or

other retirement account. To be eligible, your 2020 income can't exceed $32,500 if you're single; $48,750 if you're the head

of a household with dependents; or $65,000 if you're married filing jointly. The lower your income, the higher the credit. But

you can't claim the Retirement Savers credit if you're under 18, a student, or can be claimed as a dependent on someone else's

tax return.

Skip advert

Advertisement

@ Grieved | Dec 19 2020 6:01 utc | 135 with the rant about the Dems and Medicare for

All

The US government has been financialized like the majority of the Fortune 500. Since the

1970's the trajectory in the US has been to reduce government spending on social safety net

programs and privatize the Social Security Insurance program. While SSI was raped by

Reagan/Greenspan/Congress and taken from the independence of actuaries and made a political

budget football including false claims of being and "entitlement" program the safety net

social programs fared worse. In the early 1970's, when I was familiar with the planning for

and provision of social services like for developmental disabilities, alcoholism, mental

health, job search help, infancy care (WIC) and drug abuse, the concept of continuum of care

helped the different agencies collaborate and really help folks. Then the Fed stared changing

the rules of the way money was to be spent that developed columns of services that don't

interact/coordinate with each other as well as reducing overall low income support.

I also want to add to what you wrote earlier that humanity use to make other than the

throw-away-to-churn-the-money-mill products that were both designed and built better/to last.

It fits with our throw away food system with all that packaging and none of it refillable,

seemingly by design.....

....

....

because as I continue to write here, its all about the God of Mammon instead of the support

of the masses social structure with the underpinning of the God of Mammon way of life is

controlled by the global private financed owned elite and the support of the masses way of

life is exampled biggly currently by China.

For eight-and-a-half decades, most Republican legislators (and some Democrats) have been

trying to get rid of Social Security .

The first step in Trump's assault on Social Security's funding took effect Sept. 1st.

On Trump's orders, the IRS ordered corporations to stop withholding Social Security

contributions from paychecks, through the end of the year.

Speaking on Fox Business recently, Trump advisor Larry Kudlow said that later this year

Trump will order the IRS to continue the deferral indefinitely.

Social Security's chief actuary wrote that if Social Security is defunded, some benefits

will be reduced next year, and that benefits will disappear entirely by the end of 2023.

If you are, or if you know someone on Social Security, please pass the word!

I'm 52, won't live past 80 and have $1.6 million. 'I am tired of both the rat race and workplace

politics.' Should I retire?

More

I don't have much in savings and feel lost. What can I do? Dear Wondering in Alamo, You bring up a question I

think a lot of people have been asking themselves lately.

https://s.yimg.com/rq/darla/4-2-1/html/r-sf.html

Start survey

U.S.

Your retirement distributions won't be taxed in these states: AARP

Ann Schmidt

,

Fox Business

•

July

31, 2020

There are 12 states that won't tax your distributions from

401(k)

plans,

IRAs or pensions, according to a recent report from

AARP

.

Of those states, nine -- Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas,

Washington and Wyoming -- don't have state income taxes.

Some states only partially tax retirement distributions, AARP reported. In Colorado, taxpayers over 65

can remove

$24,000

from

their federal AGI for their state taxes, according to AARP.

Other states have policies for taxes on retirement distributions that depend on your occupation before

retirement. For example, in Connecticut, teachers can subtract 25 percent of their retirement income from

federal AGI.

There are also 29 states that don't tax

military

retirement

income at all, AARP reported. Those states include Alabama, Arkansas, Connecticut, Hawaii, Idaho,

Illinois, Kansas, Louisiana, Maine, Massachusetts, Missouri, New Jersey, North Dakota, Ohio, Oregon,

Pennsylvania, Rhode Island, South Carolina, West Virginia and Wisconsin.

The remaining 21 states tax some or all of military retirement income, according to AARP.

One exception is in Virginia, where only recipients of the Congressional Medal of Honor are exempt from

taxes on their military retirement income, AARP reported.

"... "By the Department of Labor's own admission, these are investments that are more complex, more opaque, less liquid, more difficult to value, with often higher costs than the investments that are traditionally offered through retirement plans," Roper said in an interview with Yahoo Finance. ..."

Managers of 401(k) plans now have the ability invest in private equity. In other words, your

401(k ) could soon take stakes in private companies.

The goal, according to Labor Secretary Eugene

Scalia is to allow investors to "gain access to alternative investments" and "ensure that ordinary people investing for retirement

have the opportunities they need for a secure

retirement

." The Department of Labor laid things out in a

letter that says putting 401(k) money into private-equity funds would not "violate the fiduciary's duties" of certain retirement

plan sponsors.

But some experts see a big downside.

Barbara Roper, the Director of Investor Protection

at the Consumer Federation of America, said the "significant risks" associated with private equity investments haven't been adequately

addressed.

"By the Department of Labor's own admission, these are investments that are more complex, more opaque, less liquid, more

difficult to value, with often higher costs than the investments that are traditionally offered through retirement plans," Roper

said in an interview with Yahoo Finance.

You 'could do much, much worse'

The DOL letter means that a 401(k) manager could now decide to invest in private-equity funds that previously were not accessible.

These funds traditionally have been reserved for the wealthiest traders and institutional investors. They typically come with higher

risk since private companies are not required to disclose nearly the same about of data with the SEC as public companies do.

The new rule could be tempting for average savers who may now have a roundabout way to get a piece of a company – like SpaceX

or AirBnB – that's still private. The American Investment Council, which represents the private equity industry, has

lauded the change , saying it will strengthen Americans' retirement security.

One thing that remains up in the air is how quickly the managers of the big retirement plans will embrace their new options. Companies

like Vanguard and Fidelity have not yet offered comment on the new guidelines. Another

outstanding question is whether these plans would list private-equity funds among the options for savers to choose from, or whether

private equity would simply be mixed into existing funds.

Alexis Leondis, an opinion columnist for Bloomberg,

recently asked if the move is worth the risks. “Many plan sponsors don't have the sophistication or background in alternatives

to fully understand the complicated structures of many private equity funds," she wrote.

Roper said that “the dispersion of returns in the private-equity fund space is huge, much broader than it is in the public markets.”

And while the returns for over-performing private equity funds can, indeed, beat the public markets, “if you get in a below average

fund, you could do much, much worse," she said.

An example of a big downside in private equity fund is SoftBank’s Vision fund. That fund

recently announced losses of $24 billion

after failed investments in WeWork and OneWeb.

According to

a 2018 study by the Stanford Center on Longevity, about half of American workers are saving money through a retirement plan at

work. Access to and participation in 401(k)s is much lower among younger workers.

A report from the National Institute on Retirement Security found that two-thirds of working millennials have nothing saved for

retirement.

A second rule change, over financial advice

A second change is coming soon and is expected to relax restrictions on the advice financial professionals give about their retirement

investments.

The change,

passed by the SEC last year with a compliance deadline of June 30, says brokers must act “in the best interest of the retail customer

at the time the recommendation is made, without placing your financial or other interest ahead of the retail customer’s interests.”

SEC Chairman Jay Clayton has said that the change is part of "raising the standard of conduct for broker-dealers," while he has

discussed in interviews how the best interest standard is different than a fiduciary standard.

According to the Consumer Federation of America, the move could lead to an understanding that investment advisers are not true

fiduciaries. A fiduciary is someone legally obligated to act in the best financial interests of the clients they are advising.

Roper

says that this potential new rule gives broker-dealers and investment advisers “virtually unlimited ability to act as advisers,

while simultaneously failing to regulate them accordingly.” They can now “mislead their customers into believing they are getting

trusted, best interest advice when they are actually getting investing recommendations biased by toxic conflicts of interest,” she

said.

Roper appeared as part of Yahoo Finance’s ongoing partnership with the

Funding our Future campaign, a group of organizations

advocating for increased retirement security for Americans.

Consumer Federation of America is an association of non-profit consumer organizations. More than 250 groups – from local agencies

like the New York City Department of Consumer Affairs to private groups across the country – participate in the federation.

All of these changes may not be noticed by certain savers who are often encouraged to take a “set it and forget it” approach to

their retirement.

If their 401(k) provider does end up getting involved in private equity, advocates like Roper say that "the promise of improved performance

is not necessarily met by the reality."

Ben Werschkul is a producer for Yahoo Finance in Washington, DC.

Required Minimum Distributions (RMDs) generally are minimum amounts that a retirement plan

account owner must withdraw annually starting with the year that he or she reaches 72 (70

½ if you reach 70 ½ before January 1, 2020), if later, the year in which he or

she retires. However, if the retirement plan account is an IRA or the account owner is a 5%

owner of the business sponsoring the retirement plan, the RMDs must begin once the account

holder is age 72 (70 ½ if you reach 70 ½ before January 1, 2020), regardless of

whether he or she is retired.

Retirement plan participants and IRA owners, including owners of SEP IRAs and SIMPLE IRAs,

are responsible for taking the correct amount of RMDs on time every year from their accounts,

and they face stiff penalties for failure to take RMDs.

When a retirement plan account owner or IRA owner, who dies before January 1, 2020, dies

before RMDs have begun, generally, the entire amount of the owner's benefit must be distributed

to the beneficiary who is an individual either (1) within 5 years of the owner's death, or (2)

over the life of the beneficiary starting no later than one year following the owner's death.

For defined contribution plan participants, or Individual Retirement Account owners, who die

after December 31, 2019, (with a delayed effective date for certain collectively bargained

plans), the SECURE Act requires the entire balance of the participant's account be distributed

within ten years. There is an exception for a surviving spouse, a child who has not reached the

age of majority, a disabled or chronically ill person or a person not more than ten years

younger than the employee or IRA account owner. The new 10-year rule applies regardless of

whether the participant dies before, on, or after, the required beginning date, now age 72.

The RMD rules apply to all employer sponsored retirement plans, including

profit-sharing plans, 401(k) plans, 403(b) plans, and 457(b) plans. The RMD rules also apply

to traditional IRAs and IRA-based plans such as SEPs, SARSEPs, and SIMPLE IRAs.

The RMD rules also apply to Roth 401(k) accounts. However, the RMD rules do not apply to

Roth IRAs while the owner is alive.

You must take your first required minimum distribution for the year in which you turn age 72

(70 ½ if you reach 70 ½ before January 1, 2020). However, the first payment can

be delayed until April 1 of 2020 if you turn 70½ in 2019. If you reach 70½ in

2020, you have to take your first RMD by April 1 of the year after you reach the age of 72. For

all subsequent years, including the year in which you were paid the first RMD by April 1, you

must take the RMD by December 31 of the year.

A different deadline may apply to RMDs from pre-1987 contributions to a 403(b) plan (see FAQ

5 below).

Return

to List of FAQsHow is the amount of the required minimum distribution

calculated?

Generally, a RMD is calculated for each account by dividing the prior December 31 balance of

that IRA or retirement plan account by a life expectancy factor that IRS publishes in Tables in

Publication 590-B ,

Distributions from Individual Retirement Arrangements (IRAs) . Choose the life expectancy

table to use based on your situation.

Joint and

Last Survivor Table - use this if the sole beneficiary of the account is your spouse and

your spouse is more than 10 years younger than you

Uniform

Lifetime Table - use this if your spouse is not your sole beneficiary or your spouse is

not more than 10 years younger

The Decade in Retirement: Wealthy

Americans Moved Further Ahead https://nyti.ms/34pZAbD

NYT - Mark Miller - Dec. 14

... In 2010, the economy was just beginning to recover from the worst recession and

financial crisis in recent memory. The unemployment rate was high, the stock market was

coming back and millions of workers were worried that their retirement plans were ruined.

Since then, a robust economic rebound has put some Americans back on solid footing for

retirement, but progress has been uneven. Despite the gains made in employment, wage growth

has only recently begun to recover -- and remained flat for older workers. Retirement wealth

has accumulated almost exclusively among higher-income households, while middle- and

lower-income households have only held steady or lost ground, Federal Reserve data shows.

Trends in Social Security and Medicare also are troubling. The value of Social Security

benefits -- measured by the share of pre-retirement income they replace -- is falling, and

the cost of Medicare is rising.

For members of the baby boomer and Gen X generations, the odds of success are mixed. The

Employee Benefit Research Institute has developed a model that simulates the percentage of

households likely to have adequate resources to meet retirement expenses, considering

household savings, home equity and income from Social Security and pensions.

The model shows that the highest-income households have seen their odds of a successful

retirement improve sharply during this decade, and have very high odds of success.

Middle-income households, meanwhile, have seen some gains, but still have only 50-50 odds of

success. And the lowest-income households have seen their retirement prospects diminish

sharply -- among these boomers approaching retirement, their odds of success have fallen

during the decade from 26 percent to 11 percent.

"Retirement prospects improved significantly for higher-income workers who were fortunate

enough to work for employers that sponsor retirement plans," says Jack VanDerhei, the

organization's research director.

Let's consider how the retirement landscape has changed during the decade now ending.

Retirement savings: Up for the affluent

The stock market bottomed out in March 2009 -- and it has more than quadrupled since then.

Most retirement savers did not abandon equity markets during the crash, says Jean Young,

senior research associate with the Vanguard Center for Investor Research. "Some did, but the

vast majority stayed the course."

But the recovery has seen retirement wealth accumulate almost exclusively among affluent

households that had access to workplace retirement plans and the means to make contributions.

For example, Vanguard reports that the average balance for plan participants with incomes

over $150,000 in 2018 was $193,130, compared with just $22,679 for workers with income of

$30,000 to $50,000. ...

Humans have an amazing capacity to suspend disbelief, a trait that novelists, Hollywood and,

sadly, criminals, have used to notable effect. Here are some typical frauds.

Wire transfer scams: A retired businessman in his 80s was contacted by people who claimed

they wanted to do business with him. Thinking he was back in the game and investing in a real

deal, he wired them $400,000. When he discovered he'd been defrauded, he complained to the

scammers, who then passed him along to new crooks who said they could get his money back if

he would wire them $400,000 -- which he did.

Third-party scams: Some victims play an unwitting role in facilitating scammers' attempts

to defraud a third party. For example, a gentleman in his 80s gave scammers between $600,000

and $1 million from his bank accounts. After the fraud was discovered by his family and

financial institution, he lost access to his funds. But that didn't stop the scammers. They

set up a PayPal account under his name and Social Security number, convinced him to go to

TitleMax® and borrow money using his car as collateral, then had him put the funds in the

PayPal account to which they had access.

Gift card scams: Gift cards can be used to launder money without even having to

physically send the cards anywhere. A scammer convinces the victim to go to a store, get one

or several cards, and load each one up with money. Then, they have the victim scratch off a

protective strip on the back of the card to reveal its code number, take a picture of the

number, and then text the picture to a cellphone number.

Computer-hacking scams: A common ruse aimed at seniors involves a contact from someone

claiming to be a Microsoft employee. The fake Microsoft rep claims the senior's computer has

a virus or some other problem, which they're happy to fix. The senior simply needs to click

on an email link or download an attachment the rep sends them -- and pay a fee. With one

click by the victim, the scammer gains control of the victim's computer. One victim paid

about $300 -- over and over -- to the same scammers, who kept "fixing" her computer since

they could break it as often as they chose. The victim had no idea what was happening.

Door-to-door scams: A fraudster knocks on a senior's door and says her trees need to be

trimmed or gutters need to be cleaned. I know of two people who each paid a crook $30,000 to

trim the hedges at their house. No trimming took place; the criminal just hung out for a

while and reappeared to help the elderly client write a check for their services.

Transaction settlement scams: A scammer claims they need someone to act as an agent or

middleman to help settle a transaction, such as a divorce or property settlement. The victim

receives a check that looks legitimate, deposits it in their own account or a trust account,

then wires the money to the scammer. Of course, the check was fake, but the victim's real

money is gone.

Family member financial abuse: I could devote a whole article to this type of abuse.

Financial frauds within a family can be difficult to resolve. Is an elderly parent

voluntarily giving real gifts to a family member? Or is fraud involved? Without proper

documentation, financial fraud within a family can devolve into a he said/she said conflict

among siblings and others.

Even if the timing remains vague and the conditions uncertain, the government does seem to

have decided to launch a vast reform of the retirement pensions system, with the key element

being the unification of the rules applied at the moment in the various systems operating

(civil servants, private sector employees, local authority employees, self-employed, special

schemes, etc).

Let's make it clear: setting up a universal system is in itself an excellent thing, and a

reform of this type is long overdue in France. The young generations, particularly those who

have gone through multiple changes in status (private and public employees, self-employed,

working abroad, etc), frequently have no idea of the retirement rights which they have

accumulated. This situation is a source of unbearable uncertainties and economic anxiety,

whereas our retirement system is globally well financed.

But, having announced this aim of clarification and unification of rights, the truth is that

we have not said very much. There are in effect many ways of unifying the rules. Now there is

no guarantee that those in power are capable of generating a viable consensus in this respect.

The principle of justice invoked by the government seems simple and plausible: one Euro

contributed should give rise to the same rights to retirement, no matter what the scheme, and

the level of salary or of earned income. The problem is that this principle amounts to making

the inequalities in income as they exist at present sacrosanct, including when they are of

mammoth proportions (under-paid piece work for some, excessive salaries for others), and to

perpetuating them at the age of retirement and dependency which is in no way particularly

"fair".

Aware of the difficulty, the High Commissioner Jean-Paul Delevoye's Plan stipulates that a

quarter of the contributions will continue to be allocated to "solidarity', that is to say, for

example, to subsidies for children and interruptions of career, or to finance a minimum

retirement pension for the lowest salaries. The difficulty is that the way this calculation has

been made is highly controversial. In particular, this estimate purely and simply takes no

account of social inequalities in life expectancy. For example, if a low wage earner spends 10

years in retirement while a highly-paid manager spends 20 years, we have forgotten to take into

account the fact that a large share of the contributions of the low wage earner serves in

practice to pay the retirement of the highly-paid manager (which is in no way compensated for

by the allowance for strenuous and tedious work)

More generally, there are naturally multiple parameters to be fixed to define what one

considers to be "solidarity". The government's proposals are respectable but they are far from

being the only ones possible. It is essential that a broad public debate take place and that

alternative proposals should emerge. The Delevoye Plan for example provides for a replacement

rate equal to 85% for a full career (43 years of contributions) at Minimum Wage level. This

rate would then very rapidly fall to 70%, to only 1.5 Smic (Minimum Wage) before stabilising at

this precise level of 70% until approximately 7 Smic ( 120,000 Euros gross annual salary). This

is one possible choice, but there are others. One could thus imagine that the replacement rate

would go gradually from 85% of the Smic to 75%-80% around 1.5 – 2 Smic, before gradually

falling to around 50%-60%, approximately 5-7 Smic.

Similarly the government's project provides for a financing of the system by a retirement

contribution of which the global rate would be fixed at 28.1% on all the gross incomes below

120,000 Euros per annum, before falling suddenly to only 2.8% beyond this threshold. The

official justification is that retirement rights in the new system would be capped at this wage

level. The Delevoye Report goes as far as congratulating themselves because the super-managers

will nevertheless be subject to this contribution (which will not be capped) of 2.8%, to mark

their solidarity with the older generations. In passing, once again no account is taken of the

salaries between 100,000 Euros and 200,000 Euros which usually correspond to very long life

expectancies and which benefit greatly from the contributions paid by the lower waged with

shorter life expectancies. In any event, this contribution of 2.8% to solidarity by those

earning over 120,000 Euros is much too low, particularly given the levels of remuneration;

their very legitimacy is open to challenge.

More generally it is perhaps time to abandon the old idea according to which reduction of

inequalities should be left to income tax, while the retirement schemes should content

themselves with reproducing them. In a world in which fabulous salaries and questions of

retirement and dependency have taken on a new importance, the most legible norms of justice

could be that all levels of salary (including the highest) should finance the retirement scheme

at the same rates (even if the pensions themselves are capped) while leaving to income tax the

task of applying higher levels to the top incomes

To be clear: the present government has a big problem with the very concept of social

justice. As everyone knows, it has chosen from the outset to grant huge fiscal gifts to the

richest (suppression of the wealth tax (the ISF), the flat tax on dividends and incomes). If

today it does not demand a significant effort from the most privileged it will have

considerable difficulty in convincing the public that its pension reform is well-founded.

It seems like barely a quarter goes by without Wells Fargo being exposed for some abusive

practices, like opening millions of fake credit card accounts, or selling customers of its auto

loans insurance that they didn't really need (but that the company insisted they did).

In the

latest violation,

the New York

Times

reports that Wells Fargo continued to charge overdraft and other charges to customers

even after closing their accounts for one of a myriad reasons.

The paper used Xavier Einaudi, a small business owner who banked with Wells, as its primary

example.